Oil has fuelled both prosperity and peril in the Middle East. From Saudi Arabia’s vast oilfields to the battlefields of Iraq and Iran, oil wealth has delivered unprecedented prosperity alongside persistent conflict and geopolitical tension. While the gleaming skyscrapers of Dubai and the extravagant wealth of Qatari rulers captivate global attention, countries like Yemen and Syria languish in poverty, reliant on mere fragments of oil revenue. Oil price fluctuations undermine growth prospects, destabilize national budgets, and exacerbate unemployment, deepening social tensions. Indeed, with overall unemployment reaching 20–30% in Iraq and youth unemployment at around 15% in Saudi Arabia, the region’s vulnerability is starkly illustrated.

The considerable disparity of wealth created by oil further intensifies social inequality. Elites live luxuriously, insulated from economic uncertainties, while lower socioeconomic groups and neighbouring states grapple with ongoing instability. Adding to the region’s troubles are macroeconomic imbalances, exemplified by high inflation—such as over 40% in Iran in 2023—alongside weak institutions and chronic balance-of-payments deficits, further hindering paths towards lasting prosperity.

Conflict and Economic Degradation

Yet, the Middle East’s economic landscape is shaped by more than just oil. Regional conflicts exert a devastating impact on economic development. Since 2011, Syria has lost over 80% of its GDP, becoming heavily reliant on humanitarian aid and the black market. War and instability discourage crucial foreign investment, inflate public debt due to massive reconstruction expenses, and divert essential resources away from development towards military spending. This dynamic significantly hampers economic growth and creates widespread uncertainty.

For instance, Saudi Arabia spends more than 8% of its GDP on defence, constraining its capacity to diversify the economy via ambitious initiatives like Vision 2030. Israel, although economically robust thanks to a strong technological and innovative sector, has also experienced substantial costs due to conflicts. In 2024 alone, Israel allocated approximately 100 billion shekels (about 27 billion USD) for military expenses, elevating its public debt from 61.3% of GDP in 2023 to an estimated 67% by 2025.

Consequently, reliance on oil and persistent regional conflicts represent formidable economic and security challenges. Stability remains precarious, especially in the absence of comprehensive reforms to diversify economies and broaden access to employment opportunities.

Can Dreams Sustain with Oil at $60?

The Middle East is marked by a striking concentration of income from hydrocarbons. States within the Gulf Cooperation Council (GCC)—Kuwait, Saudi Arabia, Qatar, the UAE, Bahrain, and Oman—not only share an economic dependence on oil and gas extraction but also a common political system: monarchy. This system ensures that the immense wealth derived from oil remains firmly within the grasp of a privileged elite.

The foundations of their economies remain oil-based. In Saudi Arabia, oil contributes roughly 40–45% of GDP and an even larger share of state revenues. Qatar is particularly dependent, with oil revenues comprising over 82% of the state treasury in 2024. Such dependence renders Qatar vulnerable, particularly if oil production costs continue to rise or if prices decline significantly.

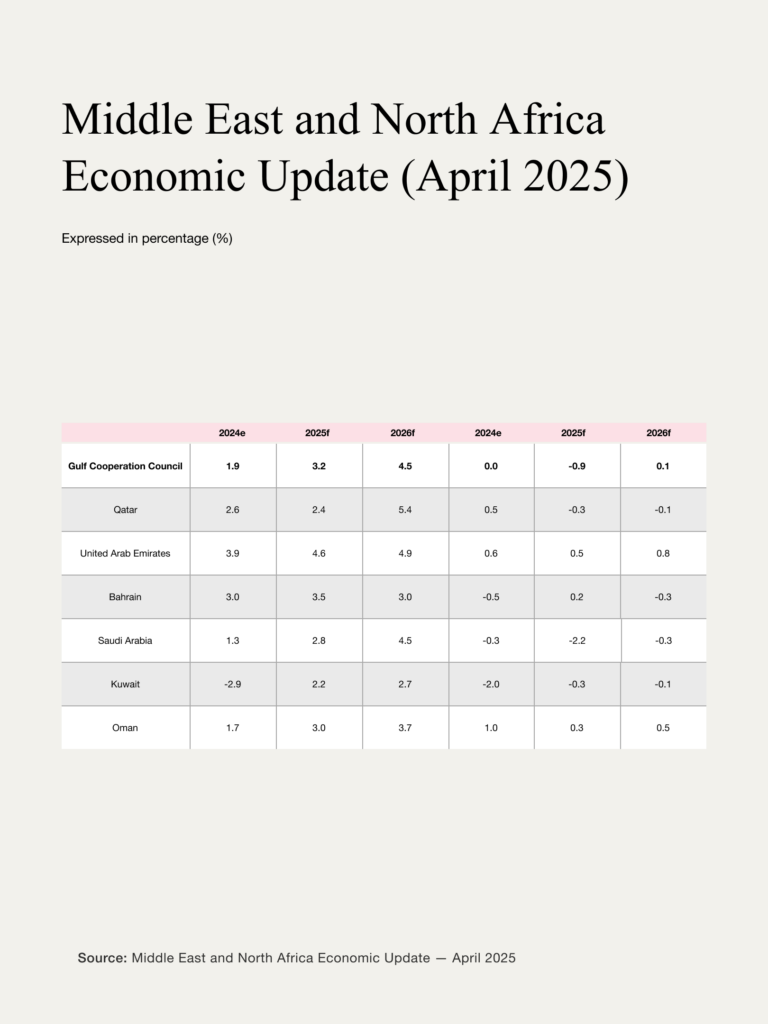

The fluctuation in oil prices directly influences regional economic performance. After virtually stagnating at just 0.4% growth in 2023, GCC economies saw modest recovery (1.9%) in 2024, primarily driven by favourable oil prices rather than structural economic reforms. However, since early 2025, oil prices have declined by more than 11%, restraining further economic development and leading to increasing national debt. Although typically low, debt levels vary notably within the GCC. Kuwait’s debt is just 7.1% of GDP, whereas Bahrain’s substantial debt level, at 134% of GDP, represents a striking regional anomaly.

Future oil price outlooks remain pessimistic due to several factors. Notably, Donald Trump’s “drill, baby, drill” strategy targets a $60 per barrel oil price, much to the discomfort of Arab leadership. Trump’s protectionist tariffs also threaten to induce a global economic slowdown, thereby depressing global demand for energy further and lowering prices. Additionally, geopolitical strategies aiming to use oil as leverage against Russia have forced OPEC members to boost production, depressing prices and intensifying the economic pressures on Russian oil producers.

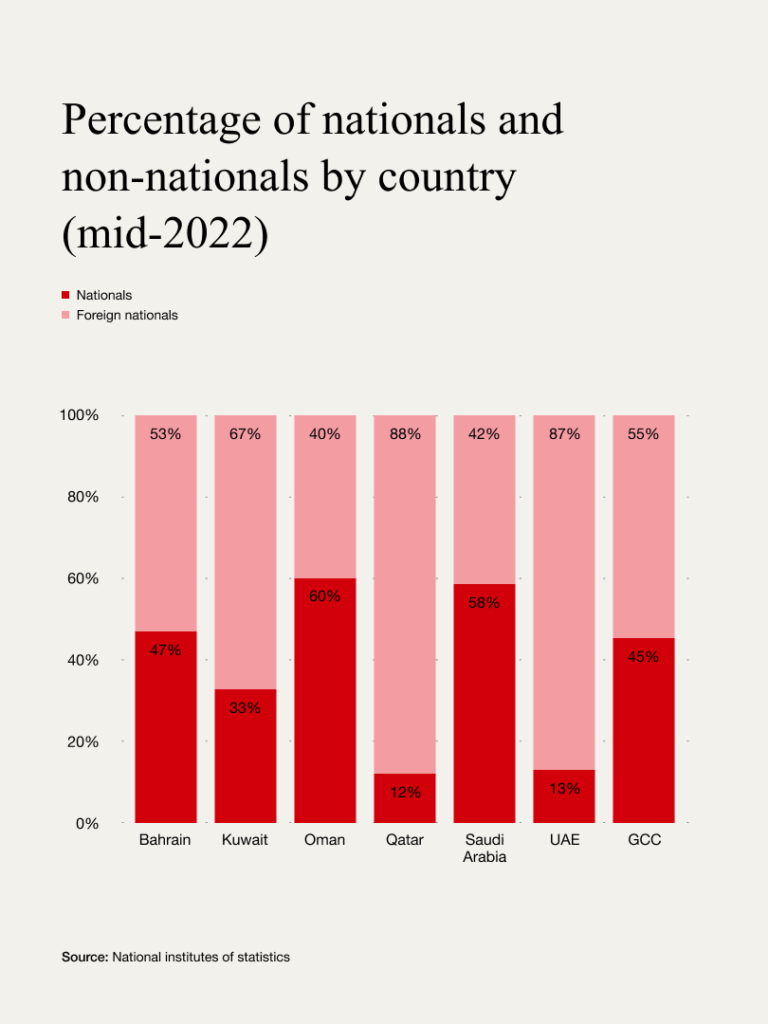

Another shared characteristic among Gulf countries is their heavy reliance on foreign labour, essential to sustaining their economies. In Qatar, migrants constitute more than 88% of the workforce, whereas Oman, with the lowest share, stands at around 40%. Beyond the familiar challenges of poor working conditions and inadequate labour protections—conditions migrant workers often tolerate in pursuit of better pay—the region faces an additional complication: a reliance on transient labour without deep social integration. Building a sustainable private sector, capable of liberating the region from dependence on oil subsidies, demands more than merely importing talent. The crucial step is supporting local entrepreneurs who, motivated by patriotism or long-term commitments, are willing to invest in the future in which they and their families aspire to live. Without such vision, the private sector risks remaining nothing more than a mirage in a desert of oil revenues.

How will Gulf countries navigate an extended period of lower oil prices? Sustained price downturns could slow or stall ambitious diversification plans. The United Arab Emirates has made significant progress: while Abu Dhabi remains oil-reliant, Dubai has successfully diversified its economic base into trade, tourism, and financial services, reducing oil dependency to just 10% of GDP. However, whether the entire Arabian Peninsula can similarly diversify remains uncertain, given differing levels of commitment and capability.

Oil as a Prosperity Trap

Unlike wealthy GCC monarchies, Iraq and Iran face unique challenges. Wars and sanctions have constrained their oil potential, yet oil remains the backbone of their economies. Iraq, producing approximately 4.1 million barrels daily, exemplifies a troubling paradox: abundant oil revenues diminish incentives for necessary economic reform.

The Iraqi government confronts the formidable task of economically integrating a population long accustomed to conflict. It has chosen to leverage oil income to create public-sector employment, resulting in a significant budget deficit of $49 billion and the addition of over 600,000 state jobs. While beneficial for social integration, this approach has inflated an inefficient public sector overly reliant on fluctuating oil revenues. Any sustained downturn in oil prices could severely challenge Iraq’s ability to sustain such employment levels.

Economic opportunities outside of oil and state employment remain scarce. Agriculture contributes modestly to GDP, with date exports as the primary commodity. Industries such as cement manufacturing in Sulaymaniyah predominantly cater to domestic demand without significant export potential.

Navigating Self-Reliance Amid Sanctions

Iran’s economic landscape differs significantly, shaped predominantly by international sanctions, particularly from the United States. Despite these constraints, Iran maintains daily oil production between 1.3 and 1.4 million barrels, mainly exported covertly to China. Longstanding sanctions since 1979 have compelled Iran toward increased domestic self-sufficiency. Non-oil sectors now account for 80–85% of GDP, with agriculture (notably pistachio exports) contributing over $1 billion annually. Manufacturing industries, exemplified by automaker Iran Khodro’s production of 500,000 vehicles per year, satisfy substantial domestic demand.

Iran’s historical strength in mathematics underpins innovations, including a financial system circumventing restricted access to international banking networks like SWIFT. Technological advances, particularly drone production, bolster Iran’s geopolitical standing, despite economic hardship characterized by inflation reaching 38.9% in April 2025 and persistent geopolitical threats.

A Hidden Economic Treasure

The economies described above share an ambition to adapt to a future where oil’s importance diminishes. Yet, responses remain stereotypical—investments in tourism or expanded state employment. A critical shortcoming is the absence of an environment conducive to independent private-sector enterprises free from state subsidies and oil revenues. Another significant issue is the low rate of innovation, often relying on imported talent from abroad. Female employment remains particularly low—5% in Yemen, 11% in Iraq, 15% in Iran, and 36% in Saudi Arabia—highlighting substantial untapped growth potential. The region’s true wealth may lie not beneath the sand, but beyond its patriarchal norms.

Statement

Oil has financed dreams and disasters in the Middle East, forging cities like Dubai while hollowing out war-torn states like Iraq. But the region’s addiction to hydrocarbons has stifled reform, entrenched elite privilege, and tethered national survival to volatile global markets. Saudi Arabia and Qatar cling to oil-funded visions while unemployment surges. Iraq turns petrodollars into public payrolls instead of industry. Iran innovates under sanctions but remains isolated and inflation-ridden. Across the region, female labor and private enterprise remain chronically underused.