From Vietnam’s humming factories to Laos’s debt-laden stagnation, ASEAN showcases dynamism and dysfunction in equal measure, oscillating precariously between industrial hardship and technological luxury in a region that is home to 670 million people. Can it leverage its youthful population and diversity to overtake ageing economic giants, or will its internal disparities and dependencies prove debilitating?

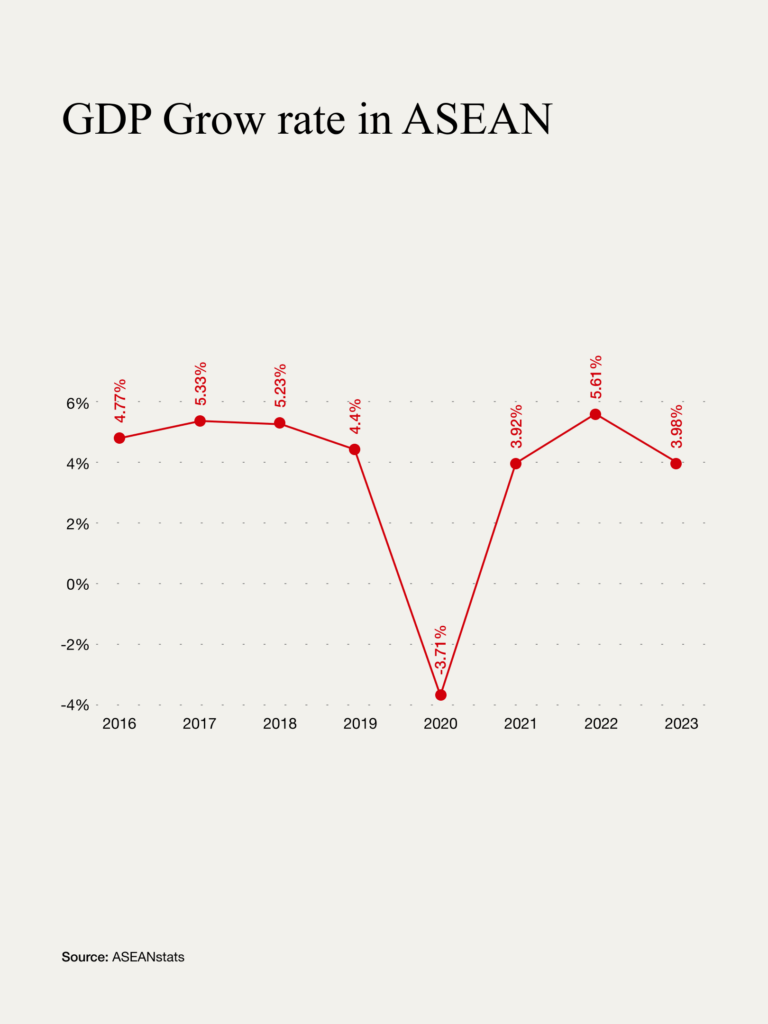

The Association of Southeast Asian Nations (ASEAN) is a diverse economic bloc with a combined GDP exceeding $3.8 trillion, ranking as the world's sixth-largest economy in 2025. While trailing behind India ($4.27 trillion), Japan ($4.18 trillion), and Germany ($4.5 trillion), ASEAN maintains steady growth rates of 3–5% annually. By contrast, Germany experienced only 0.4% GDP growth, while Japan’s economy shrank by 0.2% in early 2025.

Diversity is ASEAN’s core advantage. Rapidly growing economies such as the Philippines (6.1%) and Vietnam (6.0%) are absorbing manufacturing operations from China, whereas Singapore remains a global financial centre. ASEAN’s momentum places it in direct competition with India’s robust 6.5% growth. Beyond GDP figures, the region vies for investor favour through structural reform and sectoral strengths.

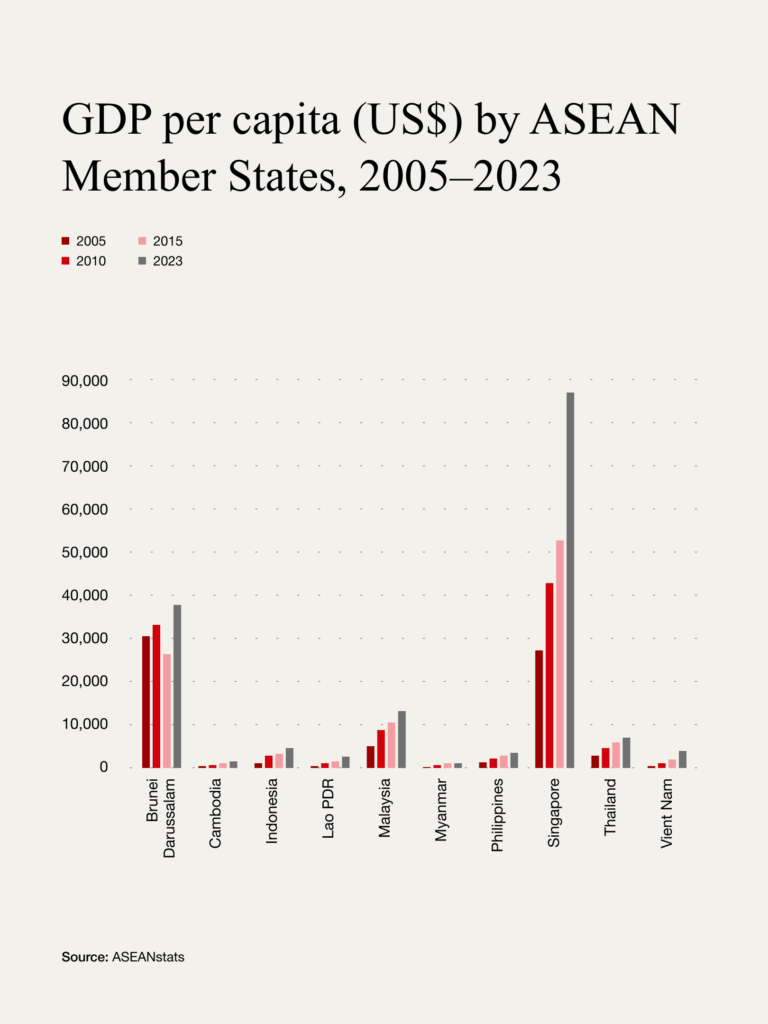

Singapore offers ASEAN a strategic advantage. Even amid economic shifts favouring developed economies, Singapore, boasting a per capita GDP exceeding $84,000, provides the region with economic stability. On paper, ASEAN has all the ingredients necessary to be decisive in the coming decades. Nevertheless, behind impressive numbers lie stark realities: Diversity fuels dynamism but frustrates unity. Myanmar's political crisis, which slashed GDP by 10% in 2021, starkly contrasts Vietnam’s industrial boom, and Laos grapples with a looming debt crisis largely unnoticed by its neighbours. Can ASEAN reconcile these tensions?

Ten Countries, Ten Economic Models

Let’s not forget: ASEAN comprises ten countries, each with its distinctive character and economic structure. Despite its vast diversity, the region lacks a unified identity beyond geographical proximity. If common interests remain elusive, one may at least discern shared characteristics among subsets of these economies.

The first group consists of countries banking their future on natural resources. For Brunei, this means oil, which represents around 60% of its GDP, creating an acute dependence that forces economic diversification. Sultan Hassanal Bolkiah seeks to transform his nation into a “startup nation“. In 2020, Brunei launched the Digital Economy Master Plan 2025, but despite ambitious objectives and substantial investment, its ranking in the Global Innovation Index 2024 has not improved, placing it at 88th, just behind Botswana and Egypt - a sobering position for a nation seeking to reinvent itself. Indonesia and the Philippines rely significantly on nickel exports but share a common vulnerability: underfunded infrastructure. This deficiency inflates extraction costs and prevents these countries from capitalising on their considerable mineral wealth.

The second group consists of countries that have become magnets for manufacturing investment. Vietnam stands out prominently, having consistently posted stable annual growth rates of 6–8%. The country has successfully diversified its economy, making strides on multiple fronts, primarily driven by electronics exports, which are expanding by more than 15% annually. Malaysia is a global leader in semiconductor production, holding a 13% share of the international market for semiconductor testing and packaging. Thailand, too, falls into this category as it seeks to offset declining tourism revenues by developing its automotive sector. However, this ambition faces significant hurdles amid elevated US tariffs introduced during Donald Trump’s administration.

The third cluster includes countries confronted by severe economic and social challenges. Myanmar suffered a GDP contraction exceeding 10% after the military coup in 2021, coupled with a humanitarian crisis and soaring inflation. Cambodia attempts to sustain itself through textiles, but this industry alone cannot service its debt to China, which surpasses 50% of its GDP. Laos similarly struggles under a hefty national debt and double-digit inflation, posing risks to its economic stability.

Distinct from these clusters stands Singapore, often dubbed the “Switzerland of Asia“. It shares numerous attributes with Switzerland: stability, low crime rates, meticulous order, and a sophisticated financial sector. However, its high living costs render it less accessible to lower-income groups.

Stability and Cooperation: Keys to ASEAN’s Future

Against this backdrop, it becomes clear: ASEAN’s potential rests on two critical factors—political stability and intra-regional cooperation. The Singaporean model of managed democracy could inspire ASEAN nations seeking equilibrium between stability and openness. Additionally, confronting shared challenges—such as the US tariffs—could catalyse deeper cooperation, unifying markets currently fragmented by political divisions.

Ultimately, ASEAN’s future hinges on leaders stabilising domestic politics and prioritising regional integration over national interests. Should ASEAN unite effectively against global pressures, from American tariffs to Chinese debt diplomacy, it could emerge as a robust counterbalance to established Asian powers.

Statement

ASEAN stands at a fault line—poised between promise and paralysis. Its $3.8 trillion economy grows steadily, yet beneath headline figures lies a region fragmented by ten competing models. While Vietnam and the Philippines surge ahead, Myanmar collapses and Laos teeters under debt. Singapore anchors the bloc, but its sheen can’t mask ASEAN’s lack of cohesion. Rising US tariffs, China’s economic reach, and internal inequality test its unity. Can ASEAN transcend its structural discord to rival ageing giants like Japan and Germany—or will it remain a study in unrealised potential? If ASEAN continues to mistake proximity for partnership, it will drift into irrelevance - quietly, inevitably, like a boat unmoored. But with strategic unity, it could outgrow its giants - not just by numbers, but by design.