In August 2025, François Bayrou, the former French prime minister, appeared on TF1 television and drew attention to the ‘comfort of the boomers, who consider everything to be absolutely fine,’ despite France grappling with a colossal public debt equivalent to 118% of GDP. ‘The first victims of this situation will be the youngest French people, who will have to repay the debt throughout their lives,’ Bayrou, himself a boomer, warned.

He added: ‘We have managed to convince them that it is necessary to increase the debt further—for the comfort of certain political parties and boomers, who from this perspective consider everything to be in order.’ After a backlash, he apologised and said he did not intend to scapegoat the boomers, but had articulated an obvious truth that had long been unspoken.

This view is hardly novel. On 5 November 2019, Chlöe Swarbrick, a New Zealand MP, retorted ‘OK Boomer’ to an older colleague who interrupted her during a debate on global warming. This is not just a typical intergenerational clash but an acknowledgement, also by boomers, that boomer dominance poses an economic challenge.

Indeed, Bayrou tied his critique to escalating debt, partly fuelled by unsustainable pension spending, which reached 14% of GDP in 2024.

Economic Winners: The Boomers

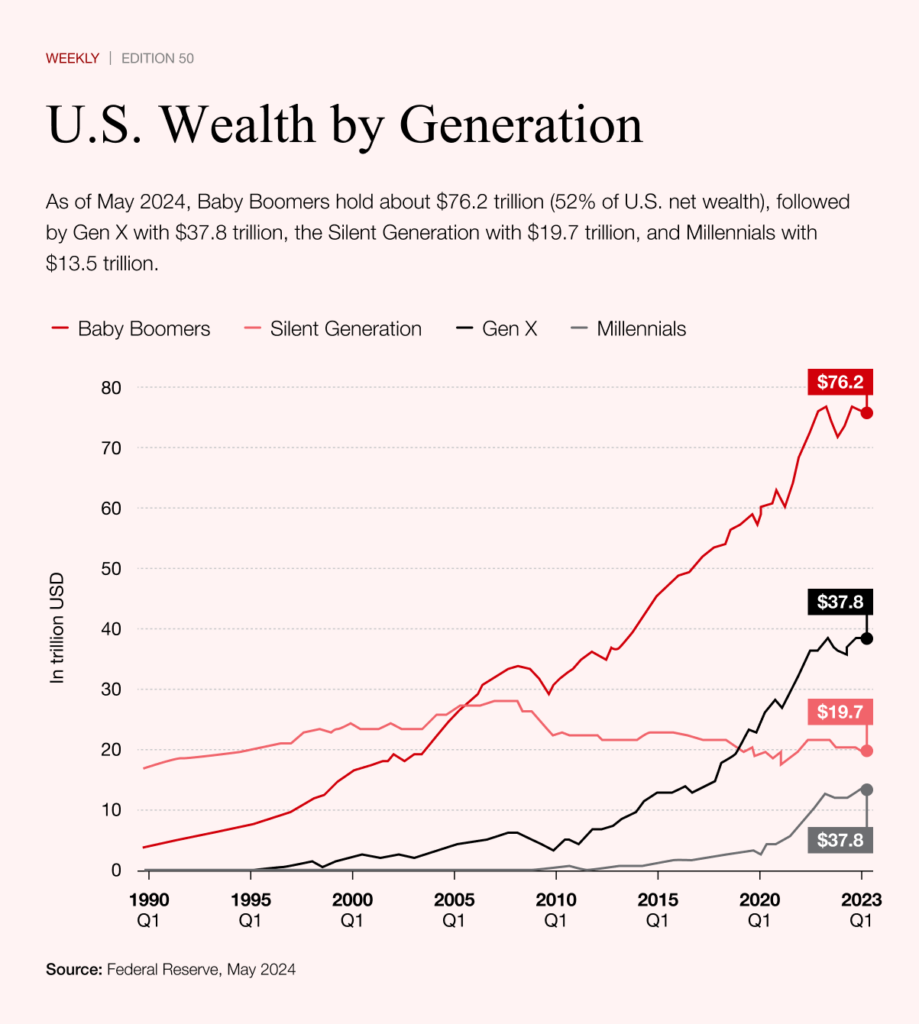

Bayrou is correct—the baby-boomer generation (born 1946–1964) has reaped benefits from the economic system in myriad ways. Intergenerational inequality is a prime factor. In America, boomers comprise only 20% of the population but hold over 52% of the wealth, totalling $82.4 trillion. Much of this stems from property, whose values have soared due to decades of low interest rates. In Britain, for instance, boomers own 70% of properties, inflating prices and restricting young people's access to housing.

Boomers also hold substantial political sway through high voter turnout (40% of voters in America), which entrenches the status quo and stymies change. This political sclerosis shaves 0.5–1% off annual GDP growth in countries with heavy boomer representation, thanks to their risk aversion and resistance to innovation.

Aristotle observed that the elderly shun risk and tend towards pessimism, whereas the young embrace it, knowing they have time to recover from setbacks. This is a natural generational tension, but pensions are an especially thorny issue. Why? In pension systems, boomers are double free-riders. Unlike property, safeguarded by ownership rights, pensions are a social compact for the common good. Seizing boomers' homes is no solution, as it would breach fundamental property rights. But pension schemes can be reformed to even out generational interests.

An Advantageous Pension System

The divide between Western and Eastern boomers is crucial. Both emerged from the post-war baby boom after the Second World War, when birth rates surged to fill the demographic vacuum. Eastern boomers, however, endured the shift from communism to capitalism, which entailed currency reforms and eroded savings. In Czechoslovakia, for example, men retired at 60 and women between 53 and 57 depending on children (per a 1965 law), while the last boomers (born 1964) retired at 64 years and 10 months. The sole common boon for Western and Eastern boomers is property ownership, though values often plummeted in the East.

Western boomers, particularly in France, profited from pay-as-you-go systems, where workers fund retirees. In the 1960s, four workers supported each pensioner, keeping contributions low. By contrast, capital-based systems—where individuals save personally—are rarer but more robust against demographic shifts. Europe's prevalent pay-as-you-go model is under strain—and France exemplifies the crisis.

France: Boomer Champion

Why has the pay-as-you-go system favoured boomers so much? Upon entering the workforce in the 1960s, the ratio was four workers per pensioner, yielding minimal deductions. This has dwindled: in 2024, it stands at 2.87 workers per pensioner, falling to 2.2 by 2030 and 1.73 by 2070. Strain intensified from 2007, as the first boomers retired.

Pensions now consume 14% of GDP, with deficits of €1.7–6.1 billion in 2024 and €6.6 billion in 2025. These figures are absolute, so stagnation or a 3% GDP recession could push the share to 14.5%. A deeper downturn might swell deficits to €12–15 billion, necessitating reforms like raising the retirement age to 65 or adopting a hybrid model.

Adding to the pressure is the exodus of young French people. According to INSEE, 100,000–120,000 emigrate annually, 60–70% of them under 35, as they chase better opportunities abroad. Their lost contributions further burden those who remain. Boomers' children, meant to fund their parents' pensions, are fleeing. With fewer payers, more claimants and mounting debt, reforms are inescapable: either extend working lives or blend pay-as-you-go with capital elements.

Without reform, France risks haemorrhaging the generation tasked with sustaining it—economically and socially. Those left behind might wryly say: ‘Merci, boomers.’

Statement

France’s baby boomers have reaped the benefits of cheap housing, generous pensions and political dominance—while leaving behind towering debt and shrinking opportunities for their children. With pensions devouring 14% of GDP, youth fleeing abroad, and the worker-to-retiree ratio collapsing, the generational bargain looks unsustainable. The real question is whether boomers will acknowledge their privilege—and give up some of their advantages—to ensure a fairer deal for those who follow.