New York. Even before the decision was taken, the Federal Reserve Bank of New York published a study estimating that nearly 90 per cent of the costs arising from the new tariffs imposed by Donald Trump in 2025 would be borne by American consumers and businesses in the form of higher prices and lower profit margins.

In other words, ordinary Americans and domestic firms have paid the price for the introduction of the duties. The conclusion is significant, as it helped to anticipate how the US Supreme Court would ultimately rule.

In addition, tariffs have contributed to inflation in the United States remaining well above 2 per cent. That, in turn, complicates the path of the Federal Reserve towards lowering interest rates.

From one perspective, the president’s stance appears almost comical. On the one hand, he has introduced measures that keep inflation above the target; on the other, he has loudly demanded lower rates, as if one could pour petrol on a fire and then express surprise that the flames refuse to die down.

The worst academic work?

The White House, unsurprisingly, rejected the study’s conclusions. Kevin Hassett, chairman of the National Economic Council, argued that the research methodology was flawed and, following Donald Trump’s example, added a measure of invective. He described the paper as ‘the worst academic work he had ever seen’ and said that such an analysis ‘would not pass even in the first semester of economics’.

Hassett also suggested that the authors should face disciplinary action. Stripped of the rhetorical flourishes, the dispute centred on one point: according to Hassett, the authors failed to take account of the potential benefits of imposing tariffs. The measures, he argued, are designed to revive domestic production in the United States – a process that would inevitably take time.

The administration’s defence is crucial to understanding why the decision of the US Supreme Court poses such a difficulty for the Trump administration and why the president moved swiftly to reimpose the duties. If the tariffs were scrapped, the constructive element of the programme would fall away.

The result would not merely be a technical adjustment of trade policy, but a de facto admission that the promised industrial revival – on which considerable political capital has been spent – is being postponed indefinitely.

Constitutional limits on presidential power

That prelude alone illustrates what a bombshell Friday’s repeal of the tariffs by the US Supreme Court represented. Six of the nine justices voted to strike them down. The ruling was not unanimous, as three conservative justices sided with the president. However, two justices appointed by Donald Trump also voted against him, underlining the limits of presidential influence.

The core of the reasoning rested on the fact that the International Emergency Economic Powers Act of 1977 – designed to address exceptional circumstances – cannot be used to introduce ordinary trade policy unilaterally. As the Federal Reserve study indicated, it was primarily Americans themselves who bore the cost of the tariffs. From a constitutional perspective, the measure amounted to a new form of taxation, and only Congress has the authority to approve taxes.

The court did not argue that the president of the United States is barred from imposing tariffs altogether, only that he may not do so under that particular statute. Donald Trump moved quickly to respond, signalling that he would raise tariffs to 15 per cent under different legislation.

It is reasonable to assume that the new decision will also face legal challenges. There is speculation that companies may ultimately seek reimbursement of the duties already paid. Taken together, the ruling and the president’s reaction have increased uncertainty in financial markets – and uncertainty is seldom welcomed by investors.

For now, markets appear unsure how to interpret the situation. Immediately after the verdict, indices even rose. Some investors regard that as a hopeful sign that the global economy might return to the period before the tariffs were introduced. That scenario, however, seems unlikely, as the president’s broader economic strategy is built around protectionist measures. At the same time, the episode has demonstrated that the US president does not wield unlimited power and that American institutions continue to operate independently.

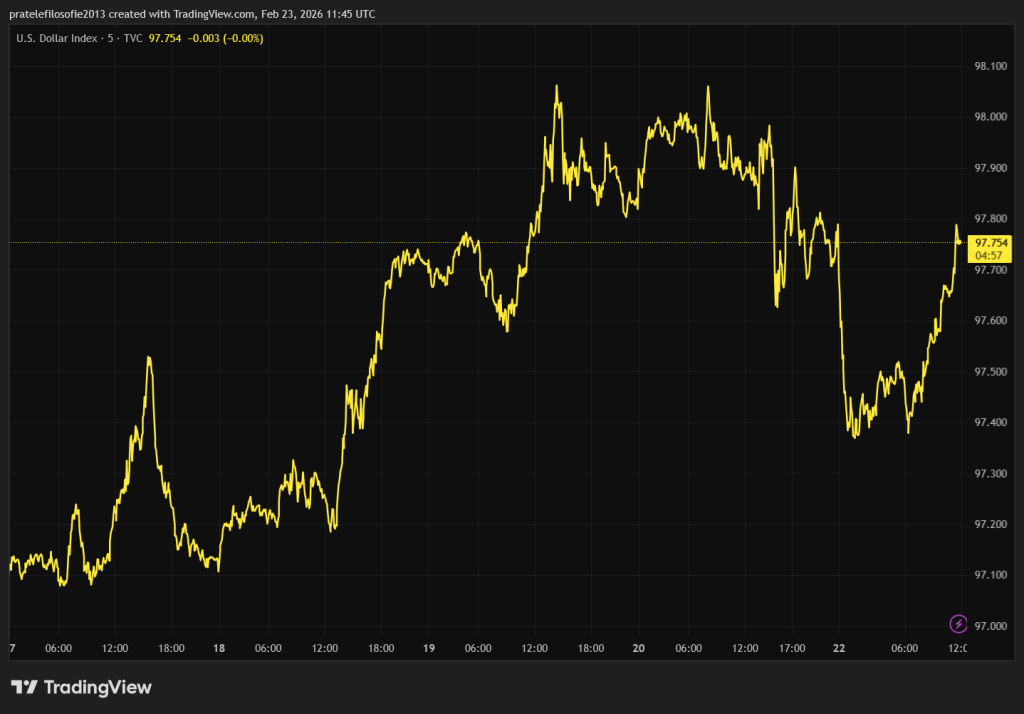

The most telling response came from the dollar. The dollar index edged lower. The tension between the president and the institutions is likely to contribute to a gradual erosion of confidence in the US currency.

Paradoxically, a weaker dollar may suit the White House. For the time being, indicators point to a longer-term bearish trend in the US currency – and there is little to suggest that the trajectory will reverse in the near future.

Another crack in the growth story

Tariffs were not the only development to dominate the headlines. Investors should also take note of another significant event. The New York–based investment group Blue Owl Capital has permanently suspended withdrawals from one of its private debt funds.

The firm provides financing to companies outside traditional capital markets and the banking sector. Instead of the quarterly redemptions that had been envisaged, investors will now receive their money back gradually as the fund disposes of its assets.

The wider private credit sector has been under strain for some time. The difficulty does not currently lie in corporate repayment capacity. The problem emerges when a fund seeks to sell parts of its portfolio: market liquidity is thin. Liquidity, which is taken for granted in favourable conditions, can quickly become a scarce commodity when sentiment deteriorates.

Private debt was marketed to investors as a profitable and comparatively stable alternative to traditional bonds, with the illiquidity premium presented as a reward for patience. The suspension of withdrawals is therefore more than a mere accounting detail; it is a warning signal.

If a fund cannot meet redemptions other than through the gradual disposal of assets, it suggests that the secondary market is not functioning as smoothly as investors had assumed. Another crack in the growth narrative thus lies not in a dramatic surge in defaults, but in the subdued admission that exiting an investment may prove far more difficult than marketing presentations implied.

At the same time, the open acknowledgement of the problem serves as a cautionary signal. Investors have begun to reassess the risks in the sector, which at least marginally reduces the likelihood of an abrupt crisis. A genuine crisis tends to erupt where complacency prevails – and the private credit market no longer fits that description.

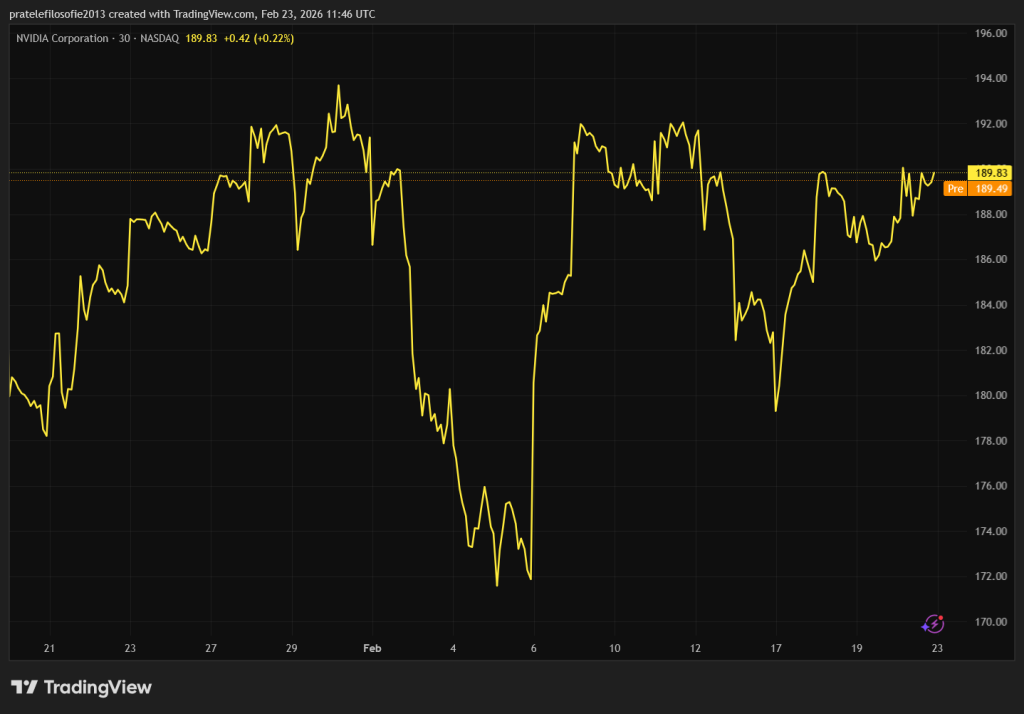

Will Nvidia decide everything?

The most important event of the coming week will take place late on Wednesday, when Nvidia publishes its financial results. The moment is a delicate one. The current earnings season has shown that investors are becoming increasingly demanding.

Strong figures are now merely a necessary condition to prevent the share price from slipping. For the stock to advance meaningfully, the company must above all deliver an upbeat outlook for the remaining quarters of the year. In Nvidia’s case, few doubt that the first and second quarters of 2026 will also prove robust.

Major technology groups have already signalled that they intend to maintain heavy capital expenditure and continue building data centres, which should support demand. The uncertainty lies further ahead. Questions may arise over guidance for the final months of the year, or over potential constraints linked to shortages of memory chips.

The real risk for Nvidia is that it could become a victim of its own success. If demand for the new Rubin chip proves overwhelming, the current Blackwell series may rapidly lose relevance. In the technology sector, there are few greater pitfalls than being displaced by one’s own innovation.

Companies could then be compelled to write down earlier investments. It is precisely this investment cycle that investors such as Michael Burry have criticised.

Firms are committing vast sums to data centres, with returns calculated over many years. If the technological frontier shifts too quickly, some of those investments may lose their economic rationale before they have even amortised.

Paradoxically, innovation that moves at excessive speed can unsettle the very investment cycle that propelled Nvidia to the summit of the market. The central question is therefore not only whether Rubin will be more powerful, but whether the pace of technological progress could outstrip the market’s capacity to absorb the shift on commercial terms. The coming week may offer the first indications of an answer.