When Javier Milei assumed the presidency in December 2023, Argentina was macroeconomically ruined. Annual inflation had breached 270%, the peso was worthless, and the Central Bank had become a money printer. Government reserves were gone, confidence shattered, and another IMF bailout lurked. Into this chaos stepped a libertarian promising to dismantle the state.

Eighteen months later, Argentina’s condition is no longer terminal. The patient is stabilising but far from cured.

From Hyperinflation to Disinflation

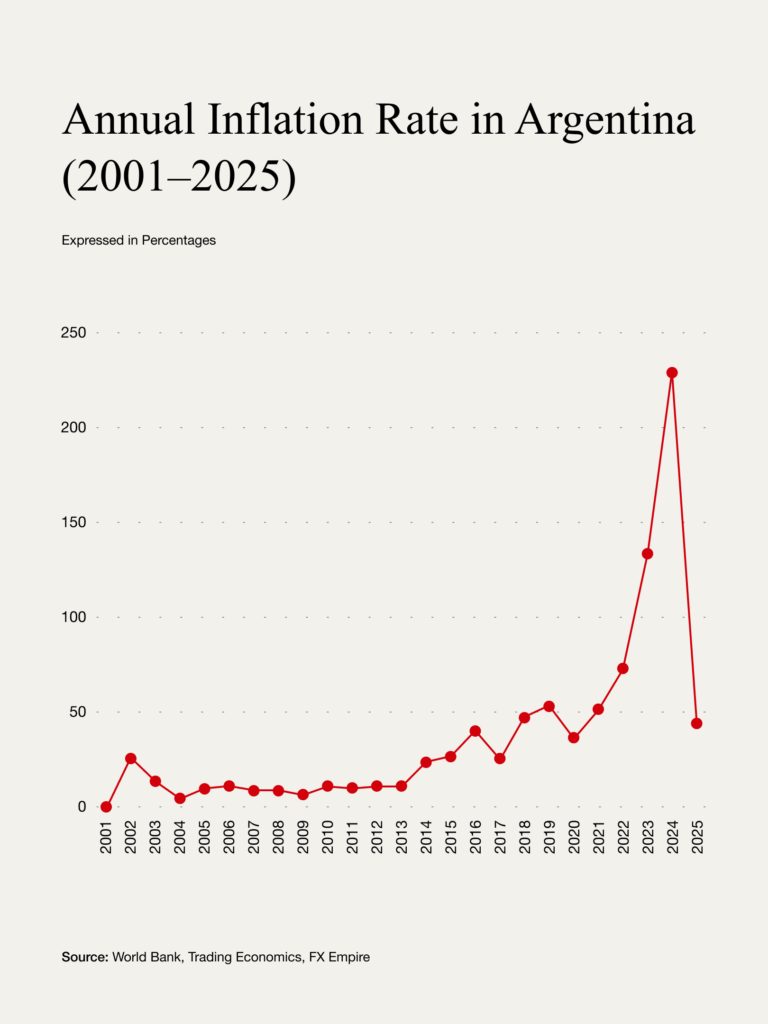

By May 2025, inflation had fallen to 43.5%, down from 276% a year ago, and Argentina's monthly inflation rate now hovers around 1.5%, the lowest since early 2018. For a country where prices once changed weekly, this is a stunning reversal.

The methods have been brutal though: Milei’s government slashed energy subsidies, cancelled public works, froze intergovernmental transfers, and eliminated tens of thousands of state contracts. These cuts delivered Argentina’s first primary budget surplus since 2008, equal to 0.4% of its GDP.

To Milei, this was a long-overdue correction, but to critics, it was economic arson dressed as reform.

Monetary policy was equally strict. The Central Bank stopped deficit financing, restricted peso issuance, and absorbed excess liquidity. Interest rates soared, then eased as inflation declined.

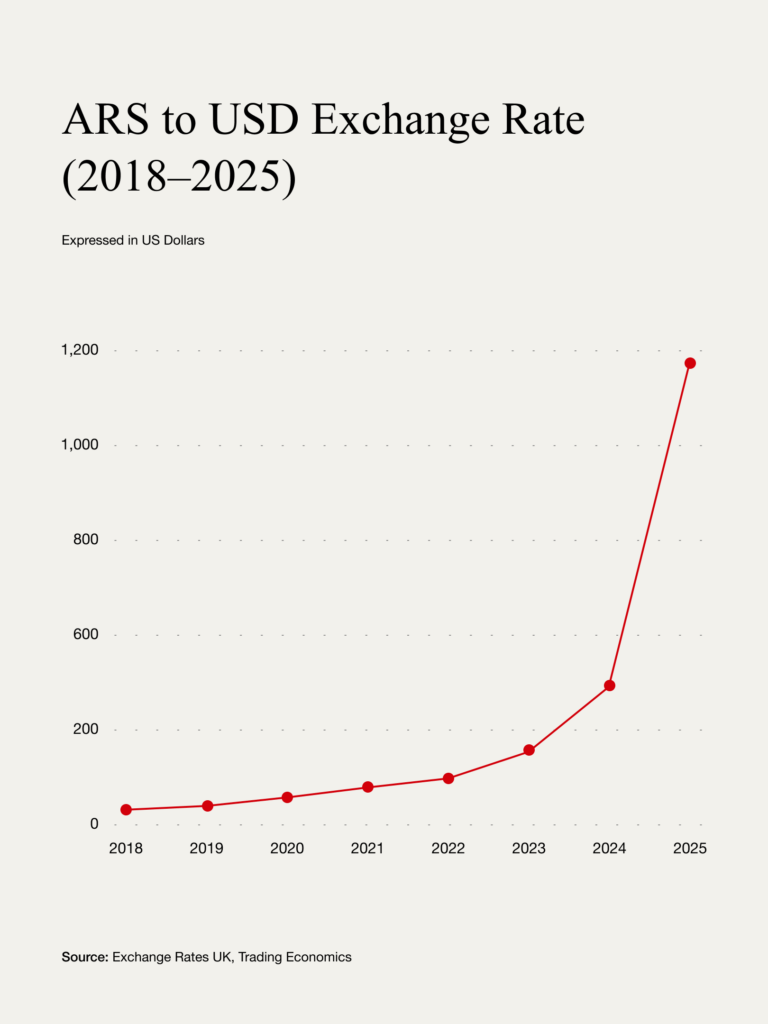

In December 2023, the government devalued the official peso by over 50% and allowed it to be freely exchanged. It now trades around 1,200 per US dollar, down from 120 in early 2022. While nominally wrecked, Argentina’s multiple and conflicting exchange rates have finally converged into a single, stable, and most importantly, truthful one.

Throughout this process, the IMF has cautiously endorsed the changes, and global markets have nodded approvingly, but inside Argentina, contradictions remain.

Taking Pain Without Complaint

Behind the macro recovery lay a certain social blowback at first, as wages in the public sector, the country’s largest employer, initially fell over 18% in real terms, and poverty peaked above 60% for the first time in over 20 years, although unemployment is now only up to 9.5%.

This has been Milei’s cure: it works, but at a cost, Yet, despite the apparent consequences, political backlash has been surprisingly muted.

Milei’s approval, though slipping, remains at 60%. After decades of delusion, his blunt refrain, “There is no money”, feels truthful. Argentines, though exhausted, are not in shock.

Added to this, in April 2025, the IMF approved a USD 20 billion Extended Fund Facility, with USD 12 billion disbursed immediately to shore up reserves. Conditions include quarterly fiscal targets, Central Bank autonomy, and exchange rate flexibility.

So far, all benchmarks have been met, and after years of reversals, the IMF sees in Milei something rare in the region: the ability to deliver actual results.

The Dollarisation Question

Milei’s most radical promise, replacing the peso with the US dollar, remains unrealised. Argentina still lacks the reserves needed, estimated at USD 40–50 billion, and current reserves sit below USD 30 billion, much of it consisting of money still owed or otherwise unusable.

Still, the trajectory is clear. Capital controls have been loosened, peso-denominated debt is being phased out, and dollar-linked financial products are promoted while foreign investment rules are liberalised. Milei’s advisers suggest dollarisation could proceed once inflation drops further, though an official date is still pending.

The model is Ecuador, which dollarised in 2000 amid economic collapse. In five years, inflation had vanished, and growth stayed modest, as macro stability returned. Argentina’s path here is rockier: its trade unions, dollarisation’s main opposers, are stronger, its politics less predictable, its institutions more fragile. But Milei sees the urgency of the situation.

Argentina, Its Past and its Neighbours

Argentina remains an anomaly within Latin America. Brazil, Chile, and Peru all keep inflation under 5%. Argentina, still recovering from the past chaos, stands apart. Argentina's currency has lost over 90% of its value since 2022. Only Venezuela has suffered worse.

Yet Argentina matters. It has the region’s third-largest economy, immense natural resources, and a strong agri-industrial base. Investor confidence is tentatively returning as borrowing costs are falling, capital inflows are resuming, and foreign investment is beginning to rise.

The key question, though, is political endurance, as Argentina’s economic history has been a rollercoaster.

The 1990s Convertibility Plan pegged the peso to the dollar, inflation vanished, and foreign capital flowed. Then came collapse: the pegging rate broke, banks froze, and unemployment soared. That trauma still persists.

Today’s plan is more flexible, with more comprehensive corrections. But every success is viewed with suspicion, every reform doubted, every statistic felt to be temporary. Even when the numbers improve, trust remains absent.

The fear is not inflation, it's relapse. Argentines have seen too many recoveries die on the vine. This is the test: not just growth, but permanence. Not merely reform, but durability.

And yet, Argentina is not poor, but it's terribly broken. A once-prosperous, educated nation, it has been hollowed out by state failure and elite betrayal, and inflation is the most visible symptom of its disease: institutional rot.

Whether Milei can break the cycle depends not only on markets or macro policy, but on the political will to see it through.

Statement

Under Milei, Argentina has managed to cut inflation from a 276% high in December 2023 to 43.5% in May 2025, ended deficit financing, secured a primary surplus, and landed a USD 20 billion IMF deal. These are historic feats. But they have come at a cost: an over 60% poverty rate, falling wages, and deepening unrest. Javier Milei’s programme is not a modest reform. It is a rupture. Its future depends less on market response than on political endurance. Argentines have seen many recoveries fail. Milei has not promised the change to be painless. It simply must be done, as there is no alternative.