The European gas market received another shock this week. Conditions have been fragile for some time, yet for the past three weeks a steady stream of negative news from the Middle East has kept markets on edge.

Midweek brought one of the most serious developments. An Iranian ballistic missile struck an industrial complex in Ras Laffan, Qatar, on Wednesday evening, causing ‘extensive damage’ to a facility used to liquefy natural gas.

The strike was Tehran’s retaliation for an Israeli attack on Iran’s South Pars gas field, which continued into Thursday morning. In the Qatari port city, home to the world’s largest liquefied natural gas (LNG) complex, the attack triggered ‘widespread fires and other major damage’, according to QatarEnergy. Early reports suggest repairs could take years.

Disruption takes shape

Qatar is currently the world’s second-largest LNG exporter after the United States. Roughly a fifth of globally traded LNG originates there, and almost all of it is processed in Ras Laffan.

To put that into perspective, around 580 billion cubic metres (bcm) of LNG were traded worldwide last year. Qatar accounted for about 110 bcm and had been rapidly expanding capacity, with plans to reach nearly 200 bcm in exports by 2030. Buyers had been counting on that growth.

The Israeli and US strikes on Iran, followed by Tehran’s retaliation, have severely disrupted global energy markets.

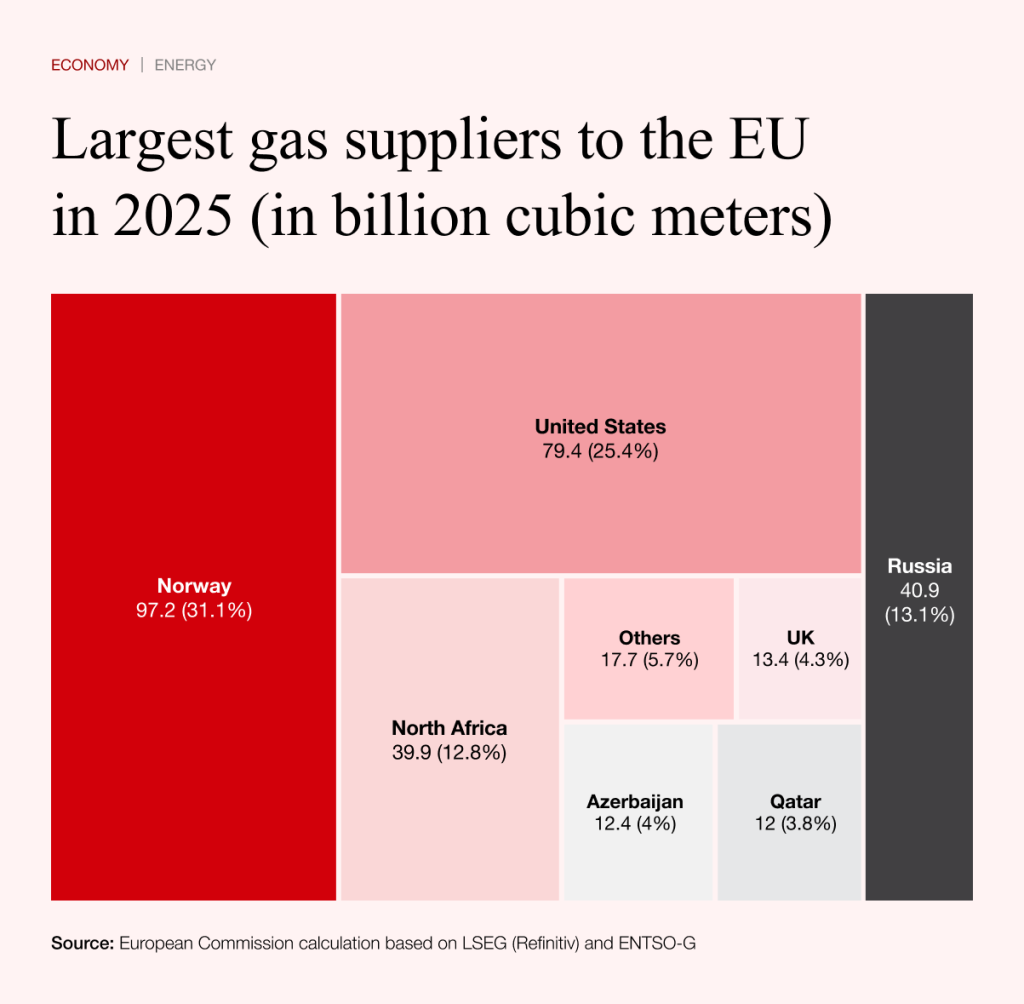

Qatar primarily supplies Asian markets, but the European Union has also relied on roughly 12 bcm annually. The bloc had placed considerable hopes in the Gulf state as it sought to replace pipeline deliveries from Russia with LNG imports.

The United States has taken a leading role in this shift and is now Europe’s largest gas supplier after Norway. Qatar, with its expanding export capacity, had been expected to play an increasingly important role.

Geopolitical tensions have complicated that strategy. Following disputes with US President Donald Trump over trade and Greenland, concerns about dependence on overseas suppliers have intensified. Qatari gas was seen as at least a partial hedge. At the same time, EU member states have agreed to phase out Russian gas imports entirely, banning LNG from January 2027 and pipeline supplies from November 2027.

Escalation hits gas markets

The war in the Middle East is now reshaping those assumptions.

The consequences are already clearly visible in prices, which have more than doubled since the end of February. On Thursday, gas traded at more than €70 per megawatt-hour at times on the Amsterdam exchange. European buyers are now competing for supplies with Asian countries, which are facing significant shortages as a result of the war and are willing to pay higher prices for the commodity.

Should the escalation continue, even physical supply constraints in Europe cannot be ruled out. Filling storage facilities ahead of next winter may prove significantly more difficult.

There is little indication that tensions in the region will ease soon.

While President Trump distanced himself from Israeli strikes on Iran’s South Pars gas field, he warned that if Tehran attacked Qatari energy infrastructure again, the United States would ‘blow the whole thing up’.

Iran’s Revolutionary Guards, meanwhile, described their response as the beginning of a ‘new phase of war’, pledging further retaliation against any attack on the country’s energy sector.

Time for a rethink

The past three weeks have underscored a simple reality. Europe can no longer afford to be selective in global energy markets.

Flexibility is becoming essential in an increasingly volatile world. Further geopolitical flashpoints cannot be ruled out, including in Asia, where China has yet to pursue its strategic ambitions by force on a comparable scale.

Against that backdrop, European policymakers are already exploring ways to ease regulatory constraints. A relaxation of green targets is being discussed behind closed doors. While such steps may help, they are unlikely to be sufficient.

Europe risks losing access to liquefied gas supplies to higher-paying Asian markets. A significant share of global supply may effectively disappear from the European market. Even if outright shortages are avoided, the impact on prices will be considerable.

Europe’s supply of liquefied gas will be diverted to Asia. Ten per cent of global supply has effectively dropped out of the market. If this does not result in physical shortages in Europe, it will certainly be reflected in higher prices.

With the impending ban on Russian supplies, the situation will only worsen. Lifting it could be a first step towards more pragmatic thinking in Europe. Economic pressure on Russia for invading Ukraine has its justification, but not if it causes far greater harm than it delivers in benefits.