As the markets entered the new week, they performed a typical reaction, when the problems of the previous one were completely forgotten.

It is as if the investor Michael Burry, who has come out strongly against the phenomenon of artificial intelligence, had never even existed. For his part, he added one very important argument, in addition to the classic statement that technology stocks are insanely expensive. In fact, technology companies write off their investment in new processors over six years.

In fact, the lifetime of processors is around 18 months before they become obsolete. This slow depreciation of investments creates the illusion that the invested capital is working longer and more efficiently than is actually the case. If companies were to write off their processor investments faster, their profits would stretch significantly and they would look much less robust.

Nvidia's management has dismissed the criticism, arguing that they are no Enron, a famous symbol of accounting machinations and masking reality, and thus have no need to shroud their results in a fog of creative accounting.

It is true that Nvidia does not make accounting errors or mask actual status. Burry's objection didn't really go in that direction. The investor pointed out that the pace of innovation in AI is so great that companies are not keeping up.

The return on invested capital is so small not because companies have not found a use for artificial intelligence, but because they are constantly buying newer equipment. Nvidia, of course, has a vested interest in selling as many new chips as possible. At the same time, it doesn't have to deal with what clients actually need the latest chips for. That's not its concern. What is important is to artificially maintain demand.

So Burry has really kicked the hornet's nest, because the pace of chip innovation today is so frantic that companies often invest before they can use what they already have. This problem affects all major AI investors today. But the markets have ignored this problem.

Google versus SoftBank

Artificial intelligence is not just about Nvidia's chips, but the race is primarily at the level of language models. The current situation around AI is thus leading investors to be more cautious. It's a natural evolution. It will now become more of a question of how the race itself evolves. Companies that have invested huge amounts of money in development without having any real use for AI will drop out. On the contrary, those entities that outperform others with their tools will go ahead.

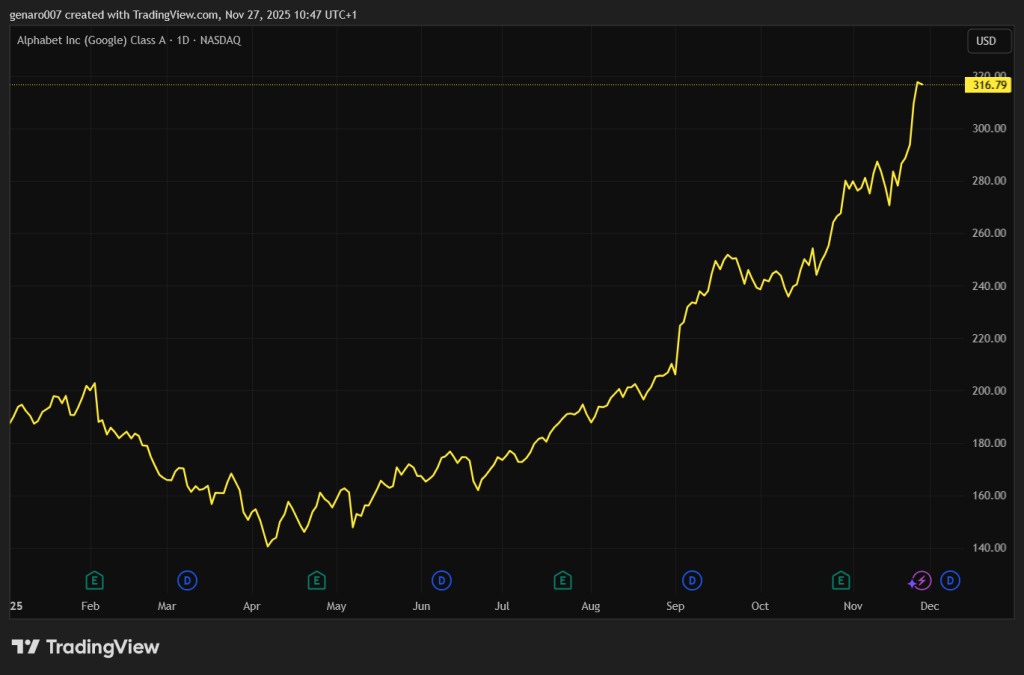

So far, the big winner of this duel is Alphabet. The latter recently introduced the third version of its Gemini 3 language model. According to many metrics, so far it turns out that this model is in many ways the best on the market.

And given that Alphabet can deploy this model instantly to billions of users through its products such as Android and Chrome, it has a distribution in its hands that competitors can only dream of. In other words, if anyone can turn raw technological superiority into real impact and monetization, it's Alphabet. The American firm is very well positioned to take the lead in the AI peloton.

This opportunity was sensed by legendary investor Warren Buffett, who, despite his traditional aversion to tech stocks, bought 17.8 million shares of Alphabet in the last published report. The success is borne out by the share price, which has risen 85 per cent in the past six months. The company now holds the third position in the stock market capitalization rankings. Google is poised to move into second position ahead of Apple.

The advent of Gemini 3 has caused some nervousness at OpenAI. Although version 5.1 brought technical improvements, it has not yet made as strong an impression as previous updates. OpenAI has also entered the browser segment with its Atlas product, where its solution is still finding its place. Combined with Google's aggressive entry, it thus appears for the first time that OpenAI's technological lead may be thinning.

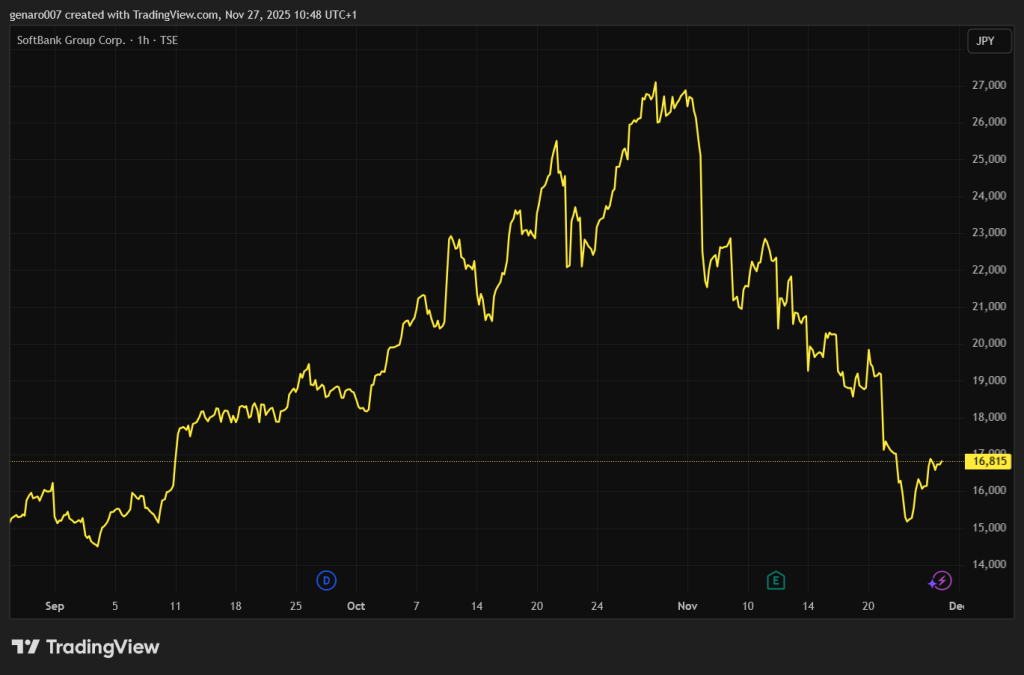

OpenAI is not yet listed on a stock exchange, and so we do not see exactly how its investments, cost growth, and actual model demand are impacting the financial health of the firm. What we can observe, however, is the collapse of Japan's SoftBank, which has provided OpenAI with substantial funding.

SoftBank's shares have been in freefall for the past month, having already written down over 33 per cent. However, the Japanese bank has more problems, but perhaps losing its lead is not helping OpenAI's stock. Thus, uncertainty in the sector may persist.

Japan as a new source of crisis

In addition to the events surrounding AI investments, we can find three macroeconomic risks in the market, but they have a common denominator, and that is debt.

The first potential crisis is US debt. It is worth noting that Donald Trump is doing everything possible to solve this problem. Whether this will not be beyond him remains to be seen, but no one can deny his desire to solve this problem, even at the cost of risky methods.

The second is the European debt, especially the French debt. Here, on the contrary, there is no sign of any effort to find a solution and it is simply waiting for the whole situation to become unbearable.

The last risk is Japan. However, with the new Prime Minister, Sanae Takaichi, it has taken a radical stance. Instead of trying to pull the handbrake and tackle Japan's debt, the Japanese Government is going to splurge even more. The new stimulus is set to reach 17.7 trillion yen, 27 percent more than under her predecessor. Japan's economy has thus been constantly living on infusions, but over the past thirty years of all this stimulus, the patient's health has not returned. And it will be no different after this stimulus.

The problem is that the country is plagued by inflation and the Bank of Japan will have to raise its rates. Until now, its governor, Kazuo Ueda, has been one of those who, while talking about the need to raise rates prospectively, has kept concrete data in sight. Now even this latest dove has swung and set markets up for the possibility that the Bank of Japan could raise its rates as early as December or January.

If this were to happen, we could see a repeat of last August's crisis. Investors would hastily dispose of their investments in foreign currencies in order to pay off their debts in Japanese yen.

In the medium term, this will be a big problem for the Japanese Government because, given the huge size of Japanese debt, even a small rise in yields means a large increase in repayments. Investors should therefore not forget to keep an eye on ten-year government bond yields in the coming months. The higher yields climb, the more heat there will be in the markets.