Wars and armed conflicts are always moments of radical change for financial markets. In the case of Iran, the shift could prove particularly severe.

Its scale will be determined by two factors: the duration of the conflict and the number of countries that ultimately become involved. Both remain entirely unknown, so speculation serves little purpose. It is more useful to outline the basic scenario that unfolded when markets opened on Monday.

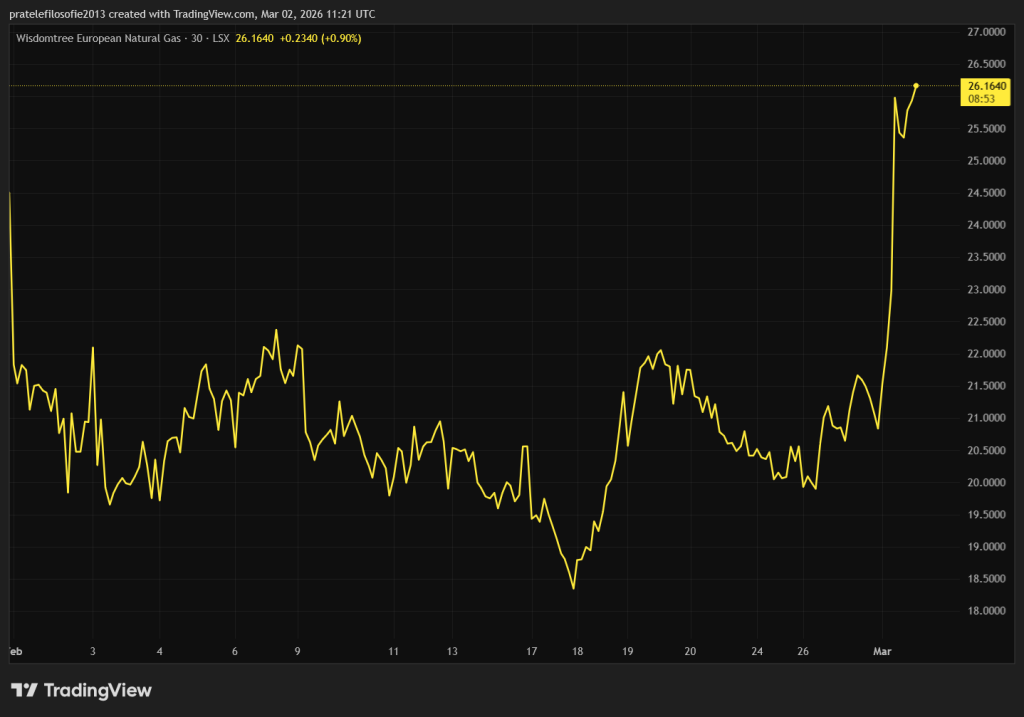

As expected, oil prices climbed. The rise in the price of liquefied gas in Amsterdam represents a significant blow to Europe. While crude gained roughly seven to eight per cent, gas on the TTF exchange surged by as much as 25 per cent. Gold prices are also likely to continue rising.

Yields on long-term US government bonds are expected to move higher. The dollar and the Swiss franc are forecast to strengthen against the euro and the Japanese yen. Equity markets are likely to weaken, with the notable exception of shares linked to the oil and defence industries.

Central bankers and macroeconomists will brace for higher inflation. The longer the conflict endures, the stronger that pressure is likely to become. Should credible signs of a swift end emerge, the opposite reaction can be expected.

Investors without extensive experience or a high tolerance for risk would be wise to wait a few days before adjusting their portfolios. It should be borne in mind that Iran has restricted internet access, limiting the flow of direct information.

At the same time, the internet is awash with videos either generated by artificial intelligence or recycled from unrelated conflicts. Such material inevitably affects not only the public but also investors. The challenge is to resist being swayed by it.

One way to do so is to focus on structural issues within the financial markets. Long-term challenges will not disappear. Once the war subsides, equity markets will return their attention to those underlying questions. The present period may therefore offer an opportunity to examine them more closely. One of the most significant remains artificial intelligence.

Nvidia at the centre of earnings season

Nvidia’s results effectively marked the culmination of the fourth-quarter 2025 earnings season in the United States. Although reporting will continue in the weeks ahead, few companies carry comparable weight within the main indices.

The chipmaker accounts for roughly 8 per cent of the S&P 500. Its movements – whether declines or further gains – can therefore influence the broader index. Its performance matters even to investors who do not hold the stock directly.

The figures were robust. In the fourth quarter, Nvidia reported year-on-year revenue growth of 94 per cent to $43bn. Revenue rose 73 per cent to $68.1bn, exceeding analysts’ expectations on both counts. The company has thus maintained formidable momentum.

For large technology groups, annual growth of around 20 per cent is often regarded as a lower benchmark. Nvidia therefore remains an above-average growth company, even if the era of triple-digit expansion has passed. In a more uncertain climate, however, investors have become increasingly sensitive to forward guidance.

For many companies, surpassing estimates on revenue and profit has no longer been sufficient. The outlook has become decisive. Nvidia did not disappoint here either. For the current quarter, it projected revenue of $78bn, above analysts’ forecasts of $72.9bn.

Strong results have come to be expected from Nvidia, even as artificial intelligence unsettles parts of the software sector and weighs on related share prices.

The company is likely to be less exposed to that turbulence than many software groups. Indeed, pressure within the sector may even reinforce demand for its products. The tightening competitive environment has been described as a rapidly constricting cycle by Citrini and Alpa Shah in their study The 2028 Global Intelligence Crisis, which unsettled markets last week.

Excellent results, but uncertainty ahead

According to the study, the difficulties facing software companies and their forced adaptation to artificial intelligence are creating a dynamic that ultimately benefits suppliers of computing power such as Nvidia.

Established firms must invest heavily in artificial intelligence. The technology enhances productivity, replaces costly labour and channels savings back into further development. That cycle ensures a steady flow of capital into the sector as companies compete to remain viable.

Failure to cut costs would leave traditional groups vulnerable to start-ups able to offer comparable products at lower prices thanks to artificial intelligence. That competitive pressure underpins continued investment and supports Nvidia’s position.

The company therefore faces little immediate risk of declining demand. Yet its shares still fell by more than 7 per cent.

The explanation lies less in current performance than in the longer-term outlook. Investors broadly expect strong results this year. The central question is how long the present pace of growth can be sustained.

Nvidia’s valuation remains elevated. Markets are reluctant to push it higher without greater clarity on the durability of its expansion. Growth will slow at some point, though no one can yet define the ceiling. Competition will also intensify. Advanced Micro Devices recently announced a major contract with Meta Platforms to supply data centres.

Constraints on the construction of data centres may also weigh on performance. In the US, projects face shortages of skilled labour and limits in electricity generation capacity.

There is also the issue of circular investment, highlighted by investors such as Michael Burry. Nvidia invests in numerous artificial intelligence start-ups, some of which then purchase its chips. A portion of that capital therefore flows back to the company.

Chief executive Jensen Huang’s press conference did little to dispel such concerns. The market’s focus is not on Nvidia’s current strength, but on whether its dominant position can endure once investment enthusiasm gives way to more sober valuation standards. If the conflict in Iran drags on, that shift in market sentiment and valuations could come sooner than many expect.