Economic exchange between the European Union and Iran has become a peripheral phenomenon, at least at first glance. With trade totalling €3.72 billion in 2025, the relationship has fallen to a level barely visible in macroeconomic aggregates. Yet the contraction is not simply a loss of importance. It reflects a strategic realignment: politically driven, enforced through regulation and far from inconsequential economically.

Anyone who strikes Iran from Europe’s trade statistics underestimates how modern markets function. Relevance is not determined by volume alone, but by integration into systems. And in that respect, Iran remains a factor.

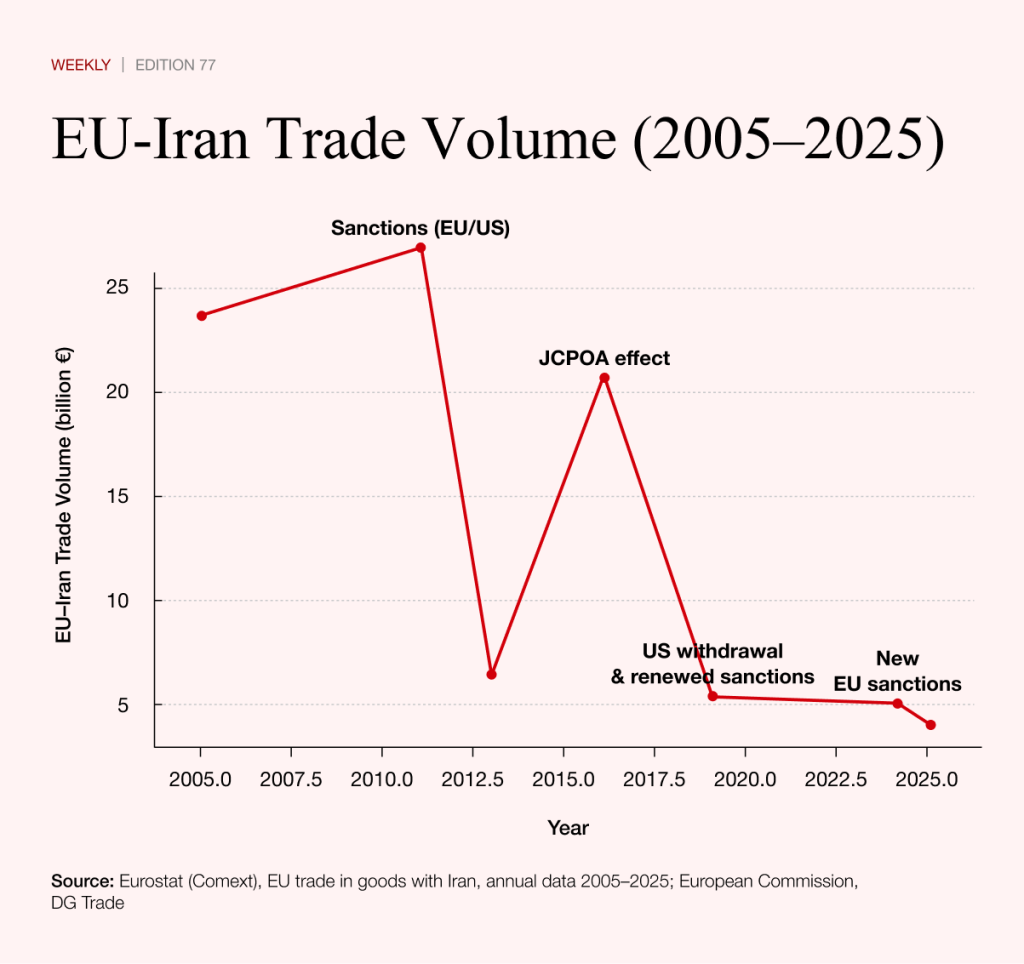

The long retreat from what was once a functioning market

At first, the figures paint a clear picture. In the mid-2000s, EU–Iran trade stood consistently in the tens of billions. In 2005, the volume reached €23.8 billion, peaking at more than €27 billion in 2011. The structure was conventional: Europe exported industrial goods, while Iran supplied energy and raw materials.

Sanctions imposed from 2011 marked a structural rupture. Within two years, trade had almost halved, falling to just €6.1 billion by 2013. The brief recovery following the 2015 nuclear agreement, driven by hopes of economic opening, pushed volumes back up to €20.7 billion. Yet the effect proved temporary.

Since 2019, the decline has been steady and politically determined. New US sanctions, European restrictions and mounting geopolitical tensions have systematically thinned out economic ties. The latest EU measures in early 2026 – citing human rights violations and military support for Russia – are less a turning point than a continuation of that trajectory.

The result is a de facto decoupling. Iran no longer plays a structural role in Europe’s external trade. Yet the reduction has altered the nature of the remaining ties. Within the sharply diminished exchange, a striking concentration has emerged. Germany accounts for 31.8 per cent, followed by Italy and the Netherlands with just over 15 per cent each. Together, the three countries represent nearly two-thirds of all EU–Iran trade.

That distribution is no coincidence. It reflects industrial specialisation. German companies primarily supply machinery, plant equipment and chemical intermediates – goods that are difficult to replace in existing Iranian production processes. The trade is less about growth than functional necessity: spare parts, maintenance technology and specialised components.

Italy and the Netherlands operate in comparable niches, with the Netherlands also serving as a logistical hub. The exchange is highly selective and, in many cases, protected by regulatory exemptions for specific categories of goods. The breadth of earlier trade relations has disappeared. What remains are targeted, often technically defined flows.

The structure of goods flows: more than pistachios

A closer look at the goods involved reveals how profoundly the relationship has changed and how differentiated it remains, despite its modest scale.

On the export side, machinery and transport equipment dominate, along with chemical products. Together, the two categories account for well over 60 per cent of EU exports to Iran. Behind them lie highly specialised industrial supply chains: production facilities, components for existing infrastructure and chemical intermediates for downstream industries.

On the import side, the picture appears simpler at first, but proves more layered on closer inspection. The largest share consists of food and live animals, accounting for around 37 per cent of imports. Food products are relatively straightforward: pistachios, dates, saffron and other agricultural goods traded in Europe as premium or speciality items. They are not essential for basic supply, but are well established in specific market segments.

The category of ‘live animals’ is more complex. It does not involve bulk shipments for meat production, but highly specialised segments such as breeding programmes, the trade in genetic material or the exchange of animals for agricultural optimisation and research. In some cases, it extends to niche markets such as falconry or specialised livestock breeding lines. Volumes are limited, but economic significance lies in quality rather than quantity.

Further categories include chemical products and so-called ‘manufactured goods classified chiefly by material’, a broad grouping covering items such as metal products or basic industrial goods. Non-fuel raw materials play only a minor role. Overall, the picture is one of fragmented residual interconnection rather than conventional foreign trade.

Systemic effects: why small trade can have large consequences

Iran’s true importance for Europe no longer lies in these direct trade flows. It stems from the country’s position within global markets, particularly in energy and raw materials.

A fundamental economic principle is decisive here: markets for key commodities such as oil and gas are globally integrated. Even if Europe imports little Iranian energy directly, any disruption in the region affects global pricing. Those price movements act as a multiplier. Rising energy costs increase industrial production expenses, drive up transport and logistics costs and feed directly into inflation. Energy-intensive sectors such as chemicals, metals and semiconductors are particularly sensitive.

A second channel operates through fertilisers. Their production is heavily dependent on gas. Rising energy prices increase production costs, which in turn feed into higher agricultural costs and ultimately into food prices.

A third factor concerns the transaction costs of global trade. Conflict in the Gulf raises insurance premiums for shipping, lengthens transport routes and injects uncertainty into supply chains. Such effects are difficult to quantify, yet carry significant economic weight.

The result is a paradox for the European Union. Direct economic dependence on Iran has been reduced successfully. Yet indirect vulnerability remains – and in some respects has even increased.

While bilateral trade can be shaped by political decisions, global market mechanisms largely escape control. Sanctions can limit direct exchange, but cannot neutralise the systemic effects of a geopolitically significant actor.

The shift has clear strategic implications. It forces Europe to think about economic security not only in terms of trade, but in terms of resilience: diversification of energy sources, stability of supply chains and the reduction of systemic risks.

More than energy: the hidden fault lines of industry

Beyond oil and gas, the growing vulnerability of global supply chains is also becoming apparent in critical industrial gases. In Germany, there are increasing indications of a tightening supply of helium, a strategically important resource for medical technology, semiconductor manufacturing and high-tech industries. According to industry sources, major suppliers such as Linde and Air Products have recently tightened their delivery policies significantly, increasingly prioritising system-critical applications. For industrial customers, that means reduced availability, longer lead times and rising uncertainty in production processes.

At the same time, there are mounting signs of strain in the hydrogen market, with in some cases noticeable price surcharges. While these developments have so far only been partially confirmed officially, they fit into a broader pattern: the stability of modern industry depends not only on energy in the narrow sense, but on a wide range of highly specialised material flows. When one of these critical points comes under pressure, the effects propagate far beyond individual markets.

A case study in modern geo-economics

EU–Iran trade is now small, selective and heavily regulated. Yet precisely in that reduction lies its analytical significance. It shows how political decisions shape economic relationships and how limited the impact of such interventions can be in a globally interconnected system. Iran is no longer a key trading partner for Europe. But it remains a node in a network whose dynamics extend far beyond bilateral ties.