Surprisingly, the classics of Russian literature, including Fyodor Dostoevsky, can offer insight into what is happening in the Russian economy. The great connoisseur of the Russian soul once wrote in his diary: “The most basic, most rudimentary spiritual need of the Russian people is the need for suffering, ever-present and unquenchable, everywhere and in everything.”

The Russian economy and Russian society, in other words, tend to function best under pressure. The greater the pressure, the more society can overcome.

History has shown this capacity of the Russian people to perform under threat many times. Yet apart from periods of calm, which are especially difficult for Russian society, the approach has another drawback. For suffering to work and continue driving people towards greater performance, it must keep growing over time.

After a few years, people become used to suffering. Fortunately, that is how the human psyche works. The same pattern is now repeating itself in the Russian economy. After a phase of intense effort comes a phase of strain and attrition, while everything continues to operate in war mode.

The Limits of an Economy Under Pressure

A similar dynamic is visible today in another form. In the first years of the war, Russia’s economy did not operate like a system heading for collapse. On the contrary, it adapted. Sanctions, isolation and rising military spending did not stop it, but redirected it. The state began concentrating resources in arms production, the military and sectors linked to the war. Pressure from outside and within became a source of strength.

But a model based on pressure has limits. To mobilize further, pressure must be maintained or even increased. What provokes extraordinary effort in the first phase turns over time into fatigue, strain and exhaustion.

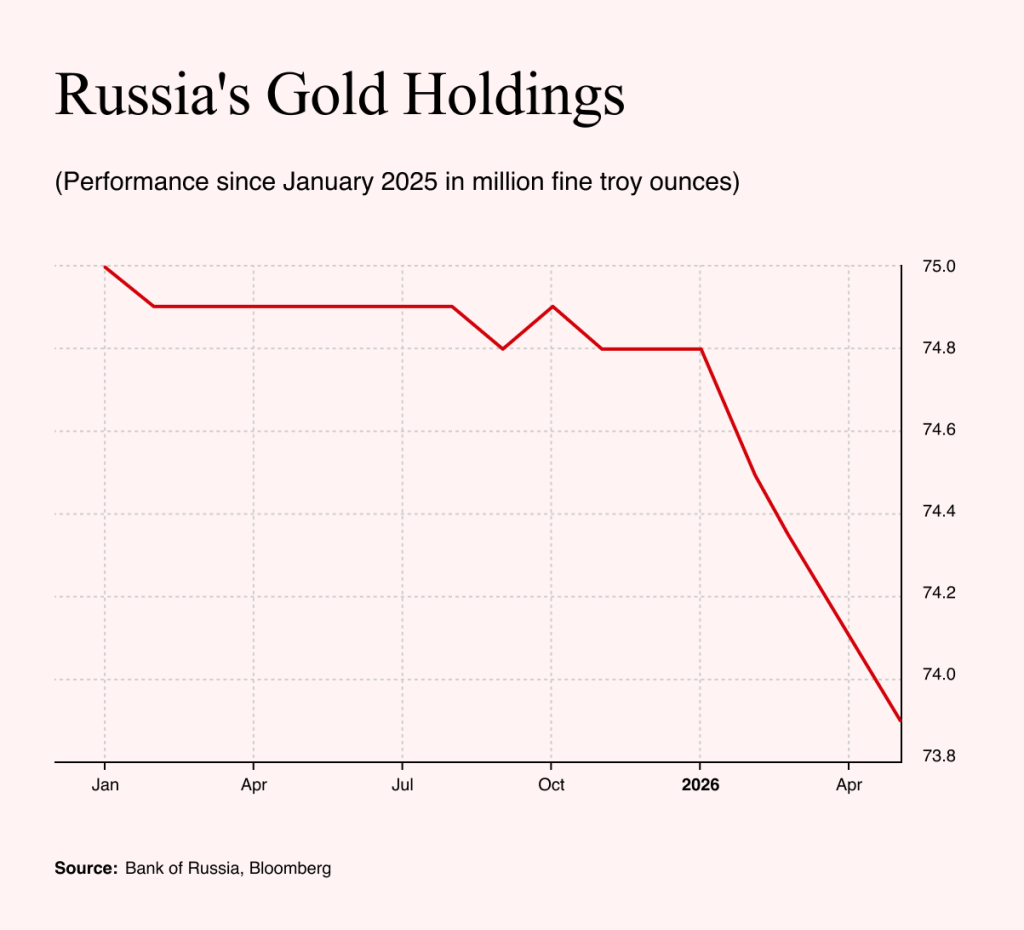

Russia’s economy has now reached a point where the war regime is still holding the system together while also beginning to expose its limits. One telling sign of the seriousness of the situation is that the Bank of Russia has reduced its gold holdings for the first time since the start of the war, selling 900,000 ounces in the first four months of 2026. The drawdown has come alongside a sharp fall in oil and gas revenues, which dropped by 38% year on year over the same period.

However, tensions around Iran have pushed oil prices higher, which will certainly help Russia. On the other hand, Russia remains largely bound by long-term contracts with its partners. Current high oil and gas prices may support the Russian economy and perhaps prevent further sales of gold reserves, but they will not free the country from its structural dependence on commodities. Those revenues are cyclical.

Russia therefore benefits less from brief oil-price spikes than from sustained high prices over time. If oil were to stabilize at $80–$100 per barrel over the next few years, that would be enough for the Russian budget to cover current spending and rebuild the treasury without drawing on reserves. The problems of the Russian economy, however, cannot be reduced to oil and gas prices alone. They are an important pillar, but not the only one.

A Disappearing Workforce and the Strain of War

At first glance, the current problem facing the Russian economy is the opposite of the one confronting many advanced European countries. Russia is not suffering from high unemployment, but from exceptionally low unemployment. The expansion of the war economy has brought the jobless rate down from about 5.1% before the war to around 2.2% today. In normal times, that might look like a sign of strength. In Russia’s case, it is increasingly a sign of exhaustion.

There are two reasons for this. Some young and economically active men have joined the army, either because of mobilization or high recruitment bonuses. At the same time, demand for workers in the arms industry and in sectors linked to war production has risen sharply. Many companies have moved to round-the-clock operations and three-shift work. What helped keep the economy afloat in the first phase of the war, namely new orders, higher wages and a sense of exceptional mobilization, is now turning into its opposite.

The problem of attrition is especially clear here. Low unemployment no longer means only that there is plenty of work. It also means that companies cannot find skilled labor, have to raise wages faster than productivity and are competing for an ever-smaller pool of available workers.

The war industry is also drawing workers out of civilian sectors, which then lose the ability to grow, modernize and sustain normal production. Although the Russian economy continues to function at full capacity, it increasingly resembles a machine forced to run without pause and without the possibility of repair.

That is not all. The main problem lies in high interest rates and the setting of monetary policy as a whole.

The Price of Saving the Ruble

The engine room of Russia’s financial defense is above all Elvira Nabiullina, the governor of the central bank. She is one of the people who prepared the Russian economy for the sanctions shock better than the West expected.

After the invasion of Ukraine triggered an attack on the ruble and the threat of financial panic, the central bank responded by sharply raising interest rates to 20%. The move was painful but effective. It helped halt the currency’s slide, stabilize the banking system and buy time.

Nabiullina was later able to lower rates gradually. But from 2023, when it became clear that the war would not be a short “special operation” but a long and grueling conflict, the logic of monetary policy reversed again.

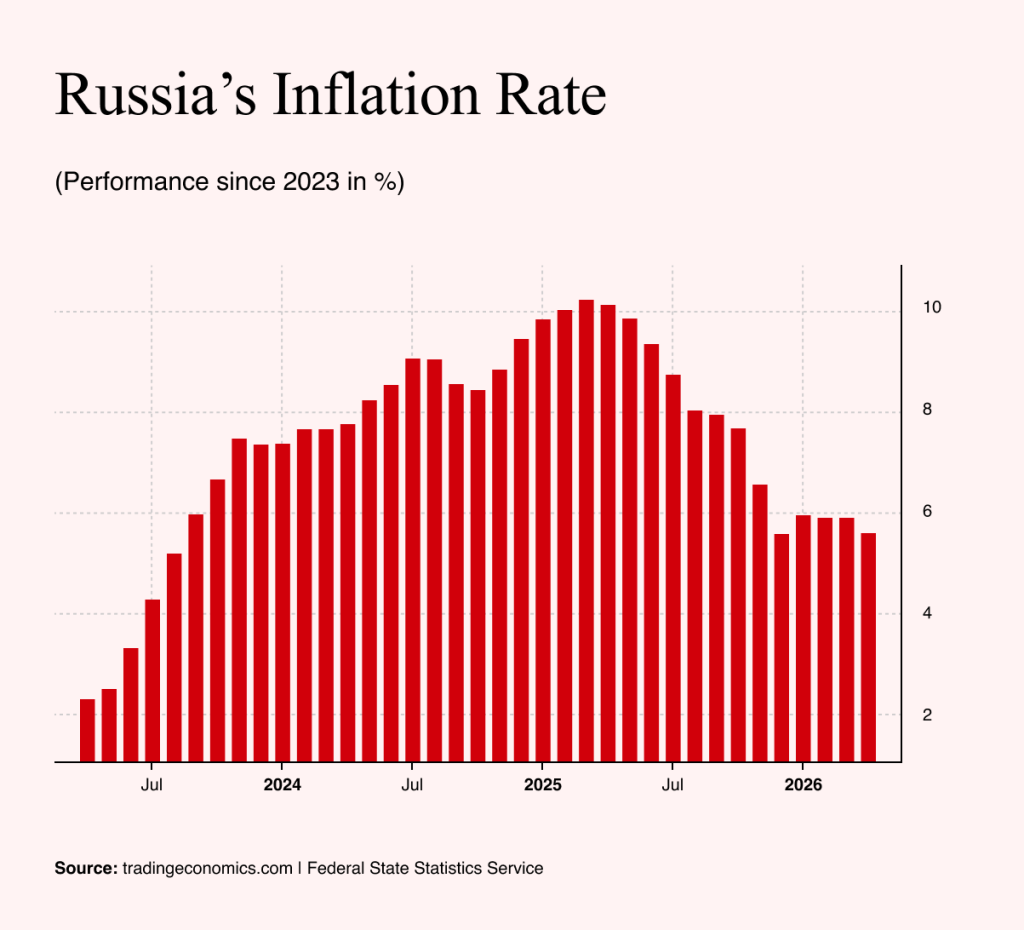

The Russian economy began to overheat. The state pumped money into the military and the arms industry, wages grew faster than productivity and inflation returned. The central bank therefore had to raise rates again to defend the ruble, dampen inflation and keep domestic savings in the Russian currency.

This is where one of the key differences between the Russian and Western economies becomes clear: debt. Russia could afford a tougher monetary policy partly because it entered the war with relatively low national debt. Even after several years of conflict, Russia’s public debt is only around 18% of GDP. This gives the central bank room to keep rates high without the immediate threat of a debt crisis that similar rates would trigger in many Western economies.

Inflation and the Cost of Expensive Money

But even this model has limits. The central bank’s current key rate is 14.5%, while inflation is around 5.6%. This creates a particular incentive for households and businesses, because it is more profitable to leave money in the bank than to spend or invest it.

In the first phase, this helps stabilize the currency and slow inflation. In the next phase, however, it begins to choke the civilian economy. People spend less, companies postpone investment and ordinary credit becomes too expensive.

The effect is most visible in the housing market. With rates so high, market mortgages are far beyond what average households can afford and often exceed 20% a year. The state is trying to ease the problem through subsidized mortgages, but even those stand at around 9% and apply only to selected groups. The result is an economy that remains nominally stable, but only at the cost of ever-greater restraint.

Nabiullina is therefore increasingly criticized in Russia for overly tight monetary policy. Yet that tightness is also one of the reasons why the Russian financial system has not yet collapsed. Therein lies the paradox of the entire war economy.

The measures that saved it in the first phase are beginning to suffocate it in the second. High interest rates are holding together the ruble and the banking system, but they are also holding back consumption, investment and normal life. Here, too, the logic of the Russian war model is repeating itself: the desire to survive at the cost of pain that must be continually prolonged.

Nabiullina did not save the Russian economy by removing that pain. She saved it by spreading it out over time. But the war has lasted too long, and the pain intended for temporary stabilization is turning into a permanent condition. Once society and the economy become used to it, it ceases to act as a mobilizing force. It no longer produces extraordinary performance, but fatigue, the postponement of normal life and the gradual wearing out of the system.