Sold as an economic wunderkind, Emmanuel Macron rose to the presidency in 2017 on a centrist, pro-European, pro-business platform. France, he promised, would be reformed — made sleek, competitive, and modern, adopting a new form of liberalism. Eight years on, the verdict is fractured. With only 29% of French citizens rating him a good president (Odoxa), his legitimacy is questioned across the political spectrum, from the radical left to the far right.

Macron emerged as if from nowhere. His aura was forged during a brief yet storied tenure at Rothschild & Co., where he reportedly helped steer a €9bn deal for Nestlé to acquire Pfizer’s baby food division — besting Danone in the process. He became a managing partner two years after his arrival at the firm. The perfect narrative: a brilliant technician with a dealmaker’s poise which isn’t appreciated by everyone, especially on the socialist side. In his own words, “What I did in the private sector is very useful to me today. It’s no bad thing to have worked in business before managing one.”

He joined the French socialist president, François Hollande in 2012, became economy minister in 2014, and then resigned in 2016 to create his own party. That decision — made while still steering economic policy — laid the groundwork for a campaign that claimed to transcend the old political cleavages. A new kind of liberalism was promised. Something more efficient, more elegant.

A Peculiar Liberal Method

Macron’s first term did sound like a liberal overture: scrapping the wealth tax (except on property), introducing a 30% flat tax on capital gains, loosening labour laws, cutting corporate tax from 33% to 25%, and launching the “Choose France” initiative, which drew €15bn in foreign investment in 2023 alone.

These policies won him the applause of business leaders and investors who had long viewed the French tax system as hostile. For a moment, it seemed the country might become a continental poster child for supply-side reform.

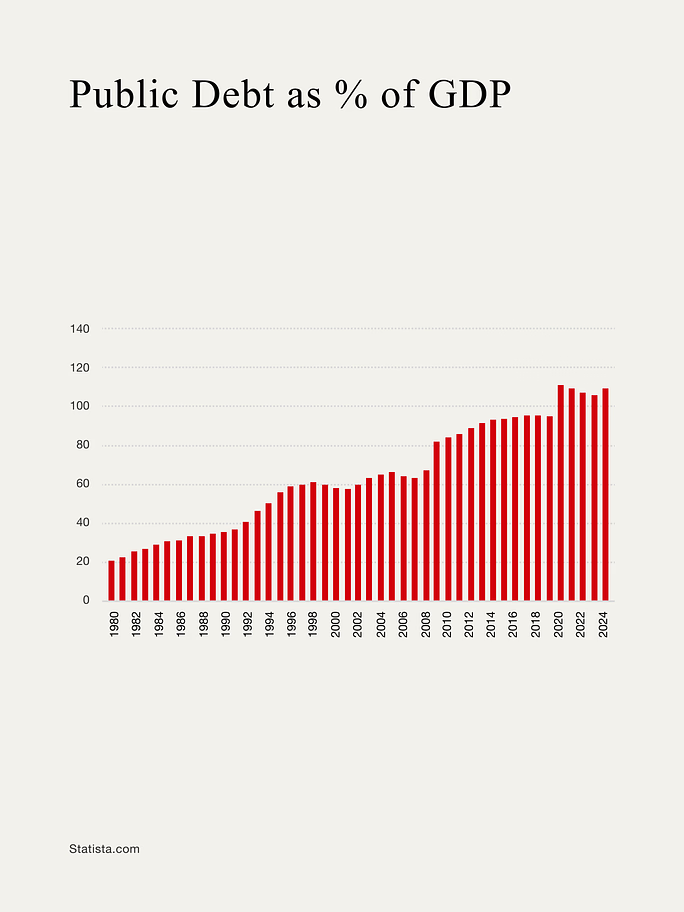

Behind the pro-market choreography, though, the state’s footprint deepened. Public debt ballooned from €2.2 trillion in 2017 to over €3.1 trillion in 2024 — an unprecedented surge, only partially ascribable to Covid-era spending. The budgetary trajectory suggests a more radical shift. Far from trimming the state, Macron has merely re-costumed it.

He claims to be “neither left nor right.” His policies reflect something vaguer still: an expensive balancing act. Billions have been spent to stabilise purchasing power, patch up demand, and placate social unrest — with few structural gains to show for it.

The government capped energy price increases at 15% instead of 45%, a measure costing over €45bn. Social transfers were expanded: minimum pensions, disability allowances, and the activity bonus were all boosted. Students received meals for as little as €1. School breakfasts were made free. MaPrimeRénov’ and MaPrimeAdapt, the renovation and ageing-in-place subsidies, accrued more than €5bn — an organised theft growing on climate anxiety. In the end, though, none of these measures has revealed a long-term economic vision.

Credit agencies have taken due note. Standard & Poor’s, which rates the quality of French sovereign debt, has steadily downgraded the country since Macron’s first involvement in economic policy under Hollande — from AAA to AA- as of May 2024. This makes things look as though this new Mozart failed to better France’s overall economy. The downgrade, in fact, reflects more than ballooning deficits: it signals international doubts about France’s overall capacity to reconcile growth with fiscal discipline — a challenge Macron promised to master, but merely postponed.

Purchasing Power: A Discordant Reality

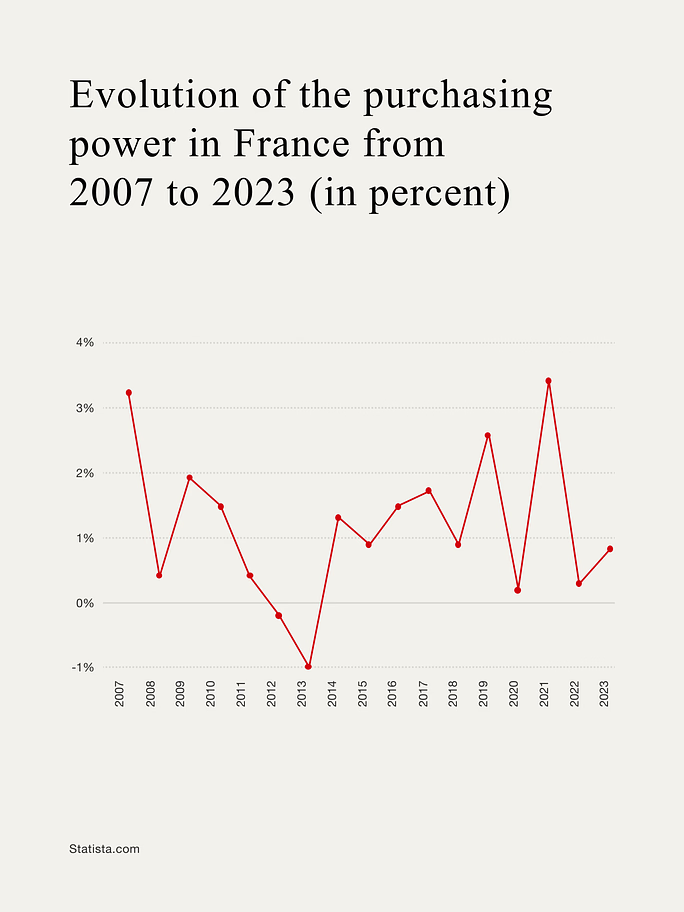

The strength of an economic project is ultimately assessed at daily level. And here, too, the melody of Macronism has grown increasingly discordant. Admittedly, the government did not hold back on headline measures: a 19.36% increase in the minimum wage between 2017 and 2024, tax exemptions on overtime, and exceptional bonuses such as the “value-sharing bonus” paid out to 6.8 million employees.

The sharp rebound in purchasing power in 2022 (+3.4%) was less the sign of a structural improvement than the product of temporary Covid-era support: energy price caps, inflation bonuses, and state subsidies. By 2023, the momentum had already faded — with growth down to just +0.8%.

Yet, behind this apparent generosity, figures tell a more sobering story. In 2023, according to DARES, 17.3% of private-sector employees (excluding agriculture) were earning the minimum wage — up from 12% in 2021. This five-point leap in just two years reveals a foundational concern: the minimum wage, designed as a floor, has become the default arrangement for nearly one in five workers. In a context of high inflation, raising the SMIC has indeed helped sustain purchasing power — but it has also frozen intermediate wages.

The resulting social strain is visible. In 2022 alone, shoplifting surged by 14%, mirroring a brutal 16.3% spike in food prices in supermarkets over a single year. Bonuses have become a palliative provision for stalled wage negotiations; the state, a substitute for a skewed productive system.

In truth, what Macron has orchestrated is less a recovery than a delicate act of economic tightrope walking: buying time with billions, without restoring either corporate margins or wage dynamics.

Statement

Macron promised a liberal symphony but delivered a state-subsidised improvisation — elegant in tone, incoherent in structure. Purchasing power was propped up, debt soared by nearly €1tn, and France’s credit rating dropped. This reveals the paradoxical nature of Macron’s legacy: the apparent championing of market liberalisation and pro-business measures should have contained state intervention, rather than entrenching it as it has. This tension, while safeguarding market interests, questions the authenticity of neoliberal ideology and worries investors as well as policymakers. As concerns about fiscal sustainability, social equity, and the genuine autonomy of market forces overshadow short-term economic stimulation, the Macron experiment leaves behind not reform, but a finely orchestrated illusion.