Not long ago, Italy was considered the eurozone’s ticking time bomb.

In 2011, yields on its ten-year government bonds soared above 7%, and the dreaded spread over German bunds reached a panic-inducing 570 basis points. Rome’s fiscal credibility was in tatters.

The European Central Bank (ECB), then headed by Jean-Claude Trichet and shortly thereafter by Mario Draghi, resorted to the penning of an extraordinary letter that effectively forced Prime Minister Silvio Berlusconi to resign. What followed was technocratic rule, imposed structural adjustments, and a decade-long perception of Italy as a managed province within the EU.

Fast forward to mid-2025, and the country offers a very different picture. Under Prime Minister Giorgia Meloni, in office since October 2022, Italy has emerged as one of the eurozone’s more stable economies—at least for now. Inflation has subsided, bond spreads are low, and for the first time in recent memory, Italy’s GDP per capita has caught up with that of France. While the country still struggles with long-standing structural weaknesses, the macroeconomic environment and investor sentiment show marked improvement.

Taming Inflation

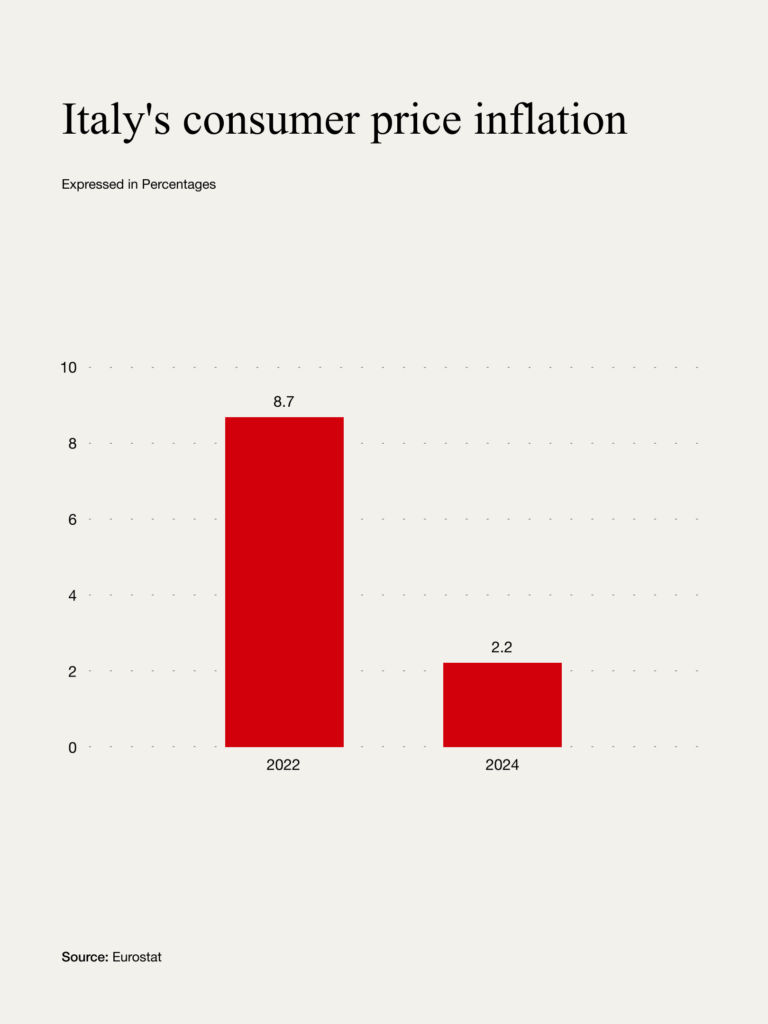

Italy’s inflationary trajectory mirrored that of most European economies during the post-COVID recovery and the energy crisis triggered by Russia’s invasion of Ukraine. Consumer price inflation peaked at 8.7% in 2022, but has since fallen sharply, landing at an estimated 2.2% in 2024 and stabilising into 2025. That figure is slightly below both the eurozone average and France’s current level of 2.5%. Crucially, Italy managed to contain core inflation—excluding energy and food—more effectively than its peers. This has preserved more of households’ purchasing power and avoided a broader wage-price spiral.

Meloni’s government played a modest but noticeable role in maintaining control over inflation. Temporary agreements with the retail and food sectors helped cap prices of essential goods. Though the fiscal cost of such arrangements was limited, they contributed to a perception of the government’s competence, particularly among lower-income households.

The Credibility Gap Closes

Arguably the most striking indicator of Italy’s improved fiscal credibility is the narrowing of the sovereign spread. At the time of writing, the spread between Italian and German ten-year bonds hovers at around 98 basis points—a level not seen since before the eurozone crisis. Markets, once jittery at the mere mention of an Italian budget proposal, now seem to accept Meloni’s economic management as cautious and broadly compliant with European norms.

This confidence comes despite relatively high debt levels. Italy’s debt-to-GDP ratio, which ballooned to 155% in 2020 during the COVID pandemic, has declined, reaching 135.3% in 2024. The fall is due not to budget surpluses—the fiscal deficit remains above 7% of GDP—but to nominal GDP growth fuelled by both inflation and moderate real expansion.

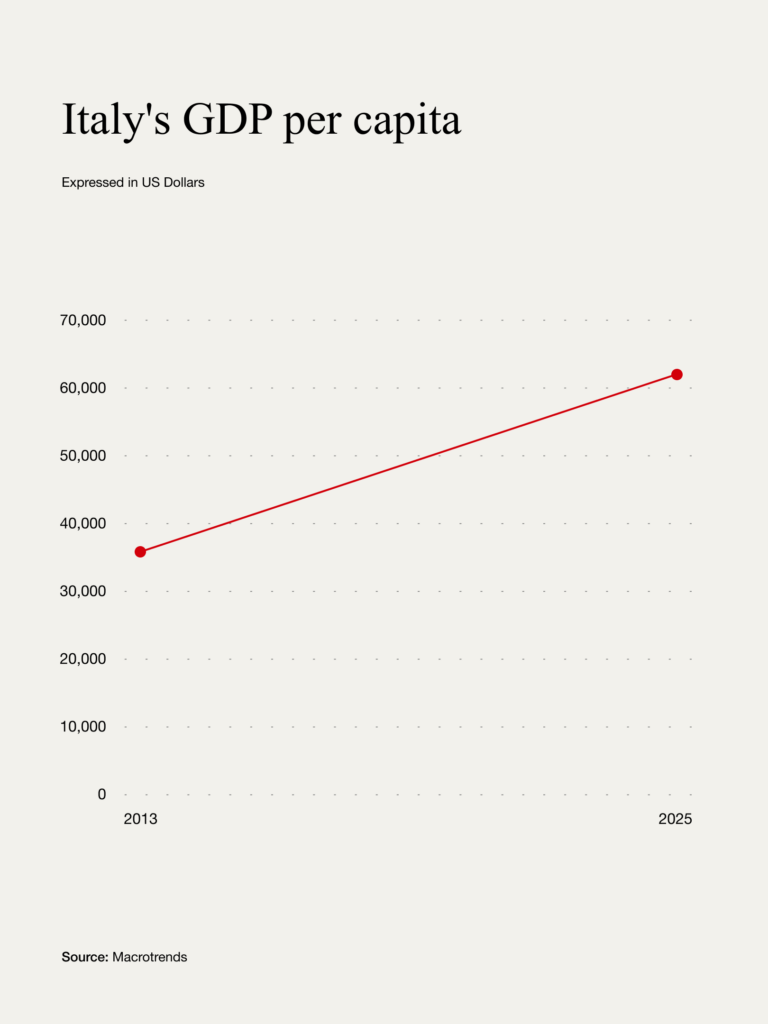

Most symbolically, Italy’s GDP per capita is nearing that of France. In 2013, the gap was around 10% in favour of France. By 2025, Italy’s GDP per capita in purchasing power standards (PPS) has reached approximately $62,600, with France standing at $65,600. In nominal terms, the gap remains but is narrowing steadily.

This shift is partially statistical—France's growth has been weak—but also reflects relative gains made by Italy. The country’s industrial base has stabilised, export performance remains solid, and Italy has benefited from reduced energy dependency and a contained labour cost surge. Business confidence has remained stable, and domestic consumption has not collapsed, despite external shocks.

Political Stability Pays

Its economic performance tells only part of the story however. It is its political stability which underpins Italy’s regained credibility. For much of the 2010s, Italy saw six prime ministers, repeated shifts between technocratic cabinets and fractious coalitions, and periods of outright populist governance. By contrast, Meloni has proven an unusually stable figure.

Domestically, one of her most significant economic reforms was the abolition of the Reddito di Cittadinanza in 2024—a basic income scheme introduced in 2019. Meloni replaced it with more targeted activation policies aimed at employable recipients, particularly citizens under 60. While the new schemes remain modest in scale, the shift signalled a clear reorientation towards labour market participation over passive support. It also helped curb pressure on the welfare budget without triggering significant social unrest.

Though elected on a nationalist, right-wing platform, Meloni has not pursued confrontational economic policies. Her approach to Brussels has been cooperative rather than combative. While advocating for greater national control over migration and budgetary policy, she has not challenged the European Commission. Instead, she has adroitly maximised EU recovery fund disbursements while preserving Italy’s fiscal credibility.

Statement

Italy still faces formidable challenges: weak productivity, an ageing population, regional inequalities, and a cumbersome public sector. But the narrative of economic decline and imminent default that prevailed throughout the 2010s no longer applies. In an EU where Germany wrestles with stagnation and France with ungovernability, Italy now looks like the grown-up in the room. The government’s economic record is not transformative. Growth remains anaemic at 0.7% per annum. But the combination of inflation control, debt stabilisation, and political consistency represents progress. Markets have taken notice and so has Brussels. Italy may not yet be the model student of the eurozone, but it is no longer its problem child.