A house in Italy for €29,000 ($32,900) may look like a real estate anomaly, but it is best understood as an exception rather than a trend. Although it is clear at first glance that living there would require significant investment in its own right, the headline price is genuinely unusual.

Across most of the rest of the continent, the picture looks rather different. The latest Eurostat data points to a market that has moved into a new growth phase. The relevant question is therefore no longer whether prices are rising, but where they are rising fastest, where they have reached their highest levels and where opportunities for investors still remain.

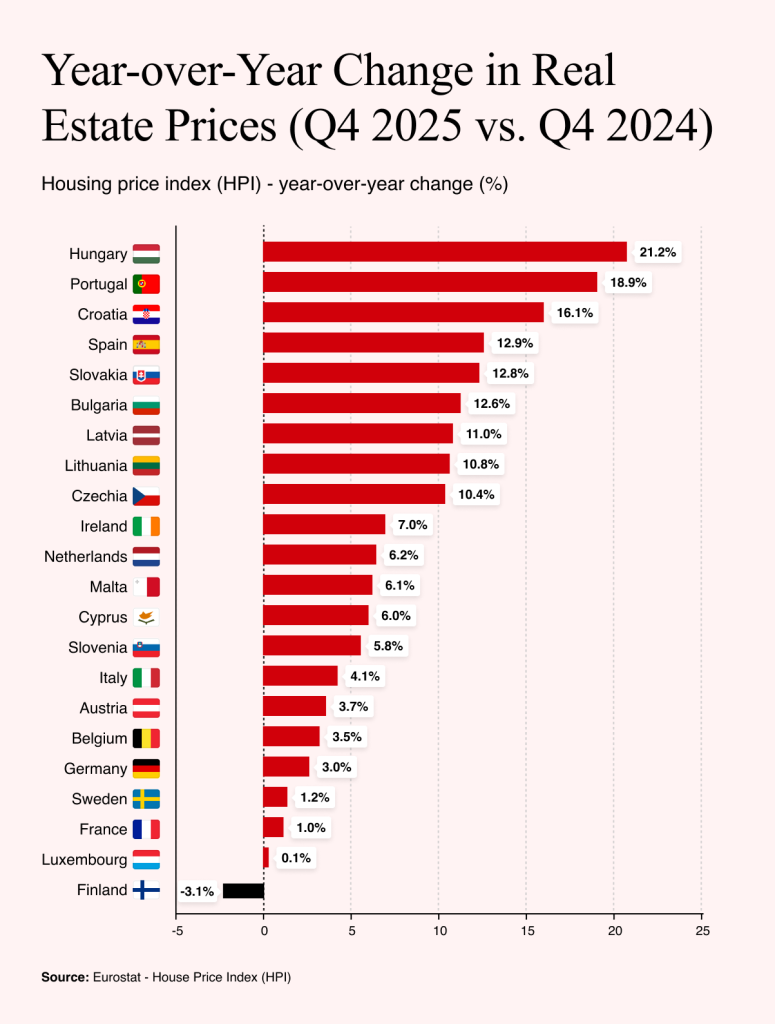

The figures themselves are telling. House and apartment prices across the European Union rose by 5.5% year on year in the fourth quarter of 2025, with the eurozone recording a slightly more moderate gain of 5.1%. The increase held up on a quarter-on-quarter basis as well, in both the EU and the eurozone.

This points to a broader recovery: after a period of stagnation, the European market is picking up again. Over the past ten years, prices across the EU have jumped by nearly 65%, while rents have risen by approximately 22%, a gap that helps explain why real estate continues to be regarded as one of the most reliable hedges against inflation.

In many countries, there is a persistent shortage of new construction, with development projects routinely held up by lengthy permitting processes. At the same time, easier access to mortgages is adding fuel of its own. Together, these factors point to renewed upward pressure on prices.

Western Europe Sets the Price Ceiling, the East Stays a Bargain

In terms of absolute prices for new apartments and homes, Luxembourg now stands as the most expensive country in Europe, according to the Deloitte Property Index, with the average price of new housing there reaching €8,760 ($9,950) per sq m.

At city level, the gap is even more pronounced. Geneva, Switzerland, leads by a wide margin, with apartment prices in its most prestigious locations exceeding €15,000 ($17,000) per sq m, well ahead of Zurich and London. This is consistent with a broader pattern in which Switzerland, Norway, Ireland, the Netherlands and Denmark have long occupied the top tier of the continent's most expensive markets.

Germany, by contrast, illustrates a more tentative recovery. According to Eurostat, real estate prices there rose by 3% year on year in the fourth quarter of last year, the fifth consecutive quarter of growth. Yet the quarter-on-quarter figure tells a more cautious story, with prices up just 0.1%, suggesting that a momentum has yet to build.

Germany went through one of the most significant corrections on the continent after a period of cheap mortgages, as higher interest rates and a weaker economy pushed prices down, particularly in major cities. According to Deloitte, the market is now gradually returning to growth, with the average price of residential real estate reaching approximately €4,800 ($5,450) per sq m.

Munich continues to be the country's most expensive city and ranks among the priciest real estate markets in Europe more broadly.

Austria offers a more stable contrast. The country has long ranked among Europe's most expensive real estate markets, with the average price per square meter for a new apartment exceeding €5,000 ($5,670) as early as 2024, putting it behind only Luxembourg and the United Kingdom.

Yet the Austrian Statistical Office notes that prices, while rising again, have not yet returned to the record levels seen in 2022. That pattern points to a market defined less by sharp price growth than by stability and capital preservation.

In 2025, Vienna retained its position as Austria's most expensive real estate market, with average apartment prices reaching €5,212 ($5,912) per sq m and single-family homes commanding even more, at €5,376 ($6,097) per sq m. Tyrol, Vorarlberg and Salzburg complete the picture of a country where high prices are concentrated in a handful of well-defined regions.

At the opposite extreme are the countries of South-East Europe, where housing in Bulgaria, Romania, Albania and Bosnia and Herzegovina remains a fraction of Western European levels. Data from the Global Property Guide places some regions of Greece and North Macedonia in the same bracket, among Europe's cheapest real estate markets.

The scale of the gap becomes clear once translated into actual prices. Last year, a buyer in the Austrian capital paid approximately €365,000 ($414,000) for a 70-sq-m apartment. The same apartment in central Geneva would cost more than €1m ($1,134m), while in parts of the Balkans, where prices fall below €2,000 ($2,270) per sq m, it would cost roughly €140,000 ($158,800), a more than sevenfold difference within a single, integrated European market.

The East Takes the Lead in Europe's Price Race

However, the most interesting developments are not taking place in the wealthiest countries, but in the eastern part of the continent.

Hungary illustrates this most clearly. Eurostat notes that the country has seen an extraordinary rise in housing prices over the past decade, with Budapest prices increasing by approximately 290% since 2015, the highest rate in the entire European Union.

A similar dynamic is playing out, albeit less dramatically, in Poland, the Czech Republic, Croatia and Slovenia, where real estate prices have also risen significantly. In each case, the same two forces are at work: convergence with Western European living standards is driving demand upward, while a persistent shortage of new apartments in major cities keeps supply from catching up, leaving prices under sustained pressure.

France, somewhat unexpectedly, fits into a similar pattern. Prices there are rising again after two weaker years, with real estate in several major cities increasing by 3%–4% annually and an even more pronounced upward trend visible in parts of western France.

Slovakia fits this pattern closely. Following a correction in 2023 and 2024, the country's real estate market has picked up significantly, placing it among the fastest-growing markets in the European Union. According to Eurostat data, last year Slovakia was among the group of countries where housing prices grew significantly faster than the European average,

Yet the comparison with Western Europe puts that growth in perspective. Housing in Slovakia remains considerably cheaper overall. According to the National Bank of Slovakia, the average housing price last year was around €2,800 ($3,176) per sq m, though Bratislava sits well above that national figure, with prices there reaching above €4,000 ($4,537) and even €5,000 ($5,670) per sq m.

Bratislava and regional capitals, particularly Kosice, continue to hold the greatest potential, with prices there rising faster than household incomes.

The Limits of Growth at the Top of Europe's Property Market

However, not every market is moving in the same direction.

London illustrates the limits of growth at the top of the price scale. The city remains caught in an affordability squeeze, with prices in some parts of the British capital even falling year on year, a combination of high interest rates, tax changes and a price level that has simply outrun what many buyers can afford.

That dynamic, analysts argue, is not unique to London. In markets that have already reached extremely high prices, there is structurally less room for further sharp growth, whereas regions that have not yet converged with Western European levels tend to offer greater upside.

It is this logic of undervaluation that increasingly shapes where investors choose to look.

An analysis by the KBC banking group points out that the gap between EU real estate markets remains wide, with not all of them equally expensive today. Parts of Greece, Romania, Bulgaria and certain regions of southern Italy stand out as particularly attractive on this basis, drawing investors with lower entry prices and room for further growth.

According to the Global Property Guide's assessments, some South-East European markets reinforce this picture further still, offering rental yields significantly higher than those available in Western Europe.

What Investors Should Expect Next

Most analysts no longer expect a repeat of the double-digit price increases seen in the post-pandemic period. That, however, points to a slowdown in the pace of growth rather than a reversal of it. Prices are not set to fall. Quite the contrary.

Demand for housing continues to outstrip supply, new apartments are being built at a slow pace, and people are still moving to cities, all of which keeps pushing prices higher. This leaves significant room for growth, particularly in Central and Eastern European countries and in regions where prices remain lower than in the western part of the continent.

For investors, this leads to a relatively straightforward conclusion. Europe's most expensive cities now look set to offer stability rather than significant price growth, while greater potential lies in countries where real estate is still relatively affordable and the economy is growing faster than the European Union average.