Financial markets are once again gripped by a sense of déjà vu. Almost exactly a year ago, on 2 April 2025, Donald Trump launched his so-called ‘Liberation Day’ tariffs, a policy intended to shield American consumers from imported goods and reshape global trade.

The move initially triggered market turmoil. Trump held his ground for several days as equities fell, but reversed course when pressure spread to the bond market. Stocks quickly recovered, allowing the President to claim vindication and silence many of his critics. With visible confidence, the President was able to declare that, after all, he had predicted a happy ending. All that mattered was to believe him.

Will Trump reverse course again?

US markets have weakened in recent weeks, though not dramatically. Since 2 March, the S&P 500 has fallen by more than six per cent, a relatively modest decline given the scale of military action involving Iran. Early optimism that the conflict might be resolved quickly has begun to fade, however, as it becomes clear that the operation may take longer than initially expected.

Supporters of the administration argue that a timeline of four to six weeks was always envisaged. Markets, for their part, appear to be pricing in a similar assumption: that if conditions deteriorate significantly, Trump will intervene to stabilise the situation.

There have already been signs of this dynamic. Each time oil prices approached $110 per barrel, Trump sought to reassure investors, signalling that progress was being made and that a resolution was within reach.

Yet a more concerning signal is now emerging from the bond market, widely regarded as more disciplined and less reactive than equities. Unlike stock markets, which are often driven by sentiment, bond markets are dominated by large institutional investors operating under strict rules and models.

Bond yields raise alarm

US Treasury yields have risen sharply since the beginning of March, nearing 4.4 per cent after a jump of roughly 40 basis points. While that level is not unprecedented, the speed of the increase is striking and potentially destabilising.

Higher yields translate into more expensive borrowing for the US government, rising mortgage rates and falling prices for existing bonds held by banks as collateral. More importantly, they signal growing expectations of inflation. Sustained increases in yields suggest that markets anticipate either prolonged inflationary pressure or a delay in interest rate cuts.

Meanwhile, high rates represent a major obstacle to Trump's Make America Great Again economic agenda. Indeed, the bond market is already looking beyond the conflict in Iran, focusing on the longer-term consequences. When the war ends, those pressures are likely to become even more significant for the administration.

The broader fiscal backdrop is already fragile. US national debt surpassed $39 trillion in March 2026, and the conflict with Iran is adding further pressure. Initial estimates put the cost of the first week of military operations at around $10 billion. According to The Washington Post, the Pentagon has requested more than $200 billion in additional funding. These figures cover only direct military expenditure and do not account for wider economic effects.

In this context, the bond market is exerting increasing pressure on the Trump administration. If yields continue to rise despite the President's declarations of military progress, the economic consequences could outweigh any strategic gains.

Between negotiation and escalation

For now, markets remain cautiously optimistic. Trump has delayed the start of potential peace talks by five days, although military operations continue in parallel. While Iranian officials have denied that negotiations are under way, investors have seen similar patterns before, including during earlier trade disputes with China, where talks were initially denied before eventually materialising.

On the face of it, it seems that Trump can celebrate success in a field in which he is extremely confident: negotiation. Despite his unorthodox methods, it cannot be denied that he has an excellent command of business negotiations. The problem is that, in the case of Iran, it is not just about business, but above all about war and extremely intertwined geopolitical relations.

War, however, presents a far more complex challenge. Unlike business negotiations, geopolitical conflicts are shaped by deep-rooted grievances and strategic calculations that cannot easily be resolved through transactional agreements. Experiences in Ukraine, where Trump previously pledged a rapid resolution that did not materialise, underscore these limits.

In the case of Iran, the stakes are higher still. Tehran's ability to disrupt global energy flows gives it significant leverage, and the longer the conflict persists, the more uncertain the outlook becomes.

Markets look beyond the war

Alongside geopolitical tensions, markets have also been reacting to developments in the technology and financial sectors.

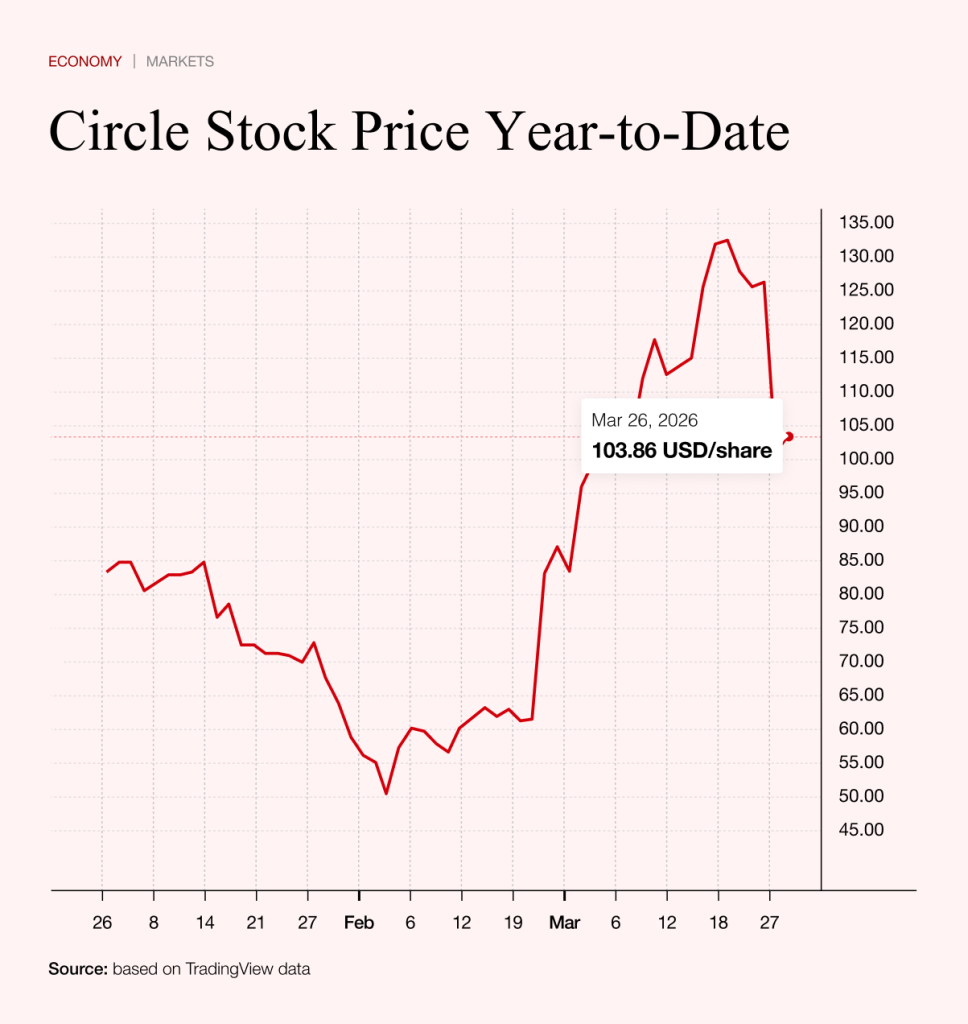

Shares in Circle and Coinbase fell this week following a revised version of the proposed Clarity Act, which aims to establish a regulatory framework for stablecoins. The updated proposal suggests that simply holding stablecoins may become less attractive, particularly if regulatory changes limit the returns currently generated through underlying assets such as US Treasury bonds.

This has raised concerns among banks, which fear that widespread adoption of stablecoins could accelerate the outflow of deposits from the traditional financial system. In an extreme scenario, such a shift could also weaken demand for US government debt, a cornerstone of the global financial system.

The regulatory response suggests that authorities are seeking to balance innovation with financial stability, even at the cost of reducing the appeal of emerging technologies.

A similar technological shock, albeit from a slightly different angle, hit the semiconductor sector. Shares in memory chip makers including Micron, Western Digital and SanDisk fell sharply after Google unveiled a new data compression algorithm, TurboQuant, which could significantly reduce the memory requirements of artificial intelligence systems.

Although investors were immediately spooked by the sudden cooling of the hardware boom and began selling in droves, seasoned analysts consider this panic to be greatly exaggerated. After all, the underlying need for data storage remains strong, and production capacity in the sector continues to be stretched.

Under normal circumstances, these developments would drive the front pages of market news, but today they remain a mere footnote in the context of war. Donald Trump is still the man in charge.