Investors have finally forgotten about Liberation Day on April 2, when the stock markets crashed for several days. These events are now just an unpleasant memory. The big players are no longer afraid.

This trend is also confirmed by a recent Bank of America survey of large fund managers, which found that the preference for cash holdings has declined significantly since July this year. High cash holdings are a sign of caution. Their decline indicates that investors prefer to buy various financial assets and are not afraid to hold them.

Despite the current risks in the market, such as rising debt in industrialized countries, the major players remain optimistic and continue to buy.

Interest rate cuts do not solve all problems

Despite the subdued reaction immediately after the US Federal Reserve (Fed) meeting, positive sentiment ultimately prevailed. The interest rate cut and the prospect of two further cuts are generally perceived as positive news. However, as usual, this optimism is exaggerated.

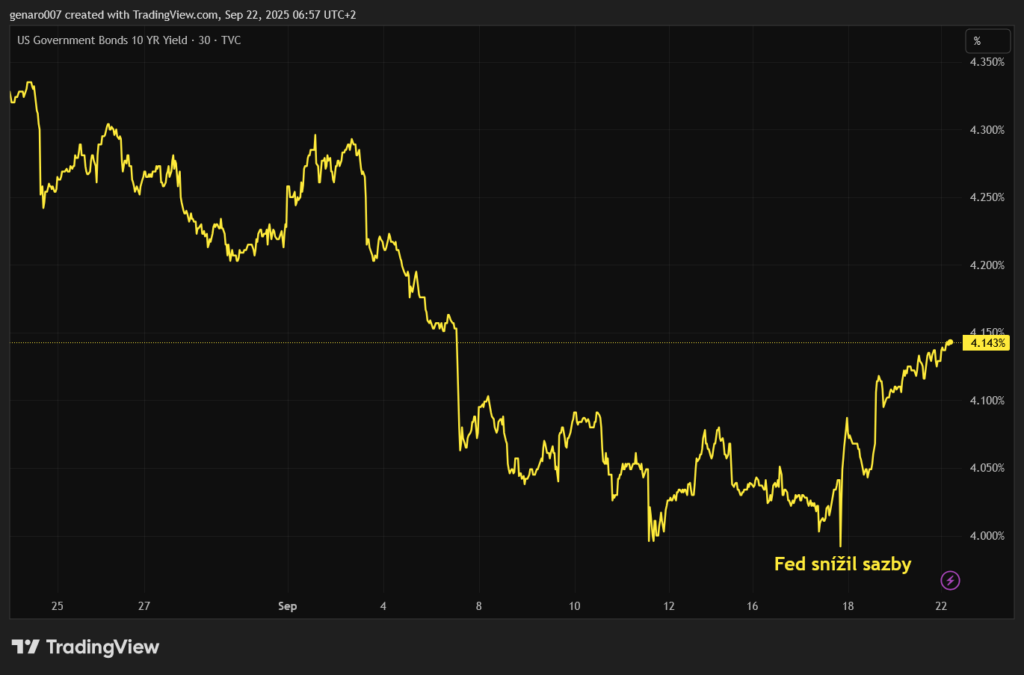

A 25 basis point interest rate cut does not solve the problem of rising unemployment. Nor does it help to bring inflation back down to the target of two percent. And it certainly does not solve the crisis in the US government bond market.

The bond market in particular has clearly shown that an interest rate cut is not a panacea. After the interest rate cut was announced, yields on ten-year government bonds fell below the psychological threshold of 4 percent, which was good news for the US Treasury Secretary and taxpayers.

This enabled the indebted US government to borrow more cheaply. Shortly afterwards, however, creditors realized that the Fed had raised its inflation expectations in its forecast. Logically, they demanded higher interest rates, and yields rose again above 4.1 percent.

An interest rate cut is indeed not a panacea. If they fall by 25 basis points, this merely provides access to slightly cheaper loans than American companies were used to. This effect is also particularly noticeable in the case of short-term loans.

To put the impact of interest rate cuts into perspective, we can cite an example from Europe. The European Central Bank (ECB) cut interest rates much faster than the Fed, yet there has been no significant economic recovery in Europe. The interest rate cut therefore primarily benefits stock market speculators, as it gives them an argument for why the markets could continue to grow.

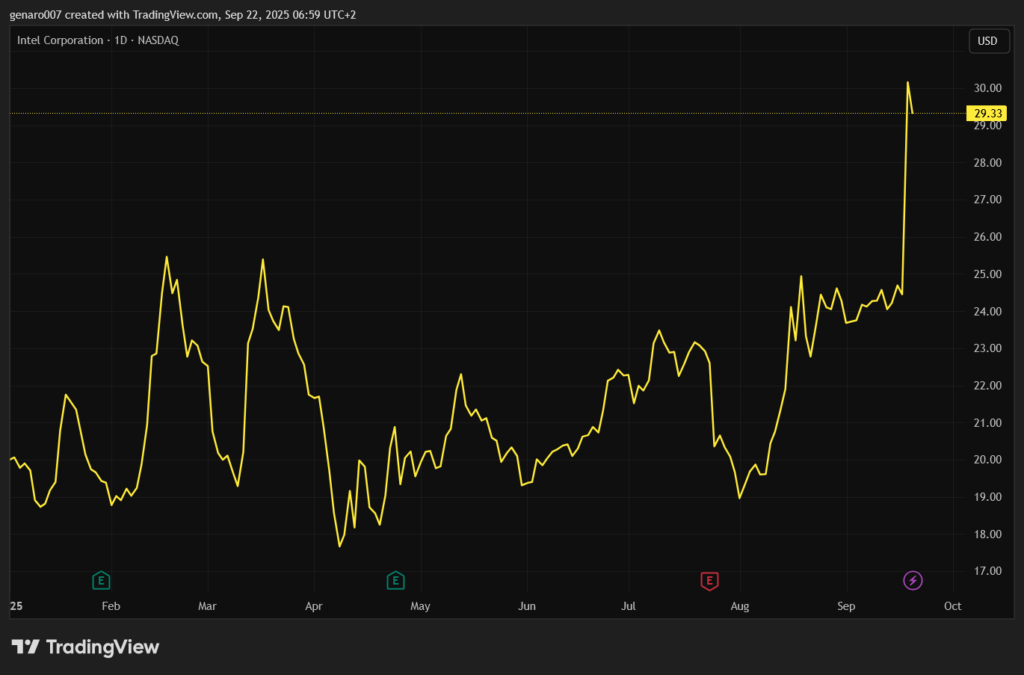

Intel shares back in focus

Last week will be fondly remembered by Intel shareholders. It has not even been a month since the US government made a surprise entry into this company. The Trump administration used funds from the Chips Act to purchase 433.3 million Intel shares. Given that these shares rose by more than 21 percent last week, the taxpayer's money quickly paid for itself.

The US government has no intention of selling these shares quickly, of course. On the contrary, Intel has become a strategic company of national interest. Most likely, the Trump administration knew what it was doing.

Nvidia has also invested $5 billion in Intel. Its CEO, Jensen Huang, spoke of a historic partnership between these two technology giants. The situation is somewhat paradoxical, as Nvidia has achieved growth thanks to its timely recognition of the artificial intelligence trend, while artificial intelligence has become an obstacle for Intel, showing that the company had “missed the boat.”

Nevertheless, this investment is a major success for Intel CEO Lip-Bu Tan, who has managed to get the company back on its feet. He was successful in negotiations with the Trump administration, which initially put pressure on him, as well as with Jensen Huang. His appointment as head of Intel thus proved to be an excellent choice.

This collaboration will enable the development of new generations of chips for data centers and PCs, bringing significant technological advantages. Overall, it strengthens Nvidia's position by diversifying the supply chain and accelerating innovation in artificial intelligence, while giving Intel access to cutting-edge GPU technology.

The investment will also help Intel raise the necessary funds to invest in catching up technologically. If Intel manages to recover and regain a leading position in chip manufacturing, it would be a major success for Donald Trump. If the company also returns to the top in the data center sector, the rise in its share price could be far from over.

Are we finally in for a quiet week?

A challenging week, in which major central banks such as the US Federal Reserve, the Bank of Canada, and the Bank of England met, is behind us. Investors now have time to analyze the measures taken by the individual central banks.

The situation is becoming complicated as there is virtually no uniform monetary policy and each central bank is pursuing its own strategy. The Bank of Canada is very cautious and is not hesitating to cut interest rates further to support the weakening Canadian economy.

The US Federal Reserve has lowered interest rates, but remains very cautious about future developments. The Bank of England is in the most difficult position, as it cannot afford to cut interest rates due to high inflation, even though the British economy is stagnating. For investors, including small savers, this raises the question of currency risk.

The trend is clear: all countries want to weaken their currencies in order to strengthen their economies in competition. Anyone who is building up savings must therefore consider in which currency to hold them.

The most favorable currency is, of course, the one that loses the least value. Let's hope that the coming week will be calm so that investors have time to consider this complex issue. According to the economic calendar, which does not contain any significant events, there should be time for this. Now it depends on whether Donald Trump will once again cause economic or geopolitical turmoil.