The Iran crisis has reminded us once again that, despite all efforts toward decarbonization and the green energy transition, oil remains a crucial raw material for the modern economy. Breaking free from dependence on internal combustion engines will therefore not be easy. Today, electric vehicles appear to be the main path forward, as China has shown more clearly than anyone else.

The figures in the Breakthrough Agenda Special Report 2026 confirm the trend. The market for key clean technologies grew by nearly one-fifth a year between 2015 and 2024, driven overwhelmingly by electric cars rather than hydrogen.

Electric cars were. Battery-electric vehicles have become a mass-market product, while hydrogen cars have remained a technological dream. Interestingly, however, even high oil prices have not seriously revived the idea of hydrogen vehicles. Yet until recently, hydrogen was supposed to be the true future of the car industry.

On paper, hydrogen cars had several advantages that might have allowed them to overtake battery-electric vehicles. They were strong precisely where electric cars still reach their limits. They offered fast refueling, longer range and less dependence on batteries – and therefore on lithium, nickel, cobalt and the entire complex supply chain behind them.

Hydrogen propulsion also seemed like an ideal solution for trucks, buses and other large diesel-guzzlers, where battery weight remains a major problem in electric versions.

Hydrogen cars thus appeared to offer an elegant answer to the dilemma of modern transportation. Instead of an electric car with a heavy battery that needs to be charged frequently and for long periods, the future was supposed to bring a car with a fuel cell, a hydrogen tank and an exhaust pipe from which only water vapor would rise into the sky. It was a narrative almost perfectly tailored to the age of climate ambition: technologically advanced, politically acceptable and psychologically comfortable, because it promised a green revolution without requiring a major change in driving habits.

When Economics Caught Up with Hydrogen

But this is precisely where the gap between the allure of the technological pitch and the harshness of economic reality became clear. While the hydrogen car seemed like the ideal compromise between the old world of internal combustion engines and the new world of clean mobility, it required something that never materialized on a sufficient scale: a dense network of hydrogen refueling stations and affordable green hydrogen.

The main stumbling block was infrastructure. It had to be built almost from scratch. That was exactly where electric cars had a decisive advantage. They could rely on the existing power grid and gradually add charging stations to it. Hydrogen had to start with almost nothing.

California, long a showcase for American technology and green politics, illustrates the problem better than anywhere else. It was precisely in this wealthy state, where people could afford to pay extra for environmentally friendly solutions, that hydrogen mobility should have had a strong chance of success. But it did not.

Owners of fuel-cell cars had to accept that the grand plans for infrastructure remained largely on paper. Instead of new stations being added, some of the old ones were closing. And what good is the car of the future if you have to drive dozens of miles just to refuel it?

The Illusion of Cheap Green Hydrogen

The second reason for the failure was the price of green hydrogen itself. The original idea sounded highly convincing: surplus renewable electricity, generated when the sun shines or the wind blows, could be used to produce hydrogen and store energy for later use.

Solar plants, for example, can produce excess electricity in the summer, which was supposed to be used to produce hydrogen. The hydrogen would then be stored, transported and later used where batteries fall short. Again, it looked elegant on paper. Reality was harsher. Renewable, low-carbon hydrogen remained more expensive than hydrogen produced from fossil fuels. The market made its choice: green hydrogen was sidelined because of its price.

This is also confirmed by the Breakthrough Agenda Special Report 2026.

According to the study, low-emission hydrogen amounted to only about one million metric tons in 2025 – less than 1% of total global hydrogen production. It also says the main obstacles remain high costs, weak demand, uncertain infrastructure and the small number of projects that actually reach a final investment decision.

Even more interesting, however, is the shift in where hydrogen is now being discussed. It is no longer presented as a fuel for family cars, but primarily as a raw material and energy carrier for refineries, chemicals and the production of ammonia, methanol, fertilizers, steel or future marine and aviation fuels.

This raises a fundamental question. Was the detour into hydrogen cars merely a developmental dead end? Or did something come out of it after all?

From Car Fuel to Power Infrastructure

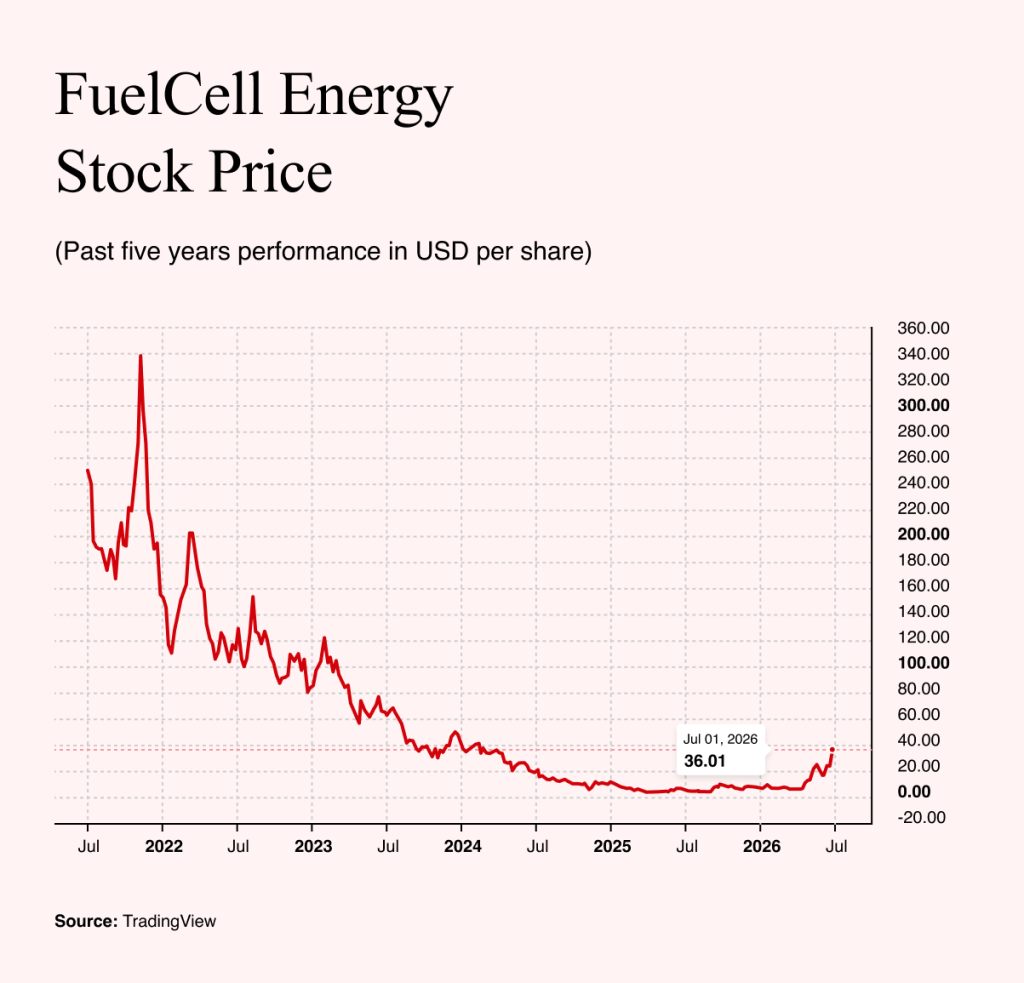

The financial markets provide the answer, specifically in the performance of FuelCell Energy’s stock. The company is not a manufacturer of hydrogen cars, but a firm that builds and operates stationary fuel cells.

In other words, it is not building the car of the future, but the small power plant of the future. Nevertheless, investors have long classified it as part of the broader group of companies associated with the hydrogen economy.

The reason is simple. Fuel cells are linked to hydrogen both technologically and as an investment theme. Through an electrochemical reaction, they convert chemical energy directly into electricity. When hydrogen is used, the byproducts are heat and water.

At FuelCell, the reality is more complex, as its systems can also use natural gas or biogas. For the stock market, however, the key labels were hydrogen, fuel cells and clean energy.

That is precisely why FuelCell rode the wave of a broader belief in an emerging hydrogen economy during the pandemic-fueled euphoria of 2020 and 2021. At the time, investors did not distinguish very clearly between manufacturers of electrolysers, fuel cells and hydrogen trucks, or companies promising green hydrogen.

It all merged into one big narrative, with clean mobility as its most visible face. Then reality set in. Hydrogen cars failed to catch on, the infrastructure did not materialize, green hydrogen remained expensive, and instead of visions, the market began once again to focus on losses, cash flow and actual orders. FuelCell’s stock plummeted along with the entire sector.

The current turnaround is therefore interesting precisely because it is not based on the return of hydrogen cars. FuelCell’s new narrative is centered on stationary fuel cells as a source of electricity for industry and data centers.

It is also a reminder of a broader shift in the green transition. The world has not entered the hydrogen age after all. It has entered the age of electricity. In the eyes of investors, fuel cells have not moved into the garage of the average driver, but to servers, factories and energy-intensive operations. FuelCell thus shows that the hydrogen narrative is not dead. It has simply moved from the auto showroom to energy infrastructure.