We are entering the fourth week of the conflict with Iran, and the coming days could prove decisive for financial markets. For now, US markets – and Israeli equities in particular – are taking the situation in their stride, despite the scale of the crisis and the potentially vast financial burden for both countries.

The cost of the war will be reflected in wider budget deficits, adding to already elevated debt levels. For the moment, however, markets remain focused on an optimistic scenario, even as the first cracks begin to appear.

Interest rates and central banks hold back

Last Friday’s session already carried a markedly more cautious tone. Central banks – with the exception of Australia, which raised rates – left policy unchanged at their latest meetings.

At the same time, expectations of rate cuts this year have diminished significantly. The European Central Bank also held rates steady, yet markets have begun to price in the possibility of further tightening, with some projections pointing to as many as two increases.

That shift has weighed on equities. For now, central bankers acknowledge the uncertainty and are waiting for clarity on the duration of the conflict before adjusting their stance.

Trump’s statements offer little clarity, as the situation appears to shift from day to day. One moment, the end of the war seems near because there is little left to invade; the next, the US threatens further escalation after Iranian operations in the Gulf.

These swings in tone are difficult to interpret, leaving markets to focus on one key variable: time. Initially, the operation was expected to last up to four weeks, but this was later extended to four to six weeks. That information proved crucial for investors and helped prevent broader panic.

The time factor and geopolitical uncertainty

For now, financial markets continue to treat the conflict as a temporary shock. The global economy may have to absorb the impact, but the adjustment remains manageable. Once that timeframe is exceeded, however, the situation could enter a very different phase, with losses mounting and some proving irreversible.

Last week, a red line was crossed on both sides with the attack on Iran’s power plants and the subsequent Iranian missile strike on the Dimona nuclear research centre. Yet markets continue to hope for a reversal driven by Washington.

Trump has issued a fresh ultimatum demanding the reopening of the Strait of Hormuz, warning that otherwise he will launch even stronger military strikes. So far, the threat appears to have had little effect, neither on Iran nor on financial markets.

What has influenced expectations, however, are reports that the Trump administration is seeking negotiations and looking for a mediator. That may prove difficult. Oman, a previous intermediary, has declined the role, while Qatar has shown little enthusiasm, given the threat of Iranian missile attacks and the scale of potential financial losses.

Markets are therefore still betting on a scenario in which Trump ultimately presents a ‘super-deal’ guaranteeing peace in the Middle East for the next 100 years. The path to such an outcome, however, is likely to be long, and negotiations will not be concluded within days.

A more realistic assumption is emerging: if talks do not begin by the end of the week, the six-week timeframe will become increasingly difficult to meet. In that case, a more pronounced market correction could follow.

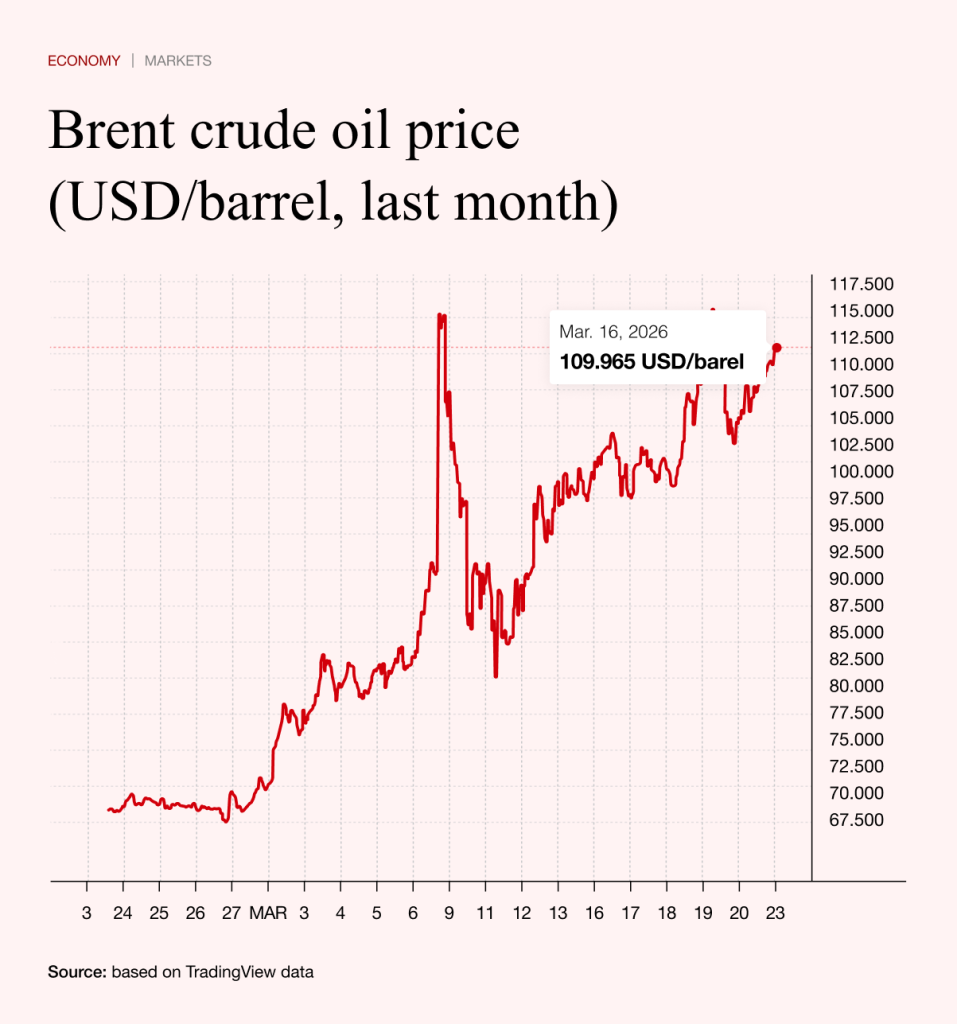

The widening gap between paper and physical oil

Despite Trump’s carrot-and-stick tactics, oil prices have risen at the start of the week, but without any dramatic surge. The upward trend is evident, yet it remains orderly for now.

A more serious issue is developing beneath the surface. Prices quoted on exchanges are, by their nature, largely virtual. What is traded are contracts, which only rarely result in physical delivery to the investor. Alongside this sits a separate price for physical oil – the price at which buyers actually take possession of crude.

Under normal conditions, the two move closely together, with only minimal differences. At present, however, the gap between them is widening significantly. The reason is that many countries, led by Sri Lanka, have virtually no oil left in their reserves.

The fundamental problem is that the world may soon begin to run short of physical oil. This is already reflected in concerns among airlines, which are uncertain whether flights between Europe and Asia can be maintained amid potential shortages of aviation fuel.

Early signs of reduced consumption are also emerging in Europe. Slovenia, for example, has introduced restrictions on large-scale purchases of petrol and diesel.

Brent crude is currently trading at USD 109 per barrel. Physical crude cargoes in Oman are selling for around USD 157 – the price at which buyers take delivery.

It is the price of physical crude that reveals the true state of the market. Even at these elevated levels, demand remains strong. In reality, the situation is more strained than headline prices suggest, and if conditions do not change within days, further increases are likely.

Bitcoin versus gold: market anomalies

Markets are sending warning signals, most clearly visible in the behaviour of gold and bitcoin. In a period of heightened geopolitical risk, risky assets would normally weaken, while so-called safe havens would strengthen.

That would imply falling bitcoin prices and rising gold. Instead, the opposite is happening.

Bitcoin has gained around eight per cent since the conflict began on 28 February. At one point, it even reached levels not seen for some time, implying an increase of roughly a fifth. Given its current position in the halving cycle, that performance is striking.

Even more surprising is the development in gold. Rather than rising sharply, the price has fallen by 21 per cent since the start of the conflict – a move few would have anticipated.

Several explanations are being discussed. One is that leveraged investors have been forced to liquidate positions in order to meet margin calls amid rising bond yields. Another is that markets expect a strengthening of the US dollar, suggesting that some investors believe in an eventual US victory.

A further hypothesis is that countries involved in the Gulf conflict are now divesting their gold reserves. A final, more controversial theory is that gold prices are being deliberately suppressed to prevent investors from shifting out of US ten-year bonds.

If demand for US government bonds were to weaken, that would pose another major challenge for Washington. It is therefore no longer sufficient to watch oil alone. Equal attention must be paid to gold prices and the yield on ten-year bonds.