As Western economies stagger under the twin burdens of inflation and sluggish growth, China charts a very different path. Its consumer-price index (CPI) has hovered around zero, even dipping to –0.1 % year-on-year in April 2025. Yet growth, albeit modest, remains remarkably steady. Price stability amid global volatility is the essence of China’s economic playbook, which prioritises control, insulation, and long-term positioning over short-term stimulus or ideological purity.

Zero Is a Policy Choice

In China, inflation is not simply an output of market dynamics, it is a variable engineered by the state. The government intervenes at multiple levels of the economy to contain cost pressures: tapping into grain and energy reserves, issuing administrative caps on fuel and electricity, and suppressing intermediate cost pass-throughs via state-owned enterprises. The result is CPI inflation that remains below 1% even as global supply chains sputter.

By contrast, the US and eurozone continue to grapple with inflationary pressures exceeding 3%, driven by wage growth, elevated energy prices, and persistent service-sector bottlenecks. China's model relies less on interest rate tightening and more on pre-emptive coordination: a web of reserve pricing, demand-smoothing, and subsidy deployment. For institutional investors, this creates a rare scenario: macroeconomic visibility in an otherwise turbulent emerging-market environment. Yuan assets are no longer simply a bet on growth. They are a hedge against imported instability.

Reflation That Builds

While the West uses fiscal spending to stoke demand, China has opted for what might be called “productive reflation”: targeted capital deployment that increases future supply capacity rather than short-term consumption. In the first quarter of 2025, fixed-asset investment rose by 4.2% year-on-year. That modest figure masks significant divergence: infrastructure investment expanded 5.8%, and manufacturing jumped a striking 9.1%, driven by automation, new energy, and high-end electronics. Excluding the troubled property sector, investment growth was over 8.3%.

The government’s refusal to reignite the housing market signals a strategic move away from asset bubbles and toward foundational productivity. The benefits of this shift may not register in quarterly GDP data, but they are reshaping the overall economic structure.

Neither Stag Nor Flate

Classical stagflation, a toxic mix of low growth and high inflation, has haunted the West since the 1970s. Central banks have spent the past two years trying to suppress price spikes without stalling activity. But China’s decoupled indicators suggest a different dynamic. Q1 GDP grew 5.4% year-on-year, exceeding most expectations. At the same time, consumer inflation was flat, and factory-gate prices, though weak, did not transmit through to households.

This apparent immunity rests on institutional machinery: wage restraint in SOEs, direct intervention in commodity markets, and regulation of upstream pricing. Even when international oil and metal prices surged in early 2025, China’s domestic price indices barely moved. The state’s granular involvement, often criticised for distorting markets, has become a macroeconomic stabiliser.

Deflation as Diplomacy

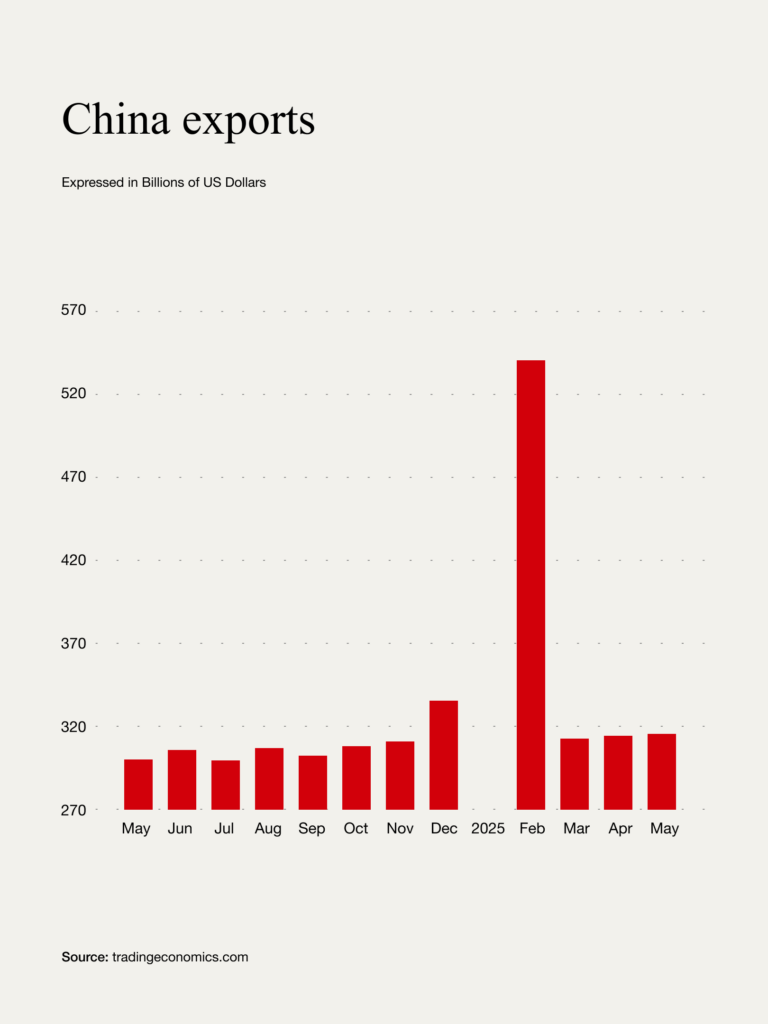

With the renminbi yuan trading in a narrow band and domestic input costs tightly managed, China’s exporters are thriving. From January to April 2025, total trade grew 2.4%, but exports climbed a healthier 7.5% to 8.4 trillion yuan. Machinery and electronics exports rose 7.7%, particularly in EVs, industrial robots, and solar components. Meanwhile, trade with ASEAN expanded more than 8%, and exports to the bloc rose over 20% in April alone.

[Put the chart two]

China is not just weathering stagflation, it is weaponising disinflation. In regions like Africa, Latin America, and Southeast Asia, where consumers are highly price-sensitive, Chinese firms are undercutting European and American competitors struggling with input costs and monetary tightening. The implication for investors: Chinese industrial exporters—especially in mid-tech and energy-efficient sectors—are gaining share in the very geographies where growth is still rising.

For Beijing, price stability is not merely economic hygiene. It is political oxygen. From the 1940s inflation crisis that destabilised the Republic of China, to the late-1980s food price spikes that preceded the Tiananmen unrest, inflation carries political weight in the Chinese state’s memory. The Communist Party’s legitimacy rests in part on delivering stability, and inflation is viewed as an attack on the social contract.

This makes China’s deflation not a problem to be solved, but an equilibrium to be preserved. Pork prices, for example, jumped 13.8% in January 2022. Within weeks, the state released frozen pork reserves, intervened in distribution channels, and muted the shock. In parallel, digital yuan pilots now allow real-time tracking of price-sensitive spending, giving policymakers surveillance not just of prices—but of sentiment. In China, deflation isn’t merely tolerated—it is cultivated as strategic stability, insulating Beijing’s economy from global volatility while reinforcing political legitimacy.

Statement

In a world of economic whiplash, China offers something deeply unfashionable: patience. Its anti-stagflation model is not a miracle, it is a method. One part suppression, one part substitution, and one part strategic restraint. The West confronts inflation with interest rate hikes and hope. China counters with control, buffers, and discipline. For global investors, the choice is not binary. But it is instructive. If the 2020s are a decade of volatility, then China’s technocratic calm may prove more attractive than its modest GDP figures suggest.