To investors, macroeconomic forecasts—predictions of GDP growth or inflation rates—serve very much the same function a lighthouse does to the captain of a ship.

While they offer orientation and direction, they never guarantee certainty. Just as meteorologists cannot precisely predict every gust of wind, even the most sophisticated economic models cannot capture every turbulence in the global economy.

Unexpected events—be it geopolitical shocks or the subtle ‘flutter of a butterfly’s wings’—can swiftly undermine even the most robust forecasts. Although algorithms dominate trading floors today, even the largest investment funds continue to rely on human strategists who interpret data with an intuition inaccessible to machines.

In an era of uncertainty, mastering the art of understanding forecasts’ inherent imperfection remains crucial for navigating economic waters.

Macroeconomic Statistics Rewritten by Donald Trump

The challenge of interpreting macroeconomic numbers is universal and persistent. However, since January 2025, Donald Trump has returned to the White House, bringing an ambitious plan to overhaul previously untouchable free trade agreements.

The detailed description of this transformation, outlined in the Miran's Plan, is intricate and involves numerous interlinked steps. The primary critique is precisely its complexity and interconnected nature—difficult to execute even by the most systematic individual. Yet, the chaotic figure of Donald Trump is pursuing this complex plan. Trump's contradictory rhetoric has muddled rather than clarified his ambitious economic agenda.

This chaotic management style is evident even in macroeconomic statistics. A prime example is the US GDP. In the first quarter of 2025, the American economy reported negative growth of 0.2%, a stark contrast to the preceding quarter’s 2.4% growth. Such a sharp slowdown would typically require a significant event—like a pandemic, war, or coup—which did not occur.

The explanation for this statistical anomaly is simple: American traders aggressively stockpiled goods ahead of the planned ‘Liberation Day’ on 2 April. This massive import surge led to a statistical downturn without reflecting an equivalent real-world economic decline. Imports surged by 41.3% quarter-on-quarter. Adjusted for imports, US GDP would have grown by 1.2%, representing a slowdown driven by uncertainty surrounding Trump’s policies. Companies, wary of an unstable environment, are curbing investment, thus contributing to a genuine economic slowdown. Trump himself acknowledges that the economy must undergo a transformative process, potentially causing GDP contraction or even recession—a sacrifice deemed necessary to ‘make America great again.’ Precisely forecasting US GDP or inflation under these circumstances verges on crystal-ball gazing.

Jerome Powell’s Crystal Ball

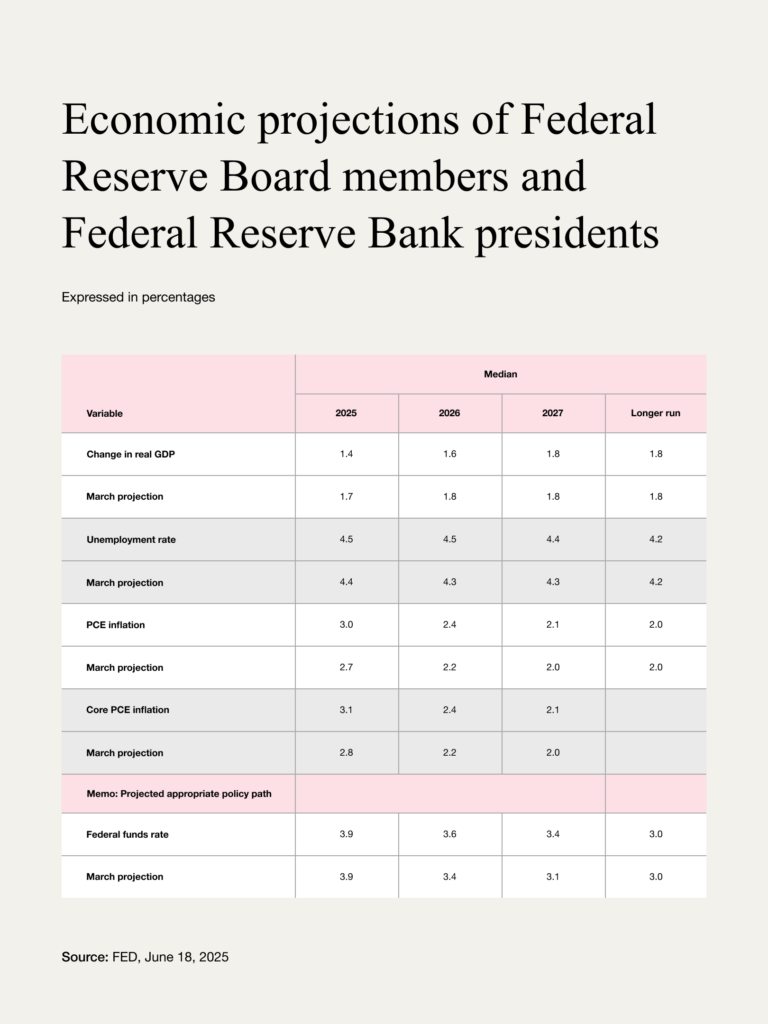

Despite the complexities, the US Federal Reserve (Fed) regularly updates its economic projections. The latest Fed meeting drew significant attention primarily due to these projections. Jerome Powell and fellow Fed members left interest rates unchanged, aligning with market expectations. However, they substantially revised their economic outlook.

The Fed reduced its GDP growth forecast from 1.7% to 1.4%, signaling continued dismissal of a recession scenario. However, falling below the critical 1.5% mark implies uncertainty around sustained job creation.

Another critical indicator closely being monitored is inflation. The potential for a second inflation wave lies at the heart of disagreements between Trump and Powell. Trump insists that his tariff policies will not significantly affect US price levels and suggests goods might even become cheaper. However, should tariff wars trigger inflation, Trump proposes delaying interest rate adjustments. Powell, aligning with economists opposing the president, contends there is a tangible risk of rising inflation.

The Fed adjusted its projection for PCE inflation from 2.8% to 3%. While inflation remaining above the 2% target throughout the year obliges the Fed to pursue restrictive monetary policy for long-term price stability, a modest increase by two-tenths of a percentage point does not portend uncontrollable inflation or social unrest. Yet, the US attack on Iranian targets could undermine Trump’s goal of maintaining oil prices at $60 per barrel.

Toward Stagflation

If oil prices rise, inflation follows, given that virtually all goods and services depend directly or indirectly on fossil fuels. Higher energy costs inherently dampen economic activity. The Fed’s projections—still excluding the implications of the Israeli attack on Iran—already highlighted existing tendencies: decelerating GDP growth coupled with accelerating inflation. These trends are likely to intensify further. Should nominal GDP decline amid persistently high inflation, the economy will enter a period of stagflation.

Stagflation's complexity arises from the dilemma it poses for central banks: recession demands lower interest rates, whereas inflation necessitates increases. Stagflation demands both simultaneously—an impossibility by definition. Central banks thus often find themselves paralysed, hoping merely for miracles. Markets, always forward-looking, have noticed this hesitation. Powell’s repeated inaction suggests he might, in reality, be waiting for stagflation to unfold.

Ultimately, reliance on macroeconomic forecasts signals an adherence to faith more than it does one to science. Investors overly reliant on statistics may find comfort in their precision, yet reality always asserts itself.

Statement

Navigating macroeconomic forecasts under Trump’s chaotic economic policies resembles sailing through a dense fog, where even sophisticated predictions falter amid unprecedented market volatility. The sharp contraction in US GDP during early 2025, artificially triggered by import surges ahead of Trump's ‘Liberation Day,’ masks deeper investor anxieties over policy instability and potential stagflation. Jerome Powell’s cautious revisions reflect a realistic assessment: economic growth slowing sharply and inflation inching upward. Trump's aggressive trade and geopolitical moves risk igniting stagflation—central banks’ worst nightmare. Investors relying solely on precise statistics ignore a crucial truth: navigating economic uncertainty demands intuition and skepticism, not blind faith in algorithms.