Investors have had a turbulent weekend. Although the International Energy Agency approved plans on Wednesday to release 400 million barrels of oil from strategic reserves, the move did little to calm markets. Prices showed little reaction, for several reasons.

Firstly, the decision itself underscores the severity of the situation. Rather than reassuring investors, it raises further concern. If Donald Trump’s assertion that the conflict is effectively over were accurate, such drastic measures would not be necessary. Moreover, the released oil is not expected to reach the market until late March at the earliest, by which time many had hoped the war would already have ended.

Secondly, even though some crude that would normally pass through the Strait of Hormuz can be rerouted via pipelines through Saudi Arabia, the supply deficit is estimated at around 15 million barrels per day.

Since March 7, traffic through the strait has been minimal. The resulting shortfall has therefore already reached at least 135 million barrels. Set against the planned release of 400 million barrels, this suggests that, while substantial, the reserves would cover the deficit for only a limited period, roughly 18 days.

These figures remain estimates. Higher prices are also likely to reduce global demand over time. Even so, in the most optimistic scenario, the released reserves would cover the shortfall for about a month. Investors are therefore asking what happens next if the disruption continues.

However, investors’ weekend respite was disrupted not only by these calculations but also by reports that the United States had launched an attack on Kharg Island. The island lies at the heart of Iran’s oil industry and is believed to handle around 90 per cent of the country’s oil processing.

The Trump administration sought to reassure markets, saying the strike targeted only military sites and was intended to avoid oil infrastructure. Tehran responded by warning that any attack on its energy facilities would trigger retaliatory strikes against a wide range of targets.

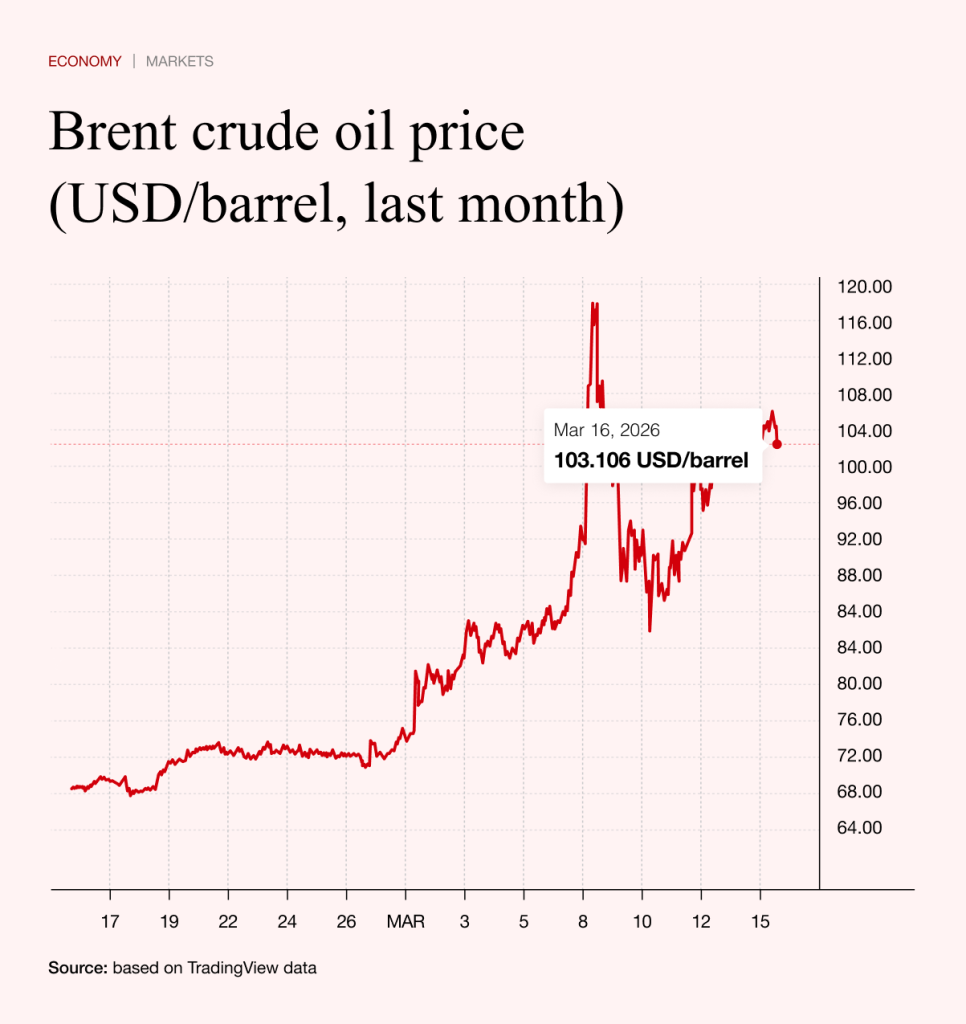

As oil is not traded over the weekend, many expected a repeat of the previous week, when Asian markets drove prices sharply higher overnight from Sunday to Monday, briefly approaching $113 a barrel. This time prices rose by only around two per cent, a modest increase given the scale of events.

Taken together with Iran’s denial that it had requested talks with Washington, the market reaction appears relatively restrained. Even so, oil prices are now on an upward trajectory. Unless there is positive news pointing to a resolution of the conflict, further increases are likely.

For many analysts, current price levels remain manageable. A more serious problem would emerge if prices move into the $120 to $130 a barrel range, where the risk of a temporary shock developing into a systemic crisis would increase significantly. Such a scenario could trigger a deeper market correction.

Stock markets in the context of the conflict

After two weeks of conflict in the Persian Gulf, it is possible to take a broader view of market performance. Overall, stock indices in Europe and the United States have held up relatively well.

The Nasdaq technology index has fallen by more than six per cent since the fighting began. While notable, this remains a limited reaction given the frequency of warnings about escalation and the prospect of a wider conflict.

European markets have performed somewhat worse. Rising energy costs have weighed more heavily on them than on US markets, where technology companies, which are less exposed to energy shocks, play a larger role. For industrial economies such as Germany and Italy, higher energy costs could pose longer-term challenges. Even so, Germany’s DAX index has fallen by only 7.39 per cent.

Does this relative stability suggest that markets remain calm, or are investors underestimating the risks?

The answer is clearly no. A closer look at the composition of major indices reveals a distinct divide between winners and losers at company level.

It is no surprise that oil companies are among the main beneficiaries of the current situation, particularly those focused on extraction rather than refining and downstream sales. For the largest integrated oil groups, which operate across the entire value chain, gains have been more moderate.

Among the losers, airlines stand out. Many have been forced to cancel flights due to airport closures in Dubai and Tel Aviv. Even those that do not operate routes to these destinations are facing higher jet fuel costs, which are weighing on profitability across the sector.

Unexpected winners and losers

Less obvious casualties can also be identified. The luxury goods group LVMH, for example, has already faced pressure due to weakening demand from Chinese consumers. It is now also contending with declining sales in the Middle East as a result of regional instability.

Although customers in the region account for a smaller share of revenue than those in China, they are still estimated to contribute between €4 billion and €6.5 billion annually. From a fundamental perspective, LVMH shares are now trading at a price-to-earnings ratio of 22.6, a level that may appear attractive to long-term investors.

Finally, let’s mention one unexpected winner. Hand in hand with oil and natural gas, fertiliser prices are also rising. Their production requires urea, which is a byproduct of the oil industry. The only country in Europe (excluding Russia) that has its own oil and natural gas reserves and can thus produce fertilisers on a massive scale is Norway. The Nordic country is therefore profiting heavily from the current situation, a fact reflected in the strengthening of the Norwegian krone. But that’s not all. Yara, one of the world’s largest producers of mineral fertilisers, is traded on the Oslo Stock Exchange. Its shares have risen by 20 per cent since the start of the conflict.

Central banks in the spotlight

What should investors watch in the coming week? Alongside developments in the conflict with Iran and movements in commodity prices, attention will turn to monetary policy. A series of key central bank meetings are due, from the Bank of Japan to the European Central Bank and the Bank of England.

The main event will come on Wednesday, when the US Federal Reserve announces its decision on interest rates. Despite the sharp rise in fuel prices, Donald Trump has recently called on Chairman Jerome Powell to cut rates. Such a move would risk fuelling inflation further, a prospect that sits uneasily with current market conditions.

Most central banks are therefore expected to keep rates unchanged and adopt a wait-and-see approach. Any decision to raise rates in the current environment would send a strong signal that policymakers see more serious inflationary pressures ahead.

The question is whether any central bank will act pre-emptively, or whether markets will be left to respond only once inflationary pressures intensify.