For decades, two basic factors were often enough to judge whether a property was a sound long-term investment: price per square meter and address. Market trends and buyers’ decisions were guided by those two criteria for years. They have not lost their importance, of course. Location and apartment size remain key. But basing today’s purchasing decisions on them alone is becoming increasingly short-sighted.

New factors are coming into play, including energy efficiency, renovation costs, job availability, transport links and future operating costs. Real estate is no longer just a question of location and floor space. Increasingly, it will depend on how expensive it is to live there.

The End of Metropolitan Dominance

The first major question, therefore, is where people will want to live and where they can afford to do so. Until now, the logic of the real estate market has driven capital mainly into large metropolitan areas. The reason was obvious: jobs, universities, cultural life and services were concentrated there. An address in a big city was not just a matter of prestige, but also of economic rationality.

COVID-19 showed, however, that many professions no longer require a daily physical presence in the city. In some cases, remote work has replaced it entirely. In others, it has done so at least in part. And as office work continues to change with the advent of artificial intelligence, the trend may intensify further. Work, in other words, may no longer be tied to a specific address as strongly as before.

At the same time, the concentration of labor and capital in large cities has had one obvious consequence: a sharp rise in real estate prices. For a large part of the working population, homeownership in major cities is becoming increasingly unaffordable.

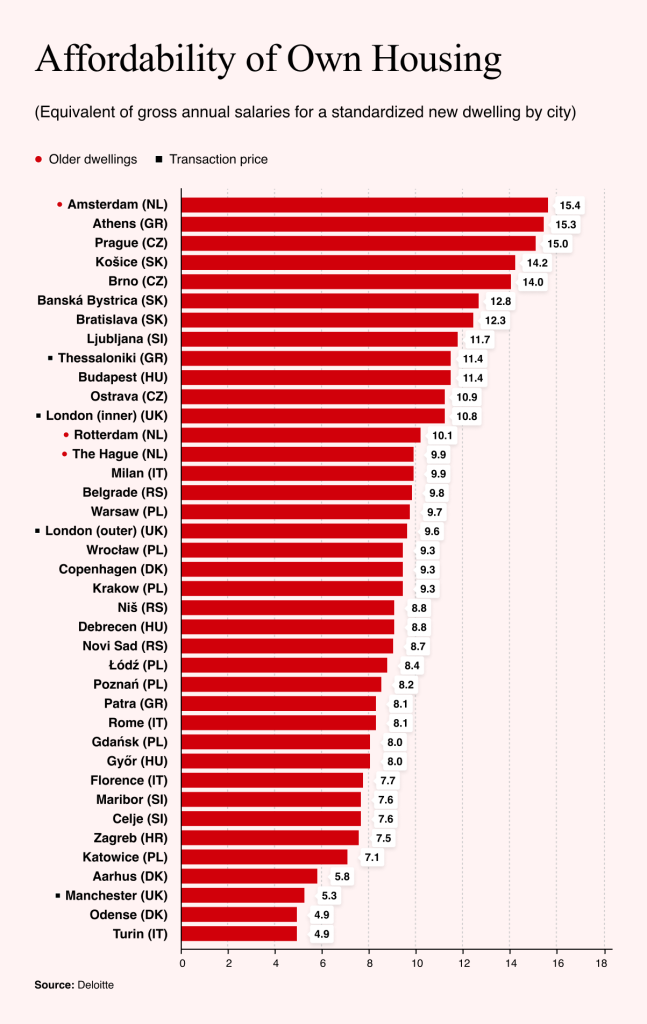

Deloitte’s regular Property Index study illustrates the point clearly. It compares housing affordability based on the number of average gross annual salaries required to buy a standardized new 70 sq m apartment.

The results are disheartening for Central Europe. Amsterdam tops the European affordability ranking, where such an apartment requires 15.4 years’ worth of salary. Immediately behind it, however, are Athens, at 15.3 years’ worth, and Prague, at 15 years’ worth. Kosice and Brno also rank very high, at 14.2 and 14 annual salaries respectively. Other Slovak cities fare little better: Banska Bystrica comes in at 12.8 annual salaries and Bratislava at 12.3.

In other words, the problem of housing affordability is no longer confined to the largest cities. In Central Europe, it is also spreading to regional centers. The first instinct, therefore, may be to leave the city and move to the countryside, where housing appears, at first glance, to be cheaper, more spacious and quieter.

The Rural Illusion Falls Apart

Yet the illusion of an affordable countryside has begun to crumble rapidly in recent years. Real estate prices have risen not only in large city centers, but across almost the entire market. At the same time, the Czech Statistical Office reports that the average price of a single-family home in the Czech Republic reached approximately €2,140 per sq m in 2024. Rural areas may still cost less than Prague or Bratislava, but they are certainly no longer automatically cheap.

There is also another problem: rural Europe has been losing residents for a long time. The Financial Times reports that between 2014 and 2024, the population of predominantly rural regions in the European Union fell by nearly eight million, while the urban population grew by more than 10 million.

The trend creates a vicious cycle. When people leave, services disappear. When services disappear, more people leave. In such an environment, shops, schools, doctors and bus services are no longer taken for granted. They become rare luxuries.

And the fewer services there are in a given location, the more daily life shifts to the car. As a result, housing that seems cheaper can become more expensive in other ways. A single-family home outside the city is not just about the purchase price and mortgage payments. It also means commuting costs, a second family car, heating a larger space, home maintenance and often expensive renovations.

That is precisely why the main winner of the coming real estate decade may not be the remote countryside, but the medium-sized city: a place that offers lower prices than a major city, while still keeping schools, services, healthcare and jobs within commuting distance, along with reasonable transport links.

The Energy Label Becomes a Rating System

Even a medium-sized city, however, will not automatically be the best choice. The second major factor is energy efficiency. The real estate of the future will not be judged solely by its purchase price, but also by how much it costs to run day to day. A poorly insulated house heated by gas or coal may seem, at first glance, like a cheaper alternative to a city apartment. In reality, however, it can become a very expensive place to live.

This is where the Emissions Trading System 2 (ETS 2), the new European emissions trading system for buildings and road transport, comes into play. Although households will not buy allowances directly, the costs will be passed on through fossil fuel prices, namely gas, coal and motor fuels. In other words, a home far from amenities, dependent on a car and costly heating, will face a double risk. It will be more expensive to heat and more expensive to leave.

Europe is already showing how energy intensity can turn from a technical specification into a legal and pricing issue. The most visible example is the French model of so-called passoires thermiques, or thermal sieves.

These are the most energy-inefficient apartments and houses, which are gradually being pushed out of the rental market. In France, it will be illegal to rent out the worst-rated Class G properties from 2025. Class F will follow in 2028 and Class E in 2034. The sale of such properties is not prohibited, but it entails mandatory audits, future renovation costs and a growing price discount.

When Cheap Becomes Expensive

This may be the most important lesson. An energy efficiency label may no longer be just another document attached to a listing. It may become a new form of property rating. A property with a good location, reasonable energy efficiency and accessible services will retain its premium value. By contrast, an old house outside the city center that depends on a car, fossil fuel heating and expensive renovations may gradually lose some of its appeal.

The housing market will therefore not merely shift from metropolitan areas to mid-sized cities. It will shift from the simple question “How much does a square meter cost?” to a much more uncomfortable one: what will it really cost to live here? The answer to that question may determine, in the coming years, which houses and apartments emerge as winners on the new real estate landscape and which become a trap.