War is not merely a matter of courage but also of finance. Short conflicts can be managed like natural disasters; prolonged warfare reshapes an entire economy. Israel, a nation accustomed to substantial military investment, has found itself at a crossroads since 7 October 2023. That day triggered a chain of events, with the response to an attack escalating into a large-scale operation extending beyond Gaza to multiple fronts. The war escalated into a 12-day clash with Iran, straining finances further. The question now looms: how long can Israel’s economy sustain the pace of these complex operations without plunging into a deep crisis?

Challenges to Economic Stability

Israel benefits from long-term planning and crisis preparedness. Resilience is not confined to its military but extends to its people and, ultimately, its economy. Israel relies on vigilance and foresight to endure. Yet even this economic resilience has limits. With the war against Iran and a planned large-scale operation in Gaza, involving the resettlement of one million people, these limits will be severely tested.

Rating agencies downgraded Israel’s credit rating in 2024 due to the Gaza conflict, though they remain lenient for now. All agencies maintain a negative outlook on Israel’s economy, warning that further downgrades are possible if the conflict persists. And persist it does, compounded by the clash with Iran. Consequently, another downgrade seems likely, though agencies are hesitant. Israel still holds an A rating from S&P, one notch below Slovakia’s A+. A further downgrade to A- would place Israel alongside nations like Poland, Croatia, or Cyprus. Such a downgrade would significantly complicate Israel’s return to economic prominence, as a lower rating means higher yields when borrowing money. Israel must borrow to finance the war, currently doing so at a 10-year bond yield of 4.1%, lower than the 4.3% for US 10-year bonds. Investors still trust the robust fundamentals of Israel’s economy and its potential recovery, making lending to Israel somewhat safer than to the US—assuming the economy returns to normal.

Economic and Social Impacts

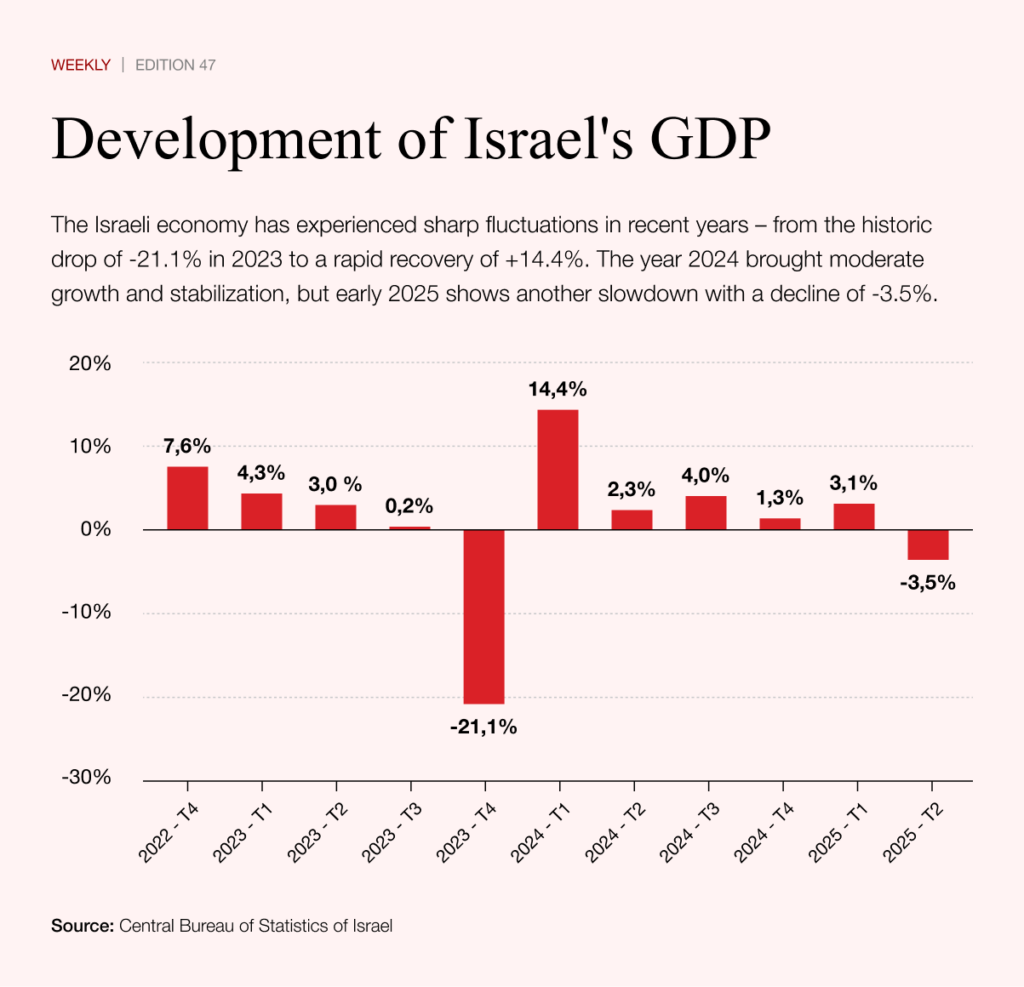

A return to normality would require an end to direct conflict. The war’s impact is most evident in GDP trends. In the final quarter of 2023, when the Gaza operation began, Israel’s economy contracted by 21%. Mobilising 280,000 reservists (7% of the workforce) halted parts of the economy. The conflict response also prompted over 800,000 Israelis—more than 20% of the active population—to pause work, bringing the economy to a near standstill, akin to the Covid pandemic. The country saw an exodus of 250,000 Palestinian and foreign workers, and a further blow came from the emigration of over 82,700 Israelis in 2024, mostly skilled individuals able to secure opportunities abroad, leading to a brain drain.

Compounding these issues are soaring military expenditures, which rose by over 65% in 2024 to $46.5 billion—the largest increase since the Six-Day War in 1967. Military spending now exceeds 8.8% of GDP, the second-highest globally, driving public debt to 69%. Inflation remains above the 2% target (3.2–3.8% annually, totalling 12% over four years). The government has kept income taxes low but raised VAT (from 17% to 18%) and property taxes (+5.3%). Public transport costs have surged by a third.

Returning to normalcy will not be straightforward. The 12-day war with Iran caused a further 3.5% GDP drop. Estimated costs for the Gaza conflict range from $65 billion to $74 billion (at least 13% of annual GDP, per the central bank), while the Iran clash cost at least $6 billion. The largest expense is the defence system intercepting Iranian missiles and drones, with each interception costing between $700,000 and $4 million. These figures suggest that another conflict with Iran would burden Israel’s economy even more than the prolonged Gaza operation.

The Paradoxical Success of Israel’s Stock Market

Israel’s macroeconomic context offers little cause for optimism. Yet the Tel Aviv Stock Exchange paints a different picture. The TA 35 index has posted remarkable gains in recent months, rising 24.8% year-to-date, outpacing Germany’s DAX by two percentage points, which has benefited from investors seeking assets unaffected by Trump’s trade policies. Over the past year, the Israeli index surged by over 46%, surpassing Hong Kong’s 44% and even the US Nasdaq, led by stars like Nvidia and Palantir, with 18% growth. The performance of Israel’s stock market is thus extraordinary.

The reasons behind this paradoxical success are intriguing. Intense military conflict drives innovation. Conflicts force companies to seek new solutions, spurring technological advancements with broad applications. Firms in military technology can test and refine their innovations in real-world conditions. A speculative factor also plays a role: every conflict eventually ends, and peace could propel Israel’s economy and stock market to new heights. Moreover, a change in political leadership could shift Israel’s focus from security investments to unlocking its economic potential. Markets are betting on a swift end to the conflict—while the economy still awaits it.

Statement

Israel’s economy faces unprecedented strain from ongoing conflicts, including a major operation in Gaza and a 12-day clash with Iran, costing billions and pushing military spending to 8.8% of GDP. Since 7 October 2023, the nation has grappled with a 21% GDP drop, mass mobilisation, and emigration of skilled workers, alongside rising debt and inflation. Rating agencies warn of further downgrades, yet Israel’s TA 35 stock index has surged 46% in a year, outpacing global peers like Nasdaq. This paradox stems from conflict-driven innovation and investor optimism for peace, but the economy’s resilience is nearing its limits.