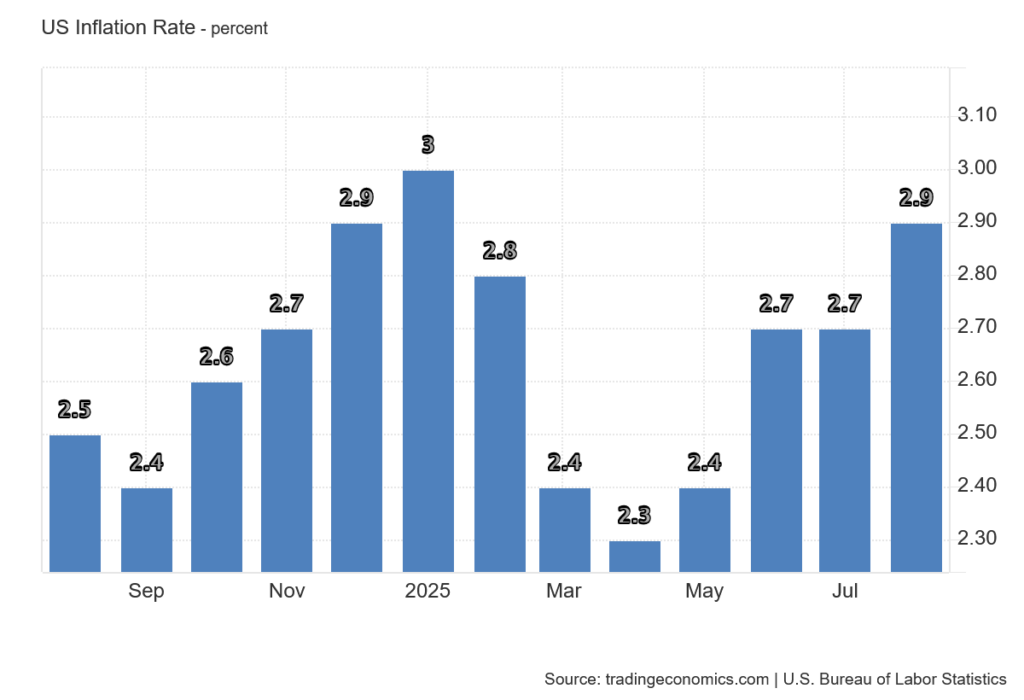

The financial markets are living their own lives, with the meeting of the US Federal Reserve (Fed) playing a key role. A cut in US dollar interest rates is already expected on Wednesday this week. The markets have successfully overcome the last hurdle, which was US inflation.

The data confirmed that overall inflation, including food and energy, rose from 2.7 percent to 2.9 percent in the US, showing an upward trend. The price increase was mainly driven by food (3.2 percent), housing (3.6 percent), and used cars (six percent).

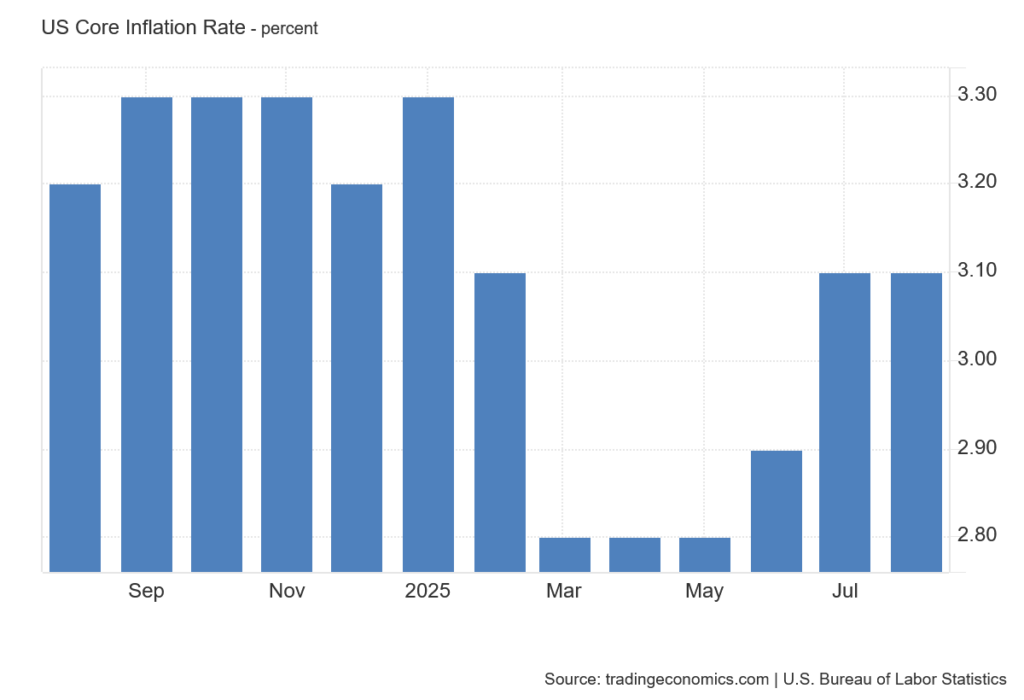

Food and housing are particularly important for low-income groups. Donald Trump is therefore on thin ice – if prices continue to rise, his electorate could become dissatisfied. It is difficult to save on food and housing, which is why price increases in these areas have a greater impact on citizens' wallets than other items. Core inflation, adjusted for the most volatile components, remains at 3.1 percent, which in itself is evidence of sustained price momentum.

The conclusion is clear: price increases in the US are accelerating, and inflation is far from over. However, this does not seem to bother the markets. From their perspective, it is important that inflation develops as expected and that nothing prevents the Fed from lowering interest rates at its meeting.

Nevertheless, the upcoming meeting is not without risks. Even if the Fed is likely to cut interest rates by 25 basis points, it will also present a forecast for macroeconomic developments in the coming months. If this forecast turns out to be hawkish, the markets could react negatively. With inflation approaching 3%, the US Federal Reserve cannot afford to cut interest rates more sharply if it wants to proceed with caution.

Every central bank governor must respect the macroeconomic data, regardless of their loyalty to President Trump. While there is room for interest rate cuts, a reduction of more than 100 basis points will be very difficult in the future.

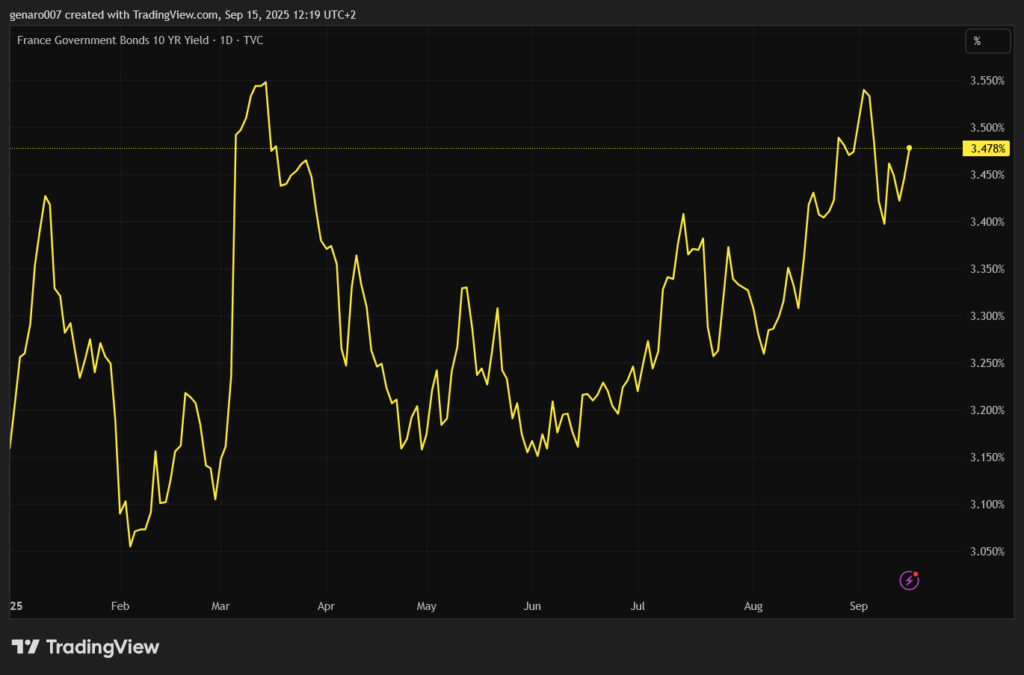

French government bonds now have an A rating

European financial markets are more or less ignoring current events on the French political stage. The most significant reaction so far has been to Prime Minister François Bayrou's announcement of a vote of confidence, which effectively led to the resignation of his government. This move came as a surprise, which probably explains the stronger reaction of the financial markets.

However, the vote of confidence and the new prime minister did not receive as much attention. The quick appointment of a new prime minister was interpreted by many as a signal to the markets that President Emmanuel Macron has the situation under control – at least on paper.

The problem is that the new prime minister has not presented a clear vision for resolving the situation. He is one of Macron's most loyal allies, and his recent moves suggest an effort to win the support of the Socialists. As a result, budget cuts will not be as severe as those proposed by Prime Minister Bayrou, who had planned cuts of €43 billion.

Given that the austerity plans cannot be implemented, the rating agency Fitch has downgraded the credit rating of French government debt from AA to A. This move was to be expected, as the agency had already indicated in its previous assessment that its internal indicators suggested an A rating, but at that time it had assumed that the government would succeed in reducing the deficit.

However, after the fall of the government, France lost its claim to this “exception.” Fitch's report was very skeptical, pointing out that the situation in France would continue to deteriorate as the country would spend more and more money on interest payments. The agency expects the current situation to continue until the presidential elections in 2027. No significant budget cuts are expected in an election year, as Macron's group wants to keep at least a theoretical chance of re-election open.

French bond yields did not react significantly to the downgrade, as the markets had already priced in this move. That is very likely. However, upon closer reading of Fitch's report, we note that this is not a light at the end of the tunnel. The situation will continue to deteriorate gradually. French bonds, French bank stocks, and insurance stocks may therefore experience market turbulence at any time once investors fully realize the economic impasse in which the French economy and the French government find themselves.

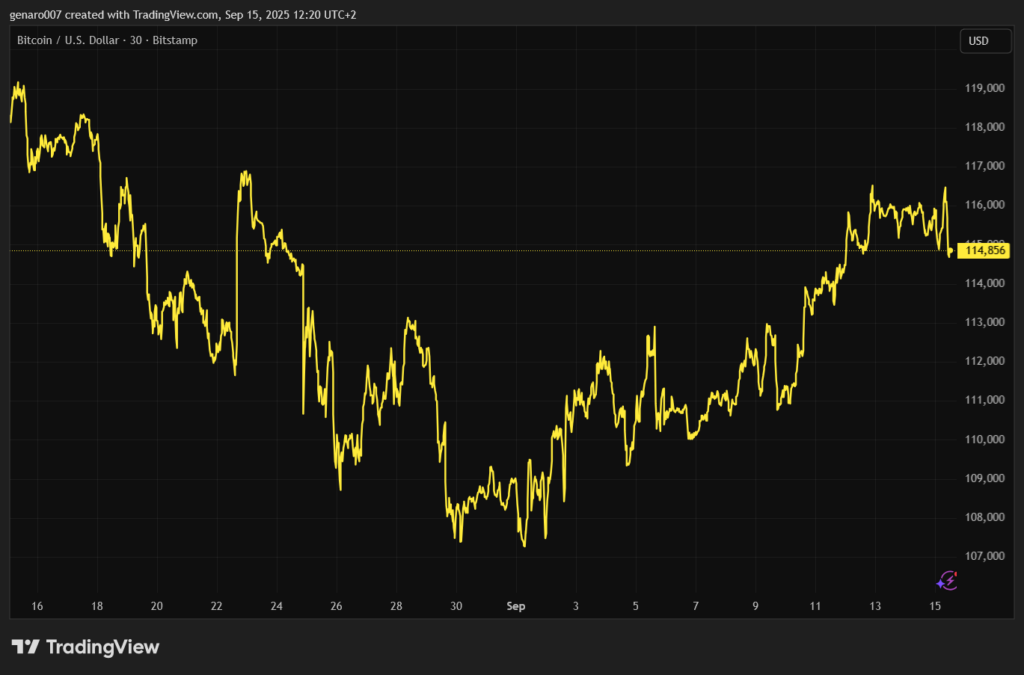

Will Bitcoin rise to another ATH this year?

Last week, Bitcoin approached the $117,000 mark but was unable to maintain this level and fell back to around $115,000. Bitcoin is thus going through a prolonged period of stagnation, which is slowly but surely testing investors' patience. The reason for this is the expectation that we will see the final phase of the halving cycle between September and November 2025.

However, some investors question this theory, arguing that investing according to halving cycles is a thing of the past, as large financial institutions have entered the crypto world. In their opinion, these have changed the dynamics of the market, so that the classic peak of the cycle, followed by a year-long bear market, may no longer occur. This possibility exists, but so far, halving cycles have mostly corresponded to reality.

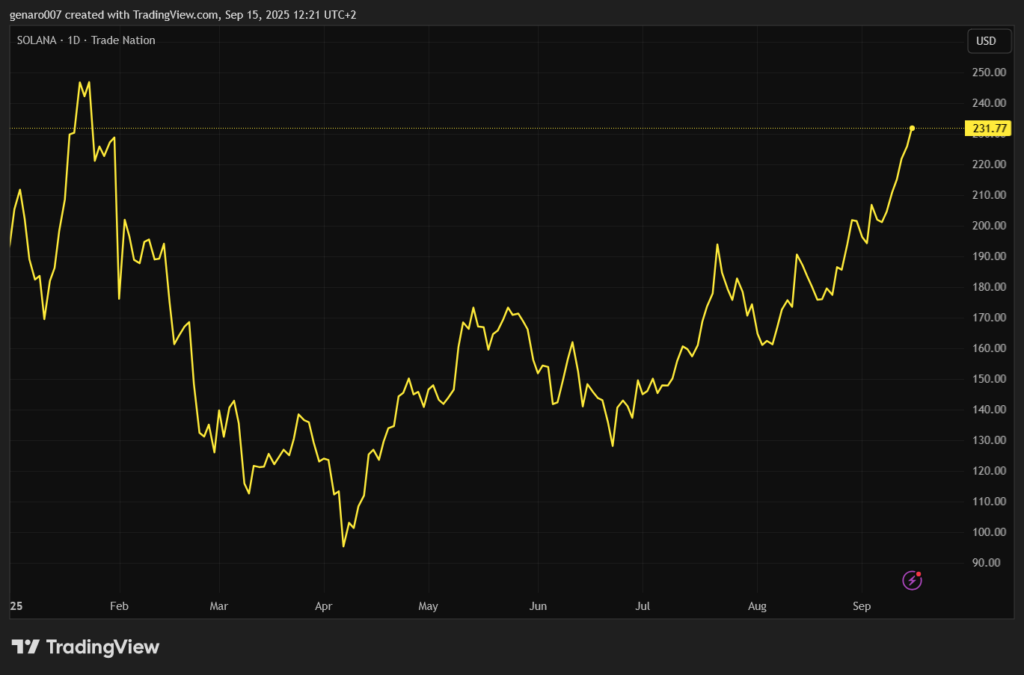

Proponents of these cycles have a strong argument: the “altcoin season” usually precedes the last major rise in Bitcoin. And this has apparently already begun. The second-largest cryptocurrency, Ethereum, gained 4.7 percent last week, while Solana rose 15.5 percent and is rapidly approaching its all-time high (ATH). Once Solana reaches its ATH, it could signal a rise in Bitcoin. The US Federal Reserve (Fed) meeting on Wednesday will play a key role in this development.

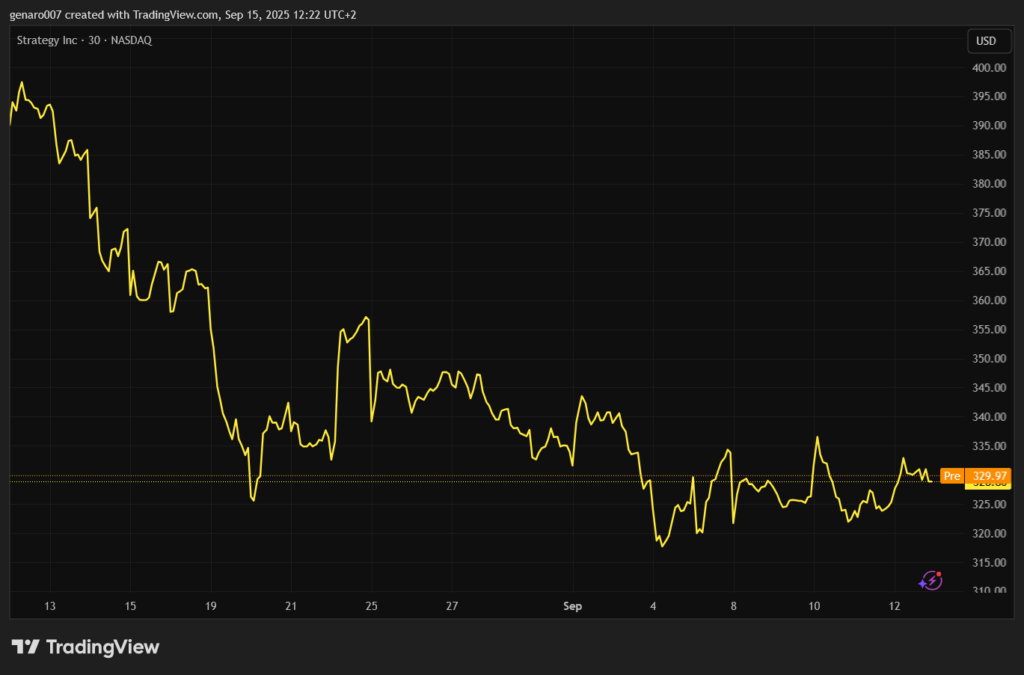

Bitcoin's stagnation in recent weeks is having a negative impact on companies that have built their businesses on the accumulation of Bitcoin or other cryptocurrencies. Strategy's shares have fallen more than 16 percent in recent months, and Metaplanet's shares have lost more than 33 percent in the last month.

The crypto market is facing a really hot fall, as any major decline could trigger a panic sell-off. Investors may start to believe that the halving cycle is over. Holding cryptocurrencies over the next three months will therefore require strong nerves.

A week dominated by central banks

The highlight of this week will be the Fed meeting. So much has already been written on this topic that further repetition would be superfluous. The prevailing opinion among investors at present is that the Fed meeting in September will be a kind of “early Christmas,” as investors have already unwrapped their “presents” this week. However, Fed Chairman Jerome Powell will have to offer the markets more than just interest rate cuts to maintain their unbroken optimism.

However, it is not only the US Federal Reserve that will decide on its monetary policy. At the same time, we will find out how interest rates for the Canadian dollar will develop. The Canadian economy is slowing down and inflation has fallen below the 2% target, making an interest rate cut seem likely. The only obstacle could be resistance from Donald Trump, who sees a cut in interest rates for the Canadian dollar as undermining his efforts to weaken the US dollar.

The situation at the Bank of England is much more complicated. The British economy is experiencing weak growth, while inflation stands at 3.8 percent. If the Bank of England cuts interest rates, this could lead to further price increases. Given the tense situation in the UK, higher prices would only increase dissatisfaction with the government there. This week offers a unique opportunity to realize the crucial role that monetary policy plays and how strongly it influences our lives.