The sovereign bond market functions primarily as a confidence indicator. If a country is well governed, inflation is low, public finances are balanced and debt is manageable, lenders are happy to provide money at low interest rates.

Many investment institutions are therefore willing to lend against what is known as collateral. The market is far more rational than the stock market.

That does not mean it is entirely free of emotion, or that every move is governed by precise calculation. It is such a vast market that its direction is determined by the biggest players, who do not act recklessly but with mathematical precision.

A Market That Punishes Fantasy

The bond market also acts as a reality check for politicians. If large institutions conclude that a borrower may be heading for trouble because of reckless behavior, yields start to rise. That makes it a highly reliable instrument of coercion.

Rising yields create serious problems for indebted states. Governments have to accept that borrowing will cost them more. In itself, that would not be an obstacle. Countries borrow all the time. The problem is that sovereign bond yields also affect the rates at which banks lend, and that quickly becomes political.

There is a risk that the property market grinds to a halt. The wider economy slows because money becomes more expensive, while financial markets come under pressure. The bond market can therefore put today’s politicians in serious trouble and, over time, destroy them politically.

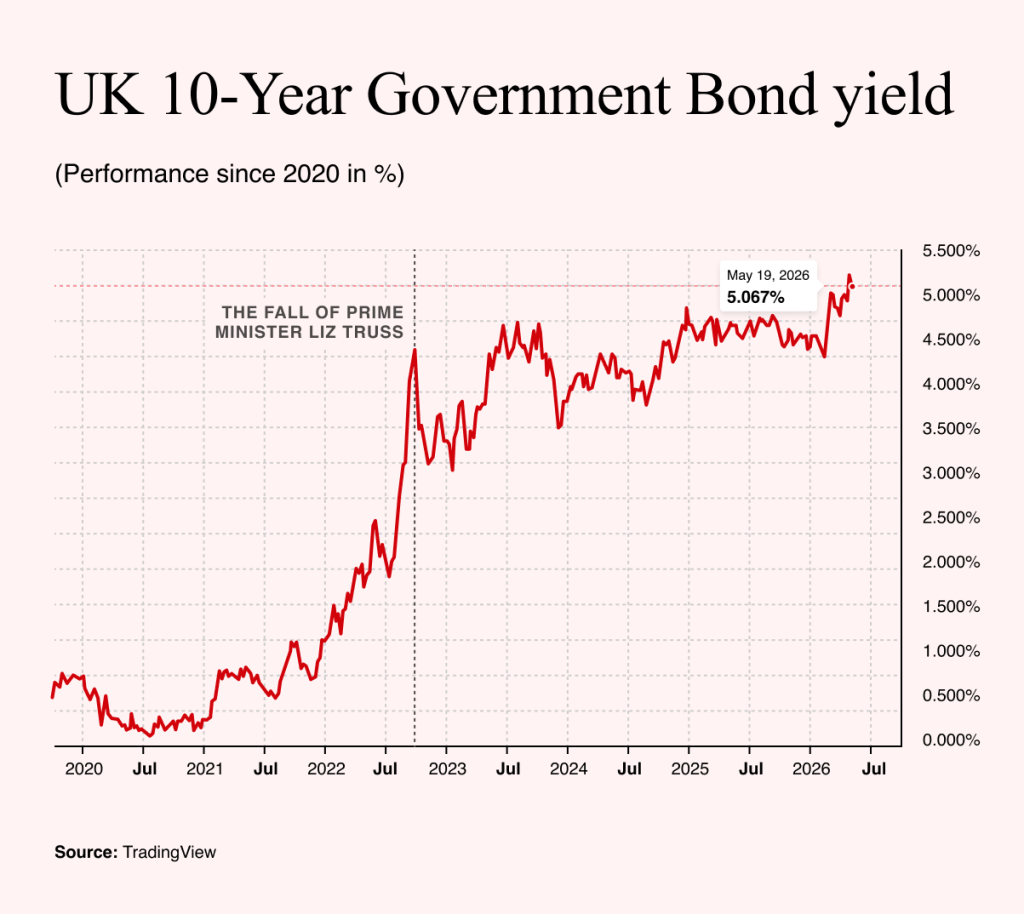

The British Lesson and the Fall of a Government

Liz Truss knows something about this. When she became British prime minister in 2022, her government proposed major tax cuts. Kwasi Kwarteng, then Chancellor of the Exchequer, called it a mini-budget, but in reality it was a radical fiscal experiment. The government wanted to cut taxes while also providing major support to households facing high energy prices. The problem was that it did not explain how it would pay for those measures.

The bond market reacted immediately. Investors began selling British government bonds, pushing prices down and yields sharply higher. The market sent the government a clear message: it did not believe its promises. Because UK bond yields also affect mortgage and loan rates, the issue quickly turned from an accounting debate into a political crisis.

The situation was made worse by pension funds whose strategies were partly tied to long-term bonds. The sharp rise in yields forced them to sell other assets, deepening the panic further. Eventually, the Bank of England had to step in and start buying bonds to calm the market.

For Truss, it meant the end. First she had to sacrifice the chancellor. Then his successor cancelled most of her program. Finally, she resigned. Her premiership lasted only 45 days. In her case, the bond market was not merely a confidence indicator. It was a direct political guillotine.

After Truss, British prime ministers began to behave like politicians who knew full well that the bond market was constantly watching them. Rishi Sunak did exactly what the markets expected and effectively reversed her agenda.

He returned to a familiar policy of caution, aimed not at solving the immediate problems facing the British public, such as the high cost of living, but above all at preserving the existing system. The country therefore could commit neither to massive borrowing nor to typical socialist profligacy. Sunak mainly maintained the status quo.

Unsurprisingly, that policy failed with voters, and Sunak eventually handed power to Starmer. The bond market at least rewarded him by pushing British bond yields below 4%.

When Even Fiscal Discipline Is Not Enough

But that was not the end of the story. What at the time looked like an extraordinary crisis for one prime minister has gradually become the normal condition of British politics. Starmer came to power with the opposite promise to Truss. He did not want to unsettle the markets, but to reassure them. His government spoke of responsibility, discipline and stability. Yet even that has proved insufficient.

UK bond yields are now even higher than they were under Truss. The yield on the 10-year British bond stands at around 5%, higher than at the height of the panic after her mini-crash. Thirty-year bonds have risen even further and, in recent days, approached levels not seen since the late 1990s.

That does not mean Starmer is another Truss. The difference lies in the speed and the cause. With Truss, it was instant punishment for a single ill-conceived budget experiment. The market saw unfunded tax cuts and reacted with panic. In Starmer’s case, the problem is slower and deeper. This time, the market is not saying that one government decision was insane. It is making clear that Britain’s overall fiscal position is extremely tight.

Britain has high debt, weak growth, elevated interest rates and huge spending commitments that will be very difficult to cut. The state has to borrow constantly, while the comfort of an era in which money was almost free has long since disappeared.

The Limits of Political Power

So while the bond market has not yet brought down Starmer, the guillotine stands ready. Every new promise, every hesitation and every budget doubt can translate into higher yields in a flash. Higher yields mean less money for politics itself. They mean less room for social spending, investment, tax breaks and support for households.

That is probably the biggest change since the fall of Truss. A British prime minister can have an overwhelming majority in parliament, win elections comfortably and promise radical change. But unless the bond market trusts him, his real power is severely limited.

Truss was politically executed by the market in a matter of weeks. Starmer, for now, has merely been warned. The main risk, however, is that he does not have many cards with which to reverse the situation. He can cut spending and disappoint voters. He can spend more and frighten the markets.

Or he can hope for a miracle in the form of stronger economic growth. But even a miracle cannot solve a deep systemic crisis. It can only cover it up for a while and prolong the agony.