For the first time in a long time, the market review opens with something other than oil prices, although they will also feature today. Most of the world’s major central banks are meeting this week, and their importance is self-evident. The vast majority are tasked with maintaining price stability, in other words, keeping inflation in check.

As oil and other commodity prices, including natural gas, helium, sulphur and fertilisers, rise sharply as a result of the blockade of the Strait of Hormuz, pressure on household finances can be expected in the coming weeks and months.

At the same time, general uncertainty about global developments is prompting people to spend less and build up savings for a rainy day.

The situation is serious for two reasons

The first is that time is running out. The war in Iran has been underway for 20 days, yet there is no clarity about when it might end. The outlook remains highly uncertain. On the one hand, Donald Trump is proclaiming total victory and the destruction of 100 per cent of Iranian targets. On the other hand, Iran continues its attacks and the strait remains blockaded.

If the original assumption that the war would last between four and six weeks still holds, we should already be halfway through. Commodity prices are elevated, and 20 days is sufficient for these developments to begin feeding into macroeconomic indicators.

Perhaps the only consolation is the time lag in the data. Even now, the US Federal Reserve had only February macroeconomic data available when making its decision. These already showed a modest rise in oil prices, reflecting the upward trend that began as US ships moved towards Iran. Since then, oil prices have risen by more than 50 per cent.

But why might this not prove disastrous? Inflation data for March will not be available until mid-April. If the war has ended by then, markets will look ahead and may treat the episode as a temporary shock. The reaction, therefore, may not be overly dramatic.

However, this is the optimistic scenario. A more troubling outcome would arise if the conflict continues even after the March figures are released.

The second piece of bad news is that this is inflation driven by a supply-side shock. In such cases, central banks have limited tools at their disposal and little ability to influence oil prices directly. They can reassure markets and the public, and attempt to mitigate secondary price effects, but the shock itself must run its course.

Central banks in action: Australia's pre-emptive strike

A series of central bank meetings opened with the Australian one. It was indeed a sharp start as Australian central bankers were undeterred by the rate hike. Rates on the Australian dollar rose 25 basis points to 4.1 per cent.

The reason for this decision was, understandably, concern about rising inflation as a result of the war in Iran. It should be added, however, that Australian inflation is already at 3.8 per cent, so it could very easily approach the five per cent mark.

That is already quite a high level, which would require more radical action. It is therefore a precautionary measure on the part of the Reserve Bank of Australia, but one that may inspire others. Its decision thus immediately sparked speculation about the Fed's next course of action.

The Fed is waiting in the shadow of policy

Under normal circumstances, this would have been Jerome Powell’s penultimate press conference as Fed chair. The word ‘normal’ must be used with caution. Powell is under investigation by the Justice Department and has made clear he will not step down until the matter is resolved transparently.

As a result, the Senate process has stalled and confirmation of a successor has been delayed. There is therefore a strong possibility that Powell will temporarily extend his term. In truth, there is little to lose, as the coming months are likely to be challenging due to political pressures and stagnant rates.

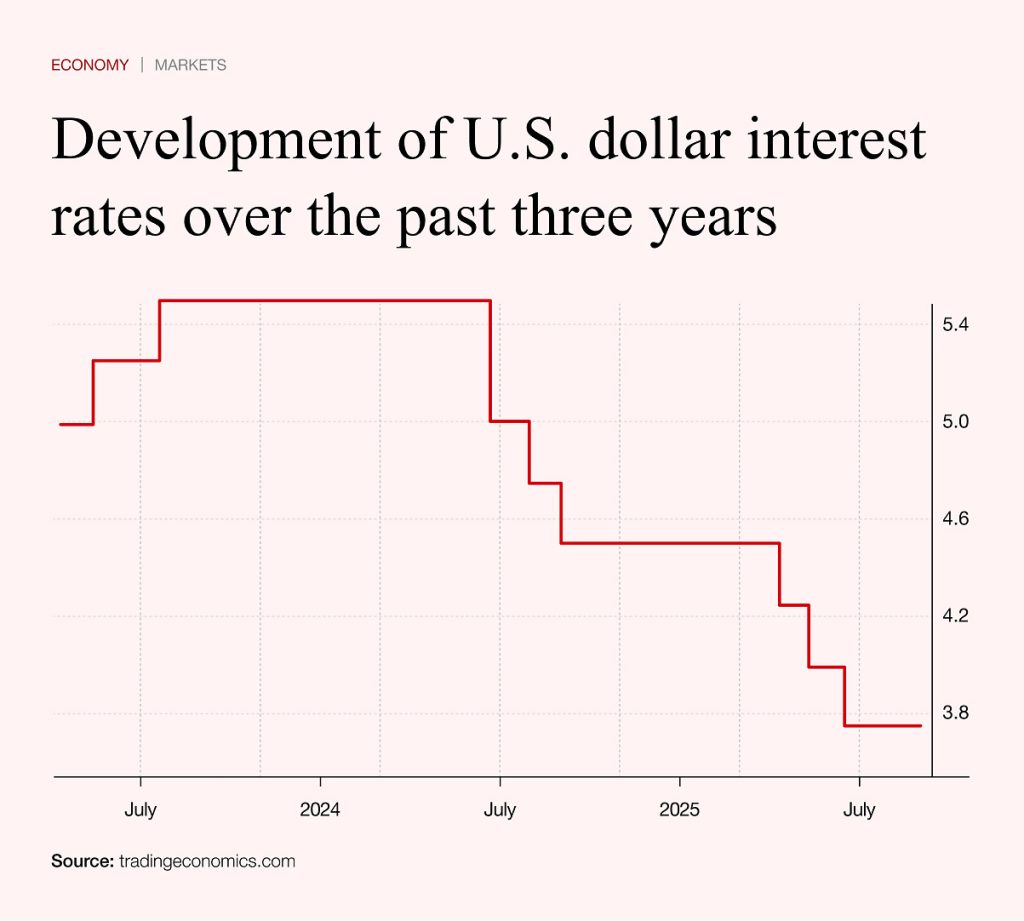

The Fed kept its key rate unchanged at 3.75 per cent, a move that came as no surprise. While a rate rise might have been justified, it would have added strain to markets already grappling with high oil prices and complicated Donald Trump’s position following the attack on Iran.

At the same time, a rate cut, which the US president had favoured ahead of the meeting, was not an option, as it would have fuelled inflation. One positive aspect did emerge. The governors’ vote was largely unified. Before the meeting, there had been speculation that the uncertainty surrounding Iran would deepen divisions. That did not materialise. Only Stephen Miran supported a rate cut, which surprised no one.

The meeting also presented updated economic projections. Inflation is expected to rise from 2.4 per cent to 2.7 per cent in 2026, before stabilising in line with earlier forecasts.

GDP growth projections were revised slightly higher, with models suggesting expansion of 2.4 per cent in 2026. Powell attributed this improvement to increased labour productivity driven by artificial intelligence, which is expected to have a positive impact on the US economy.

At the same time, the Fed does not expect artificial intelligence to have a significant effect on unemployment, which is forecast to decline gradually to 4.2 per cent in 2026.

Taken as a whole, the projections suggest relative stability, with no fundamental shift in outlook. However, at the subsequent press conference, Powell was asked how the forecasts accounted for rising oil and commodity prices.

He replied that if the Board had a ‘joker’ that would allow it to avoid publishing an economic forecast, it would have used it at this meeting.

In effect, Powell acknowledged on camera that policymakers do not yet know what lies ahead.

That may not sound reassuring. Yet it does reflect a degree of humility, which is preferable to offering false certainty about the effects of military intervention.

Further escalation of the war in Iran

Tensions in the Gulf have intensified rather than eased. The conflict has entered a new phase. Israel has struck the South Pars gas field. Iran responded by signalling it would target gas infrastructure in the region, and followed through on that threat.

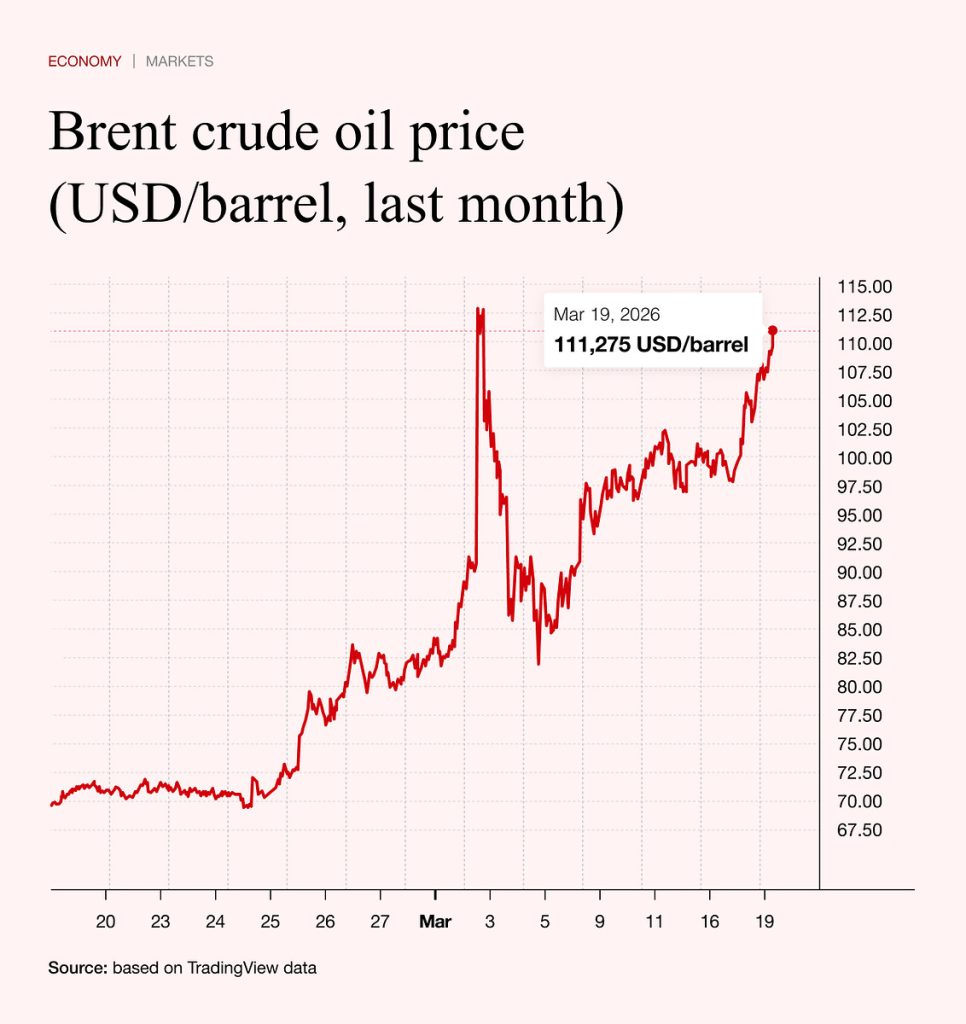

On Wednesday evening, it attacked Qatar’s Ras Laffan industrial complex. Donald Trump reacted negatively, as such developments inevitably push oil and gas prices higher. This has already been reflected in the markets. Brent crude briefly traded above USD 110 per barrel, a level associated with crisis conditions.

When prices crossed that threshold about a week ago, the US administration responded with measures and rhetoric aimed at bringing them down, and initially succeeded. A similar situation is now unfolding, and further action may be required to prevent serious damage to the global economy.

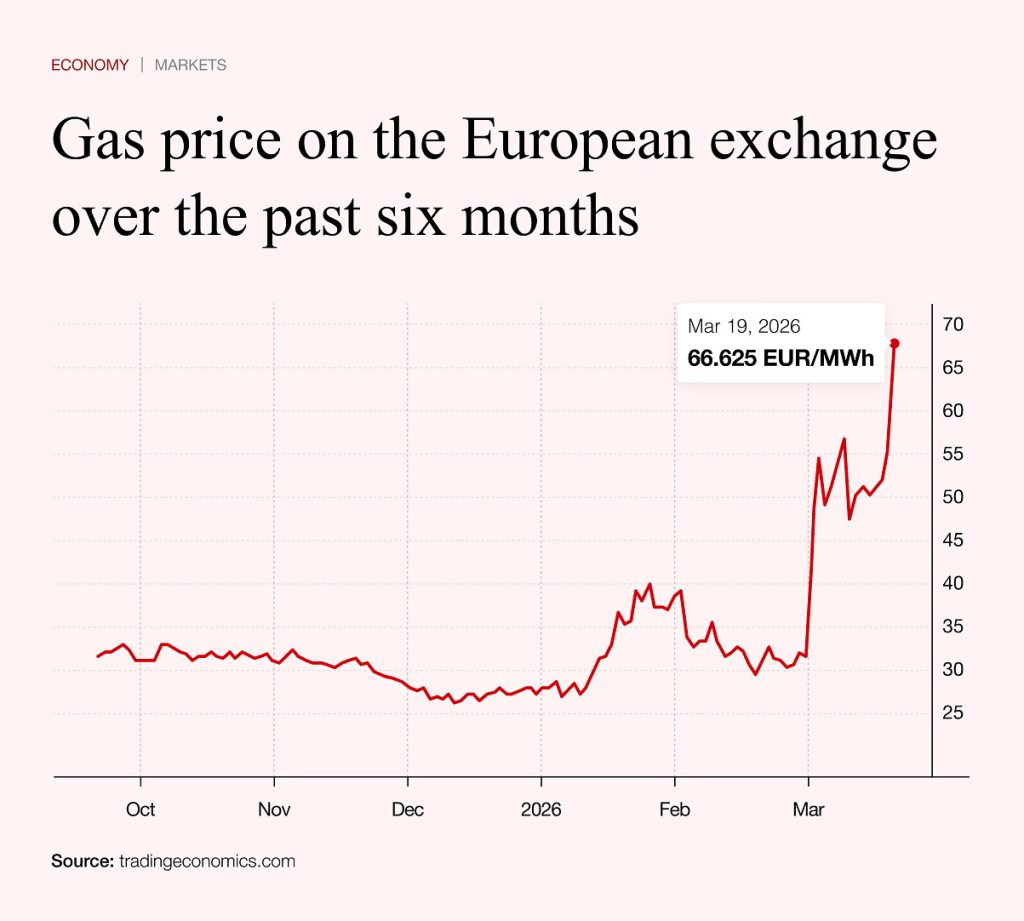

For Europe, however, the outlook is particularly concerning, as it points to potential disruption of gas supplies. Gas prices on the Amsterdam exchange have exceeded EUR 66, marking a daily increase of around 20 per cent and the highest level since the start of the conflict.

European leaders need to respond swiftly, as the risk of a repeat of the 2022 gas crisis is growing. High gas prices are also exerting severe pressure on electricity prices across the continent.

The European Central Bank is also meeting on Thursday. It remains to be seen whether it will follow the Fed’s cautious approach or opt for pre-emptive action in line with Australia.