When Donald Trump entered the White House again in 2025, his robust plan to reshape American foreign trade via aggressive tariffs threw macro-economic forecasts into turmoil. Estimates of GDP growth, inflation, and trade balances, which global economies had relied on for years, suddenly became obsolete. Economists, divided along partisan lines, began debating methodologies and lost their firm footing. Trump’s actions underscored a timeless truth: even the most refined economic models cannot tame human unpredictability.

Yet, in the long term, another narrative emerges—paradoxically, one of stark predictability. Demographic data, unlike fluctuating economic forecasts, offer clear, almost relentless certainty. According to the United Nations, people aged 65 and older comprised 9.3% of the global population in 2020; by 2050, this proportion will climb to 16%.

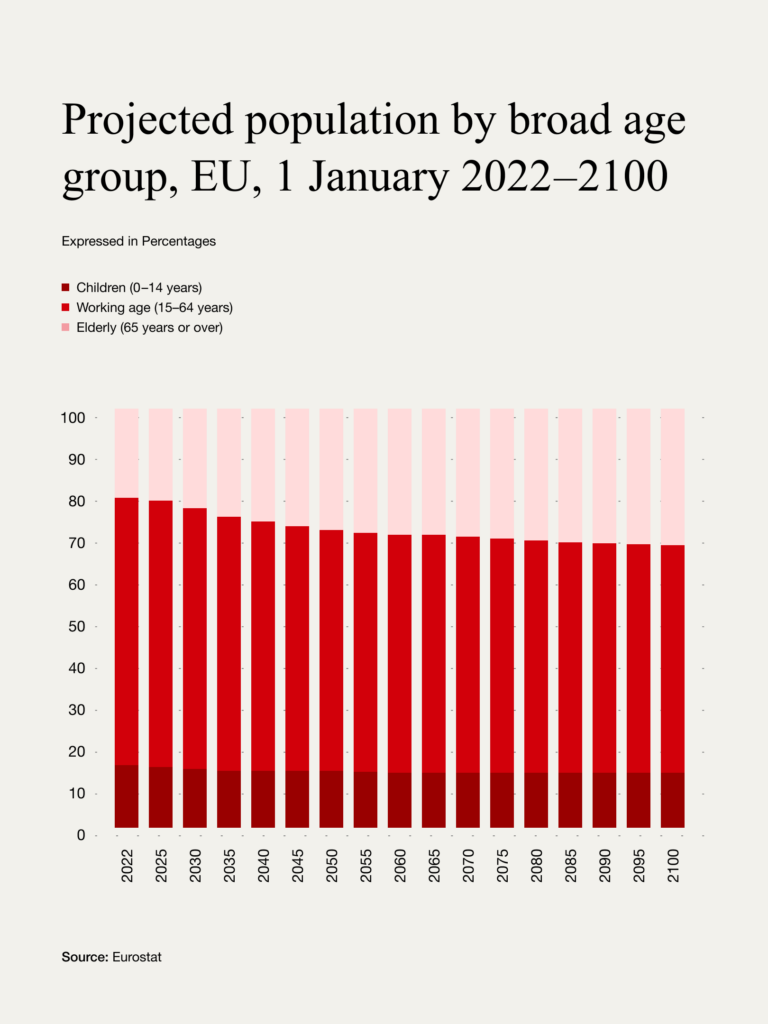

Europe's situation is even more alarming: seniors currently constitute roughly one-fifth of the population; within a quarter-century, they will represent nearly one-third. With an average fertility rate of 1.5 children per woman—far below the replacement level of 2.1—Europe is heading towards a demographic trap. Yet Europe is not alone; Japan has already trodden this path. Clearly, this trend is unsustainable. The crucial question is how we can prepare for this inevitability.

Ageing Populations

To grasp the economic impact of an ageing population, consider the numbers. A 2016 study by Maestas, Mullen, and Powell suggests every 10% increase in the proportion of the population aged over 60 reduces per capita GDP growth by 5.5%. While the exact figures can be debated, the trajectory remains indisputable. With age, people's capacity to generate economic value diminishes, and their contribution to GDP growth declines. Simultaneously, their capacity for consumption falls. Given that Western economies rely heavily on domestic consumption, this presents a formidable barrier to sustained growth.

The lifecycle theory, developed by Franco Modigliani and Richard Brumberg in the 1950s, assumes people rationally base their consumption on lifetime resources. Younger people (under 30) tend to save or incur debts, for example, to purchase homes. Middle-aged individuals (35–50) reach peak consumption due to higher incomes and family expenditures. Consumption declines in senior years (65+) as people live off savings or pensions. This theory carries macro-economic implications: population or income growth boosts savings rates, while an economy without growth simply redistributes wealth between generations. Children are not merely a source of life fulfillment but also a genuine economic asset to any nation. Thus, an ageing population presents two major problems: declining production and consumption.

Reality of the Demographic Problem

At first glance, demographic challenges might seem a distant future concern—perhaps around 2050. However, they are already at our doorstep. From a millennial’s viewpoint, it might still sappear remote, but the reality is starkly different. Looking at the working-age population, Europe has lost over 30 million people aged 15–64 from 2010 to today from the workplace—approximately 2 million fewer workers annually. This is already a critical issue for many European firms.

Admittedly, the unemployment rate in the eurozone remains relatively high, standing at 6.2% in April 2025. However, the unemployed often lack the skills or motivation required to replace retiring workers. Consequently, companies seek alternatives such as robotics and artificial intelligence. Significant expectations are placed on humanoid robots, with Tesla, Figure AI, Unitree, and UBTech actively pursuing advancements. This isn't distant speculation but imminent reality: Tesla intends to deploy Optimus robots for electric vehicle production this year, planning mass production by 2026 with an approximate price tag of $20,000 per robot. Although Elon Musk frequently misses deadlines, technological solutions clearly exist. Yet a vital question remains: who will these robots produce for?

Who Will Consume?

The deeper problem lies in consumption. Biologically, older people naturally consume less. Japan, where adult nappies outsell those for children, exemplifies this consumption transformation. The argument that increased healthcare spending among the elderly could boost GDP isn't a sustainable solution. French sociologist Emmanuel Todd consistently argues that GDP inadequately assesses economic problems, as it treats primary and tertiary sectors equally. Higher healthcare turnover doesn't contribute to national wealth as effectively as primary-sector activities. An ageing population will thus lead to a harsher GDP decline than mere nominal reduction suggests.

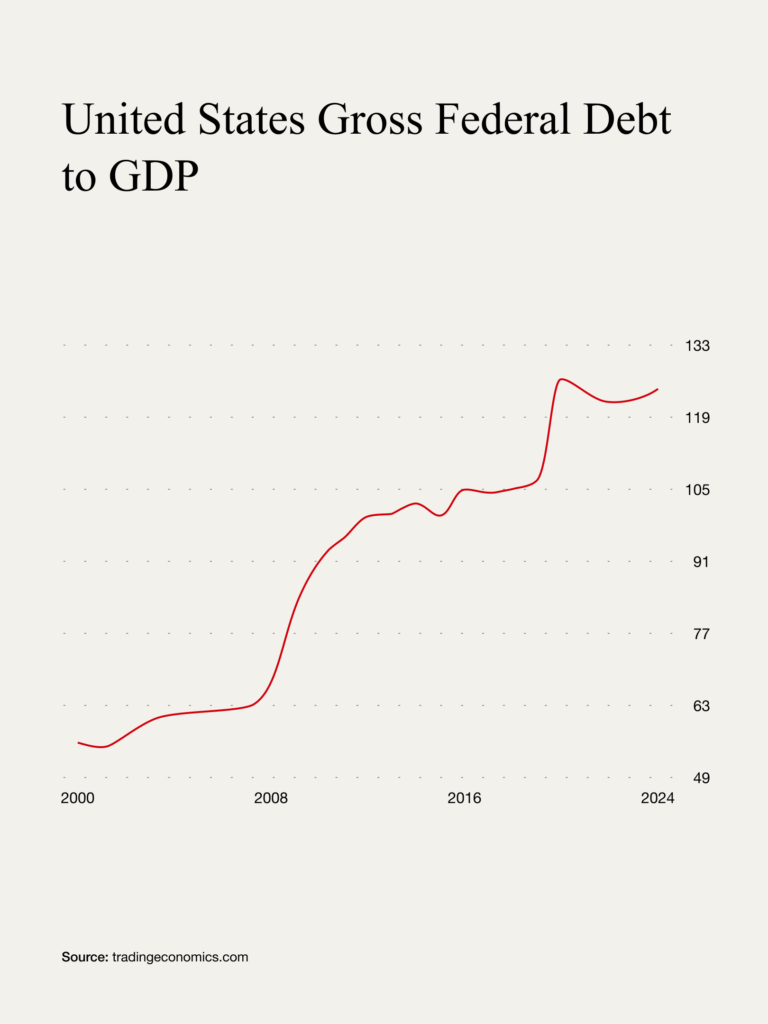

Moreover, lost growth potential affects bond markets significantly. Western nations carry heavy debts—the US debt-to-GDP ratio is nearing 120 % in 2025, while the eurozone hovers around 90 %. Persistent budget deficits since the Covid-19 pandemic are reaching 4–6% annually, driven by ever increasing mandatory expenses, notably pensions. Investors tolerate high debt only if growth potential is evident. With escalating indebtedness, higher interest rates inevitably ensue, pushing nations towards debt traps. Trust in system sustainability declines, potentially shifting abruptly into distrust.

Yet opportunities exist. Western economies leveraged demographic dividends and integrated China and Eastern Europe into global capitalism, redistributing wealth to poorer nations and the profits of global corporations.

Reduced European workforce availability and rising Asian wages complicate outsourcing, intensifying pressure for fairer wealth distribution between Western and Asian economies.

Governments ignore these demographic realities at their peril. The genuine crisis isn't abrupt collapse but slow, quiet stagnation.

Statement

Trump's return to power and disruptive tariff policies vividly remind us that economic forecasts struggle to grasp human unpredictability. Yet beneath this turmoil lies a stark inevitability: the global demographic crisis. Europe's plunging fertility rates and rapidly aging populations point to severe economic stagnation, where shrinking workforces cripple both production and consumption. Despite technological hopes like robots entering factories, a deeper question lingers: who will sustain demand when aging societies consume less? Without strategic interventions and wealth redistribution, Western economies risk quiet, persistent decline. The demographic time bomb is no distant threat—it's a crisis already reshaping our present.