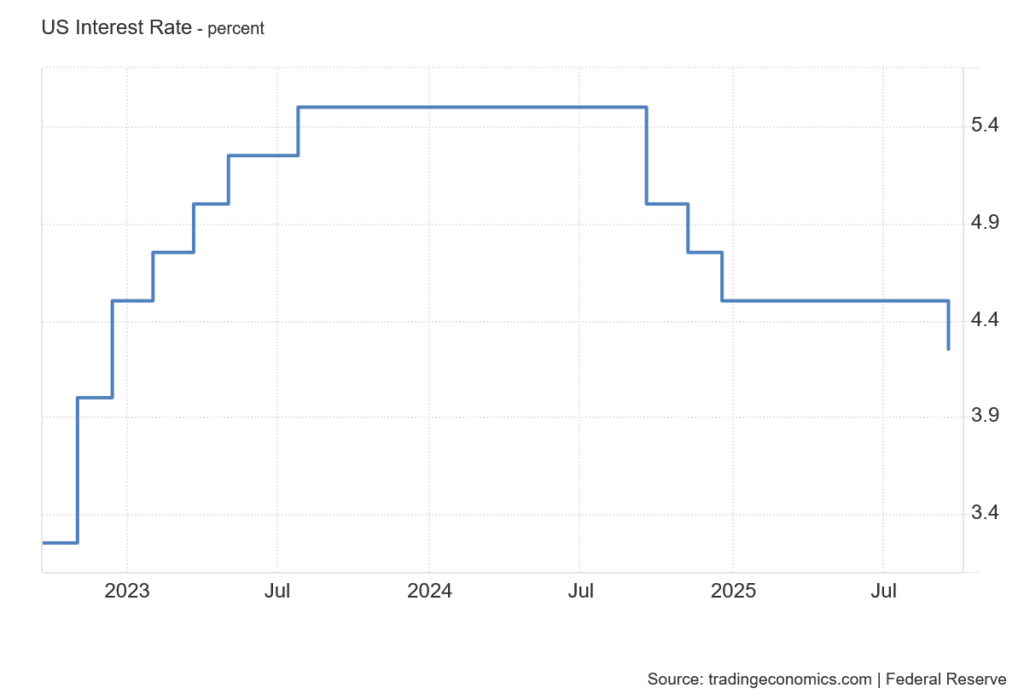

The investment sector initially breathed a sigh of relief, as the disaster scenarios that assumed interest rates would remain unchanged or fall by 50 basis points did not materialize. It is always good for the markets when expectations are met. And a reduction of exactly 25 basis points was expected.

So in the evening, they were able to continue in good spirits. But it very quickly became apparent that not everything is as rosy as one might expect. US monetary policy is thus characterized by several contradictions that will not be easy to resolve. What do these tensions look like within this institution?

Trump's man on stage

Eleven central bankers voted in favor of lowering interest rates by 25 basis points. One vote was against. And that vote belonged to Stefan Miran. The American economist came to the Fed straight from the White House. It is clear to everyone whose interests he will represent.

On Monday evening, the US Senate approved his nomination at the last minute. It was by no means clear whether he would make it to the meeting in time. On Tuesday, he was already attending the Fed meeting. And on Wednesday, he voted against the general consensus of the central bankers.

Miran has thus clearly set the direction. He will fight for the lowest possible interest rates. Given that Powell's term ends in May, the markets will be watching Miran much more closely over time, as it will be clear that the new Fed leadership will be more aligned with the White House.

In the long term, this is not good for the Fed, as it should remain apolitical. From May 2026 onwards, this will be very difficult. It is understandable that Trump may find low interest rates beneficial for his policies, but low interest rates are by no means risk-free. If they are very low, they will fuel inflation, further weaken the already weak US dollar, and further fuel the bubble in the real estate market. Internal tensions within the US Federal Reserve will not bring calm to the markets in the long run.

Inflation is no longer the biggest problem

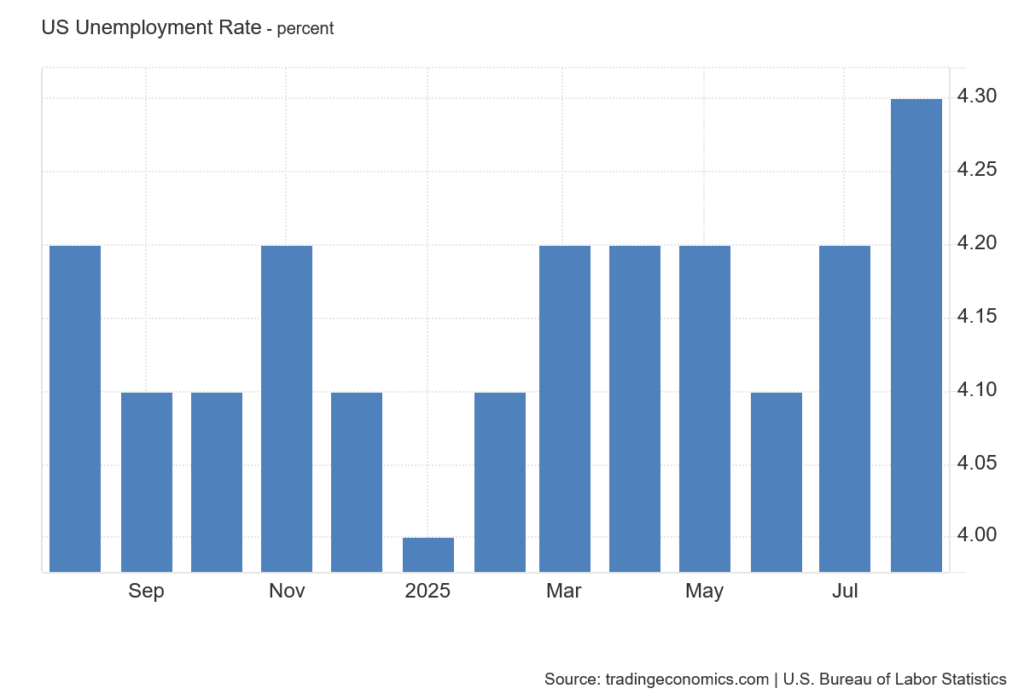

In addition to Stephan Mirano, the Fed's willingness to support the weakening labor market was a very important message. Jerome Powell made it clear in his speech after the interest rate cut announcement that the weakening US labor market was the main reason for this.

The Fed has a dual mandate: price stability and promoting maximum employment. The reduction in interest rates, both current and future, serves to support the American labor market. Jerome Powell is not only concerned about the slow rise in unemployment, but above all about the low level of new job creation.

With fewer jobs being created, it is logical to assume that unemployment will rise in the coming months. The Fed has revised its forecast for the unemployment rate to 4.5 percent by the end of 2025.

However, the interest rate cut, i.e., the support for the labor market, comes at a time when the Fed has also revised its inflation forecast for 2026 upward. PCE inflation is now expected to reach 2.6 percent next year, instead of the previously forecast 2.4 percent.

The Fed's decision thus sends a clear signal that the labor market is currently of crucial importance. The Fed is prepared to tolerate slightly higher inflation than it had previously indicated. This stance was also reflected in the forecast of further interest rate cuts. By the end of this year, the Fed could cut interest rates twice instead of just once. All this, of course, is contingent on macroeconomic indicators continuing to point to a cooling labor market.

The Fed has also raised its forecast for US GDP growth. In 2025, it is expected to grow by 1.6 percent instead of 1.4 percent. The Fed was even more optimistic for 2026, with growth expected to reach 1.8 percent instead of 1.6 percent. Growth of 1.8 percent is good because it creates new jobs. The good news is that the US is not expected to experience a recession if the forecast proves accurate.

Paradoxically, however, there is no reason to lower interest rates if GDP is growing solidly. From this perspective, it is obvious that Powell is bowing to political pressure. The overall impression of the press conference was that the current head of the US Federal Reserve is already looking forward to being relieved of the burden of leading the Fed in May.

The initial reaction of the markets was positive. However, this was followed by slight volatility. The markets fluctuated slightly as it was unclear whether the Fed had decided to cut interest rates for positive or negative reasons. Ultimately, the US markets closed slightly higher.

Furthermore, they remained optimistic despite the forecast that there will only be one interest rate cut in 2026. That is really not much to satisfy them completely. The markets did not pay too much attention to this information, as a slightly different Fed will be deciding on interest rates from May 2026 onwards.

Much ado about the Magnificent Seven

Fortunately, the Fed is not the only one deciding the fate of the markets. The US stock markets are largely determined by the performance of the seven largest technology companies. These were successful this week. Alphabet managed to pass a milestone in market capitalization when it joined three other companies whose value exceeds three trillion US dollars.

Tesla shares have jumped significantly. Over the past five days, they have risen by more than 21 percent, even though the car manufacturer is currently selling 13 percent fewer electric cars than a year ago.

The main reason for the increase is the fact that Elon Musk has purchased more than $1 billion worth of Tesla shares after a long period of time. As a result of this price increase, the classic P/E ratio reached a value of 246. Tesla shares are thus once again significantly overvalued. From a fundamental perspective, Tesla is much more expensive than Nvidia, whose sales and profits are rising rapidly.

Nvidia shares came under slight pressure this week. This was due to two negative reports about developments on the Chinese market. The Chinese antitrust authority (SAMR) accused Nvidia of violating the terms of its 2020 acquisition of Israeli company Mellanox Technologies for $7 billion. This acquisition strengthened the American chip manufacturer's dominance in the field of network technologies for data centers.

One of the conditions was that Nvidia ensure the availability of the chips on the Chinese market. The company faces a fine from the Chinese authorities for violating these conditions. At the same time, the Cyberspace Administration of China (CAC) called on companies such as ByteDance and Alibaba to suspend testing and cancel orders for the RTX Pro 6000D chip developed by Nvidia for China.

This pressure is no coincidence, as another round of negotiations between China and the US on the future form of new trade agreements took place in Madrid earlier this week. China is making it clear that it has the means to increase pressure on the US, specifically through Nvidia.

There is intense speculation in the markets that Chinese manufacturers are on the verge of producing their own chips for artificial intelligence. If these speculations are confirmed, the United States would lose its decisive advantage in the technology race.