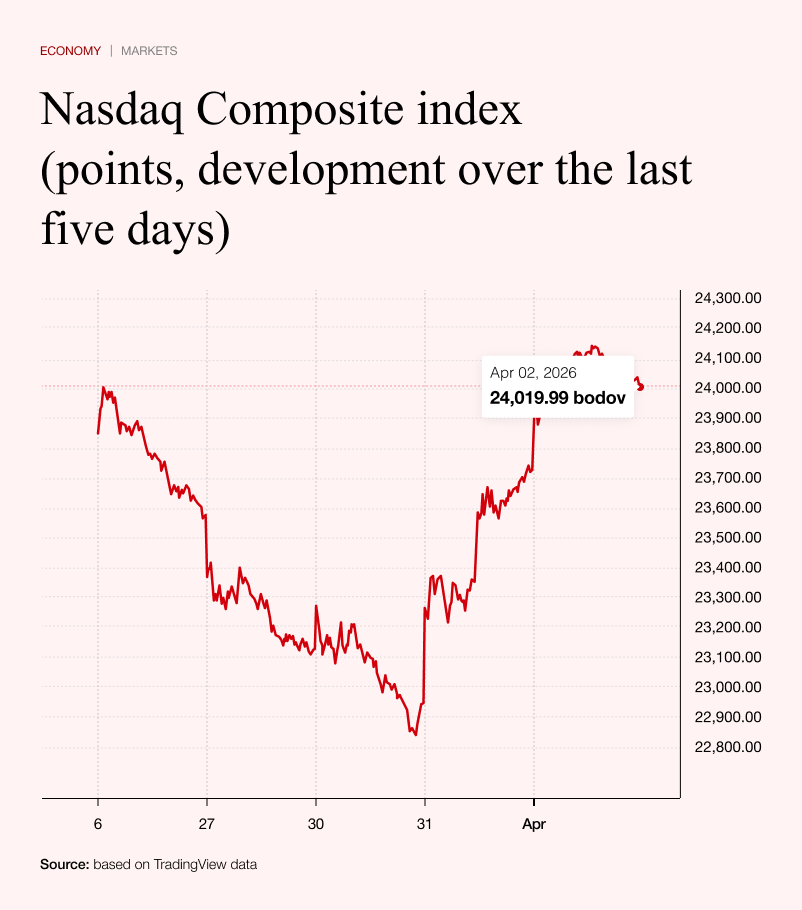

For five weeks, US stock markets have more or less resisted negative sentiment. Hardened optimists were sustained by the belief that Donald Trump does in fact have a plan.

Even if he does not, they have been counting on his negotiating skills as a seasoned businessman in the New York market. As time goes on, however, his method of constantly alternating between carrots and sticks is no longer working. Trump increasingly looks as if he is negotiating with himself rather than with Iran, which has consistently denied at official level that there have been any peace requests from his side. Doubts extend beyond that claim.

At the beginning of the week, Donald Trump said in an interview with the Financial Times that the Iranian regime had allowed 20 ships to pass as a ‘sign of respect’ for him personally. The statement is problematic on several levels.

First, Trump appears to have increased the number of boats from 10 to 20. Second, according to data from tracking services, no such passage has taken place. There is also no indication that such a group of tankers was ever waiting to pass through the Strait of Hormuz. This suggests a first clear detachment from reality.

A further problem lies in the underlying assumption that Iran would act in such a way. It is difficult to imagine that the Iranian regime would show respect to the American president at a time when it has been subjected to heavy bombing for more than a month.

Markets are increasingly uneasy that the man directing the operation is misreading the situation. His contradictory statements, once seen as part of a strategy to confuse the opponent, are now becoming a source of confusion in their own right.

Even speculators struggle to read the market

The market is shaped not only by optimists, but also by speculators. The latter have largely relied on the so-called Tacos theory – the assumption that Trump will ultimately yield to market pressure, reverse course when tensions escalate and do what investors expect. That would mean an end to operations and some form of deal.

Speculators were encouraged when Trump spoke of a peace deal being on the table and said he had found more reliable counterparts than the previous leadership. That narrative, however, faltered on 1 April. During the day, markets rallied on optimism after the White House suggested that the Iranians themselves had asked for peace.

Traders expected confirmation that this was a clear example of the Tacos theory in practice. Trump prepared his evening address, and overseas markets closed on a strong note. That confirmation, however, did not materialise. Instead, the opposite happened.

The US president once again threatened Tehran that unless it agreed to peace, he would send the country back to the Stone Age. At the same time, he said the operation would be completed quickly, within a week or two. This style of communication is now draining optimism from the markets, as similar messages have been repeated before.

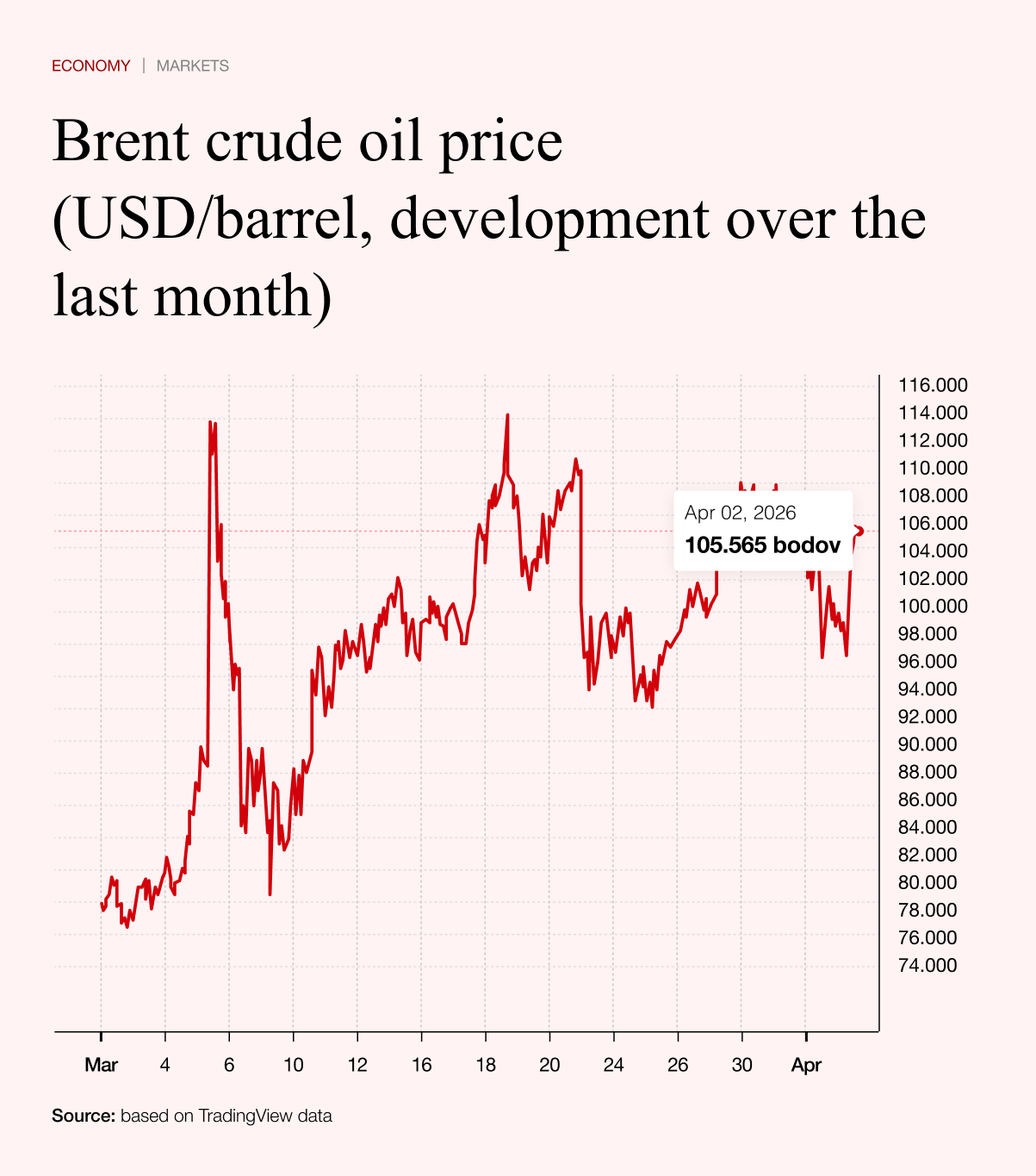

Overnight, oil prices rose sharply again, gaining more than five per cent. The Japanese stock market has once more fallen into the red. Markets are effectively back where they started, except that the world has endured a month of elevated oil prices. Concerns are mounting. In addition, stock exchanges will be closed from Friday to Monday for the Easter holidays, giving the US and Israel room to intensify the conflict without immediate market reaction.

Europe edges towards stagflation

The inflation dynamic is beginning to show in macroeconomic data. European Union countries have released price estimates, with inflation accelerating from 1.9 per cent to 2.5 per cent across the eurozone. This was driven largely by Germany, where inflation reached 2.7 per cent in March.

However, rising prices are evident across the region. In France, although inflation has not yet reached two per cent, it accelerated from 0.9 to 1.7 per cent.

That poses a serious problem. Inflation in France has so far remained subdued, largely due to weak economic growth. Slow growth combined with rising prices creates the classic conditions for stagflation – a situation that is difficult to resolve because central banks have limited room for manoeuvre.

Until higher oil prices fully feed through into lower GDP, central banks would normally raise interest rates to counter inflation. However, their ability to act is constrained, as monetary policy cannot directly influence oil prices.

In addition, Donald Trump has taken the position in recent days that reopening the Strait of Hormuz is no longer a US concern and that Europeans must deal with the situation themselves. This stance adds further pressure on Europe to take a clearer position in the conflict.

Where is the safe haven?

The biggest problem for investors at present is that there is no place to hide. Market nervousness is high, and equities remain vulnerable.

In the past, when stocks performed poorly, investors could turn to US Treasuries. However, yields on US ten-year bonds are also rising sharply. As yields rise, bond prices fall, limiting their role as a refuge.

Gold, which usually serves as a safe haven in times of war and rising inflation expectations, is also weakening. It has fallen by more than 14 per cent since the conflict began.

One reason is that the Turkish central bank has sold large amounts of gold in an attempt to stabilise its currency. Other countries in the region may follow, increasing supply and putting further pressure on prices.

Other alternatives, such as bitcoin, are also unattractive. The cryptocurrency remains in a bear market and, if past patterns hold, a recovery is unlikely before late summer.

Support from the ‘Magnificent Seven’ stocks, a pillar of recent market performance, is also fading. These large technology companies, expected to benefit from artificial intelligence, have lost more than 12 per cent since the beginning of the year.

Investors, in short, have nowhere to hide. The only option is to hold cash and wait – which is why the US dollar has emerged as the only clear winner of the current situation.