In the spacious conference room of the New York Federal Reserve during the summer of 1979, the atmosphere was palpably tense. Paul Volcker, freshly appointed Chairman of the Fed, sat at the head of the table, closely observing the anxious movements of his colleagues. Before them lay charts depicting rising oil prices, slowing economic growth, and a dangerously increasing unemployment rate. Looming in the room was a spectre: stagflation, an economic phenomenon contradicting every textbook principle.

On the surface, stagflation seems straightforward, yet it proves exceptionally complex in practice. It combines economic stagnation—either a slowdown or outright recession—with rising inflation. Frequently, it is accompanied by increasing unemployment. Traditional economic models, such as the Phillips Curve, assume inflation and unemployment act as balancing scales: when one rises, the other falls. Job losses reduce purchasing power, thereby pressing prices downward. Conversely, tight labour markets empower workers to demand higher wages, inflating prices. Stagflation defies this logic. It represents an anomaly, baffling central bankers as standard instruments—interest rates or fiscal policy—suddenly appear ineffective. Stagflation remains a central banker’s nightmare, resistant to orthodox remedies.

A Brief History: The Crisis of the 1970s

To understand this phenomenon better and assess whether it poses a genuine threat today, let us revisit the American experience of the 1970s. This decade remains synonymous with economic turmoil and its consequent challenges. Inflation gradually spiralled out of control.

In 1971, President Richard Nixon implemented wage and price controls to combat inflation, yet such measures proved ineffective—as do most policies that disregard free-market principles. In 1974, President Gerald Ford introduced the ‘Whip Inflation Now!’ campaign, which similarly floundered due to reliance on slogans rather than systemic reforms. The situation deteriorated further with the 1973 oil crisis, prompted by an Arab embargo against countries supporting Israel during the Yom Kippur War. A second oil shock occurred in 1979–1980, driven by the Iranian Revolution. The geopolitical interplay between Iran and Israel continues to underscore the need for vigilance today. Despite a possible ceasefire halting the rise in oil prices after 23 June 2025, stability remains uncertain.

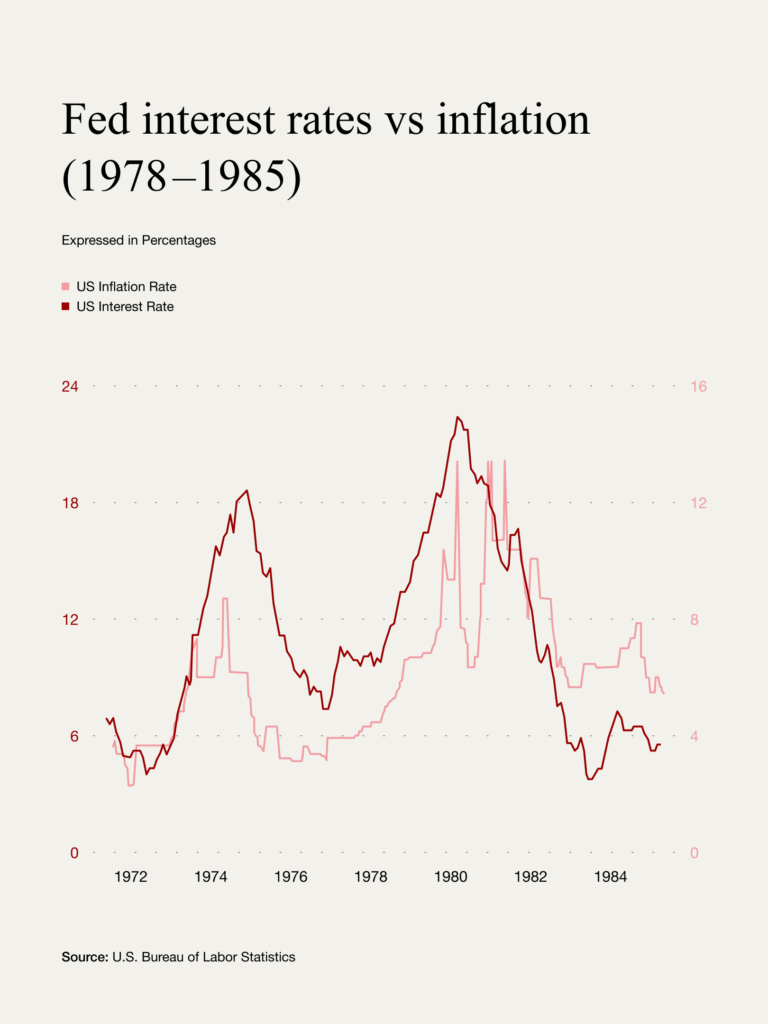

Returning to the 1970s, Paul Volcker adopted a radical measure: drastically raising interest rates above 20% to tame inflation approaching 15%. This ‘Volcker Shock’ entered history, successfully curbing inflation but at the cost of soaring unemployment, peaking at 10.8%.

Causes and Limitations: Why Does Stagflation Occur?

If we schematically analyse stagflation—accepting some simplification—we conclude it originates from numerous misguided decisions. Had central banks acted decisively in the mid-1970s, they might have prevented such rampant inflation. Central bank interventions typically require a remedial process involving short-term discomfort but promising long-term resolution. Politicians, however, find such ‘suffering’ politically unpalatable.

Yet central banks' miscalculations alone do not fully explain these crises. Typically, an external issue emerges—in the 1970s, it was the oil crisis. Rather than an unpredictable ‘black swan,’ it represented a ‘grey swan’—a known potential issue whose precise timing remained uncertain. Preoccupied with internal problems, central banks failed to respond adequately. Volcker eventually resolved the crisis through extreme measures. Could such decisive actions be repeated today? Probably not. The Volcker Shock raised US debt from approximately 33% to nearly 50% of GDP—a move untenable given today’s already elevated debt levels. Nevertheless, Volcker's clarity of vision and decisiveness remain instructive. He restored confidence in the Fed, precisely what central bankers currently require. Stagflation isn't merely an economic conundrum—it fundamentally reflects lost confidence in central banking leadership, a systemic fault that should be avoided.

The Stagflation Threat in 2025

The latest projections from the US Federal Reserve dated 18 June 2025 offer limited optimism. Expected US economic growth has been revised downward from 1.7% to 1.4%. Inflation, measured by the PCE index, is anticipated to reach 3%, up from an initial forecast of 2.7%. The economy slows while inflation accelerates—signs that stagflation might be approaching. Commodity price increases since early 2025 further compound these concerns. Copper prices rose by over 12%, platinum surged by more than 41%, and should oil prices again climb beyond $90 per barrel, stagflation could become inevitable. Yet, neither President Trump nor Fed Governor Powell can confidently predict such outcomes.

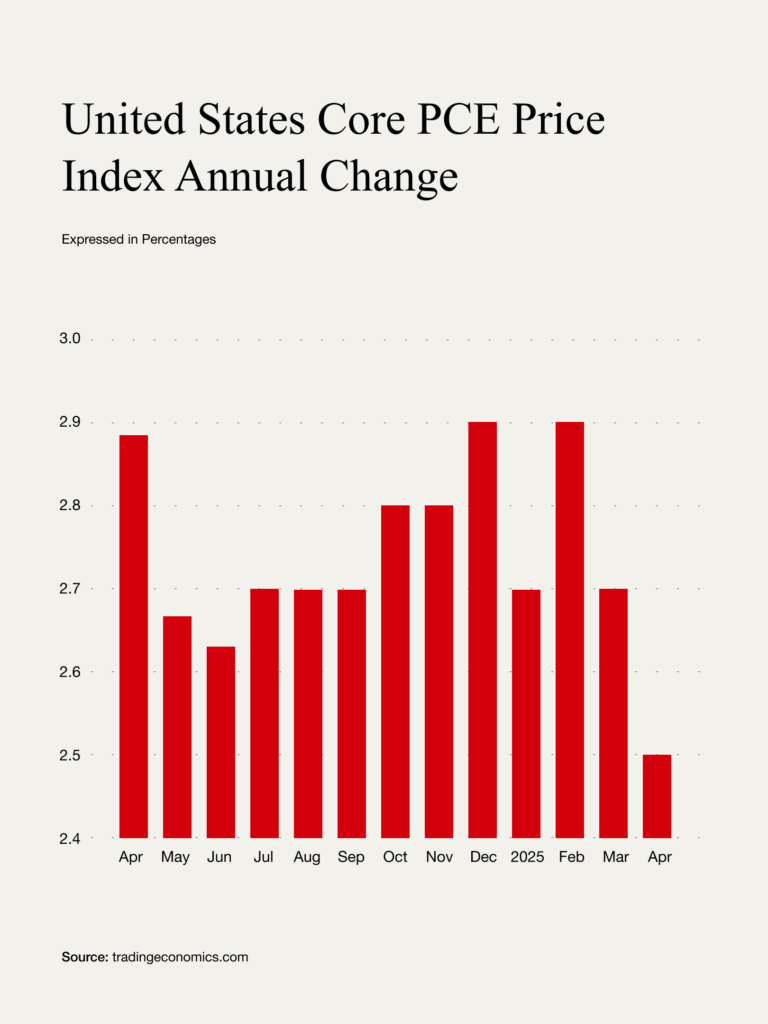

Trump’s criticisms of Powell, whom he dubs ‘Mr. Too Late,’ extend beyond mere frustration over delayed interest rate cuts. By questioning Powell’s competence, Trump positions the Fed chair as a scapegoat should stagflation materialise. Powell defends himself by presenting bleak economic forecasts—like the 2.4% inflation recorded for April 2025. If inflation indeed reaches the predicted 3% by year-end, prices must surge dramatically in a short period. Powell adopts deliberately pessimistic forecasts, allowing him credit should a worst-case scenario fail to unfold. Whether this strategy succeeds or stagflation re-emerges remains uncertain. Modern central banks must regain Volcker’s resolve to avoid repeating past mistakes.

Statement

Stagflation, a troubling mix of inflation, stagnation, and unemployment, haunted the 1970s and returns as a plausible risk today. The economic disruptions of that era—driven by geopolitical shocks and inadequate policy responses—underline the crucial role of decisive central bank leadership. The Volcker Shock, while politically costly, restored essential credibility. Today's central banks face similar threats but with diminished manoeuvring room due to elevated debt.