If anyone was previously unaware of the importance of the Strait of Hormuz for the stability of global oil and gas markets, the recent attack on Iran will have dispelled any doubt.

The narrow sea route connecting the Persian Gulf with the Indian Ocean, which is only about 34 kilometres wide at its tightest point, is not only crucial for energy supplies. Its near hermetic closure has also disrupted exports of a wide range of other key raw materials.

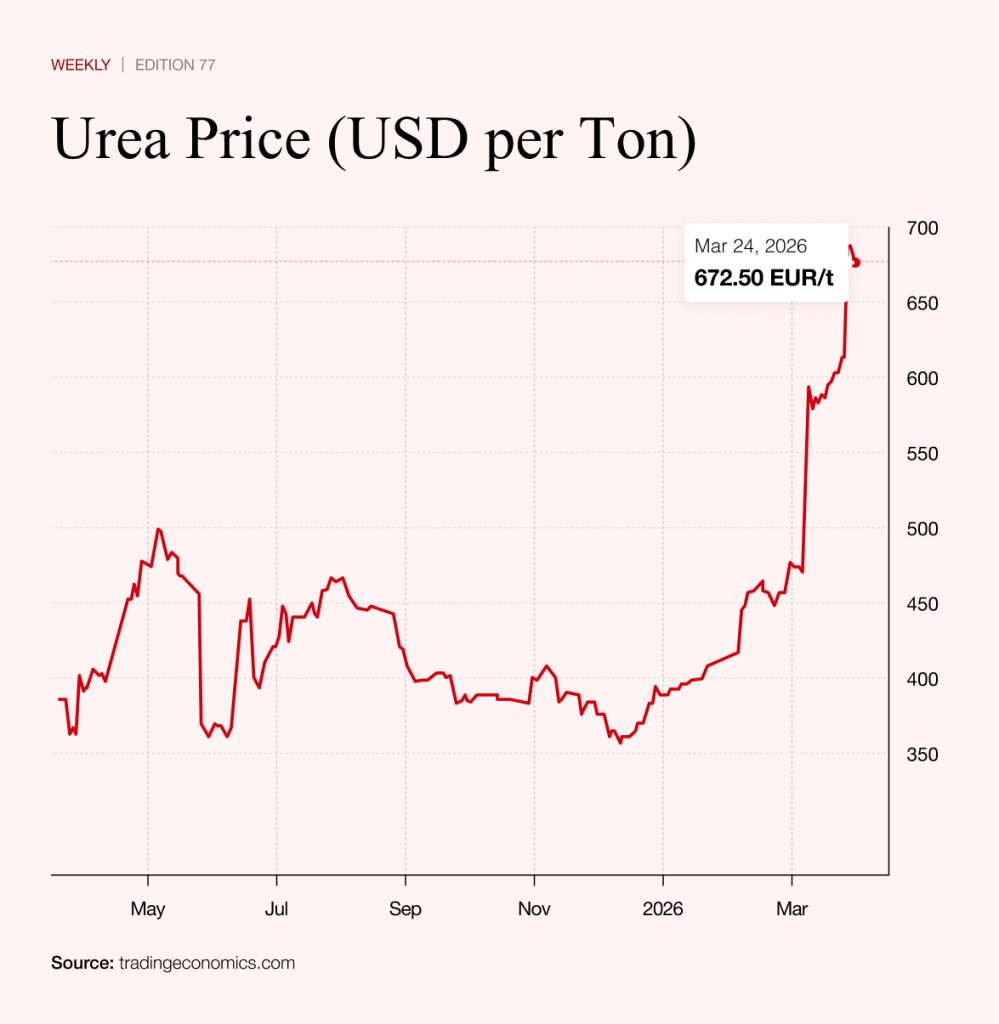

Fertiliser is in short supply, leading to a price boom

One of the sectors hit hardest is agriculture, primarily due to soaring fertiliser prices.

Gulf countries account for roughly a fifth of global supply of commodities such as ammonia, phosphate and sulphur. In the case of urea, their share approaches 50 per cent. Since the outbreak of the Iran conflict, its price has risen by nearly half.

Analysts at the Carnegie Endowment for International Peace estimate that the conflict is disrupting around one fifth of global trade in phosphate fertilisers. Sulphur, a by product of oil and gas processing, is also essential for their production.

With the war affecting about 45 per cent of the sulphur market, many countries could soon struggle to produce phosphate fertilisers if the situation persists.

A similar dynamic applies to nitrogen fertilisers, which are even more important. Crops rely on nitrogen for protein synthesis and photosynthesis. These fertilisers dominate global usage, accounting for nearly 60 per cent of the market. Without them, soil fertility could fall by an estimated 40 to 50 per cent.

Around 10 per cent of the world’s gas supply comes from the Middle East, and gas is the key input in producing synthetic nitrogen fertilisers. Producers now face both shortages and sharply rising costs.

In Europe, gas prices have increased by about 70 percent since the start of the war in Iran. At certain points, the price nearly doubled. The exact figure fluctuates depending on the latest reports from the Middle East, the price is extremely volatile.

A clear example of negative impact is Duslo Šaľa, a Slovak fertiliser producer, which has already reduced some ammonia production due to high gas prices.

Bad timing for food production

The timing could hardly be worse. The Centre for Strategic and International Studies notes that nearly half of global nitrogen fertiliser consumption is used for staple crops such as wheat, rice and maize.

‘Higher fertiliser prices will affect crop choice,’ Joseph Glauber of the International Food Policy Research Institute, IFPRI, told Deutsche Welle, adding that farmers are likely to switch to less fertiliser-intensive crops.

In poorer countries in particular, farmers may simply reduce fertiliser use altogether, which would depress yields. The strain will be felt even more acutely as spring planting begins and demand naturally rises after winter.

Consumers are therefore likely to feel the effects indirectly, as higher input costs are passed through to food prices. Rising fuel costs will add further pressure.

‘First it will be higher energy and fertiliser prices, which will then have a knock-on effect on transport and food prices, until eventually it is reflected in supermarkets,’ Carsten Brzeski, chief economist at ING Germany, told Politico.

If the Strait of Hormuz is reopened by the end of March, he said, the impact would still be felt by farmers and consumers, but would remain ‘short-term and manageable’.

How much more expensive is food going to be?

Few analysts are willing to offer precise estimates of the impact of the Hormuz blockade on food prices. However, one figure cited by Joseph Glauber is telling: energy accounts indirectly for about 50 per cent of food production costs.

Oxford Economics has raised its forecast for global food price growth from below one per cent to around two per cent. Martin Hudcovský of the Slovak Academy of Sciences has suggested a similar magnitude. A sustained 10 per cent rise in energy prices could translate into a roughly 2.5 per cent increase in food prices over time.

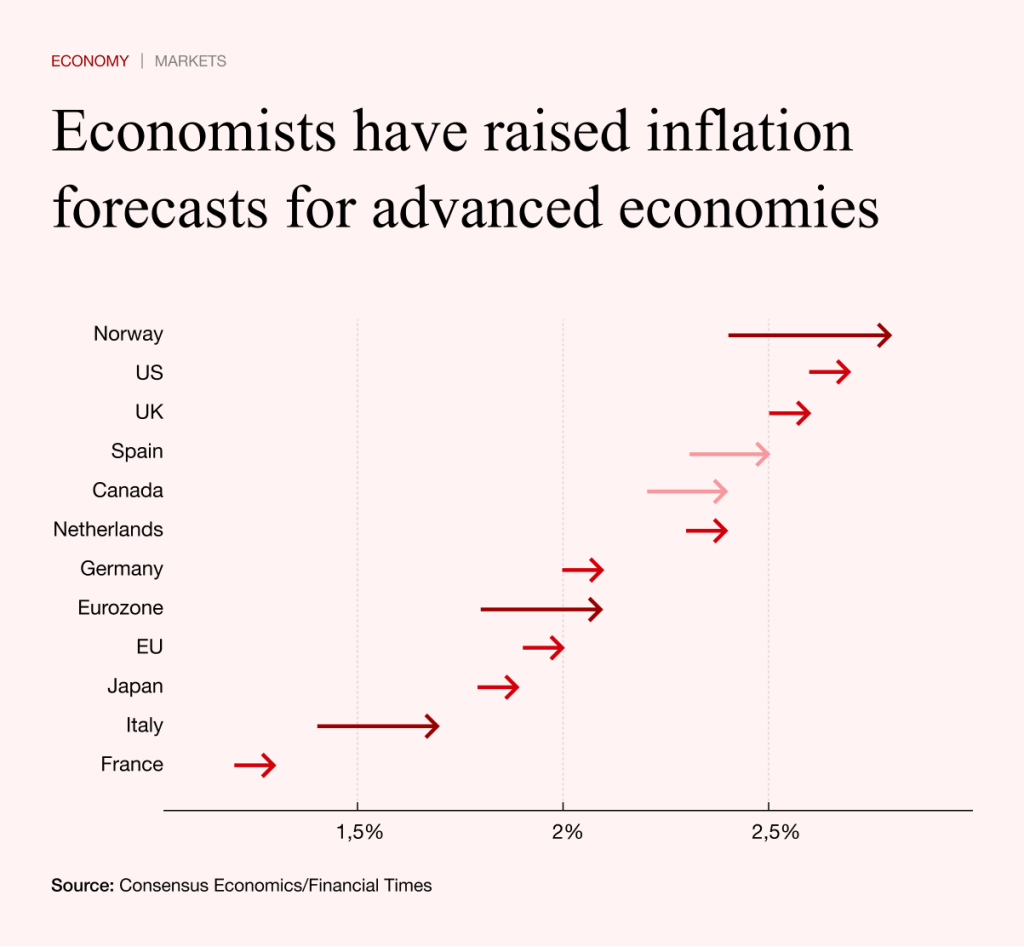

Inflation expectations are also shifting. According to economists, the blockade could add 0.2 to 0.3 percentage points to US inflation in the final quarter of the year. In the eurozone, the increase could reach half a percentage point, and more than one point in Italy.

Consensus Economics has already revised its euro area inflation forecast for 2026 from about 1.8 per cent to 2.1 per cent, even though the conflict has so far lasted less than three weeks.

Rising inflation expectations also raise a critical question: whether central banks will respond by tightening monetary policy again, potentially slowing economic growth. With each additional day of conflict and disruption in the strait, that risk continues to grow.