One of the secrets of stock market psychology is that markets do not like uncertainty. They can cope with a few pieces of bad news or a quick change in trend, but the worst outcome for them is an increase in uncertainty and unpredictability.

This unpredictability was epitomized by Donald Trump at the start of the Iran crisis. Even a single social media post by the US president increased tension and volatility. Over time, however, markets became accustomed to this carrot-and-stick strategy.

It seemed that the news of a two-week ceasefire and subsequent peace talks would mark the final stage. However, negotiations in Islamabad failed. On Sunday evening there was further news from the White House, which wants to increase pressure on Iran by blocking ships that Tehran has so far allowed to depart, primarily tankers bound for China. This is further bad news for markets.

The Price of Predictability

However, this is where predictability comes in. Markets have become accustomed to conditions changing almost every minute. What matters is that their behavior remains predictable, and that has proved to be the case.

Oil has returned to above $100 per barrel. As a result, prices across the energy sector are rising. By contrast, shares in companies that rallied last week have fallen. Losses were recorded in airlines such as Air France, Ryanair and Lufthansa.

The luxury goods sector also weakened. Outside sectors directly affected, however, there is general calm.

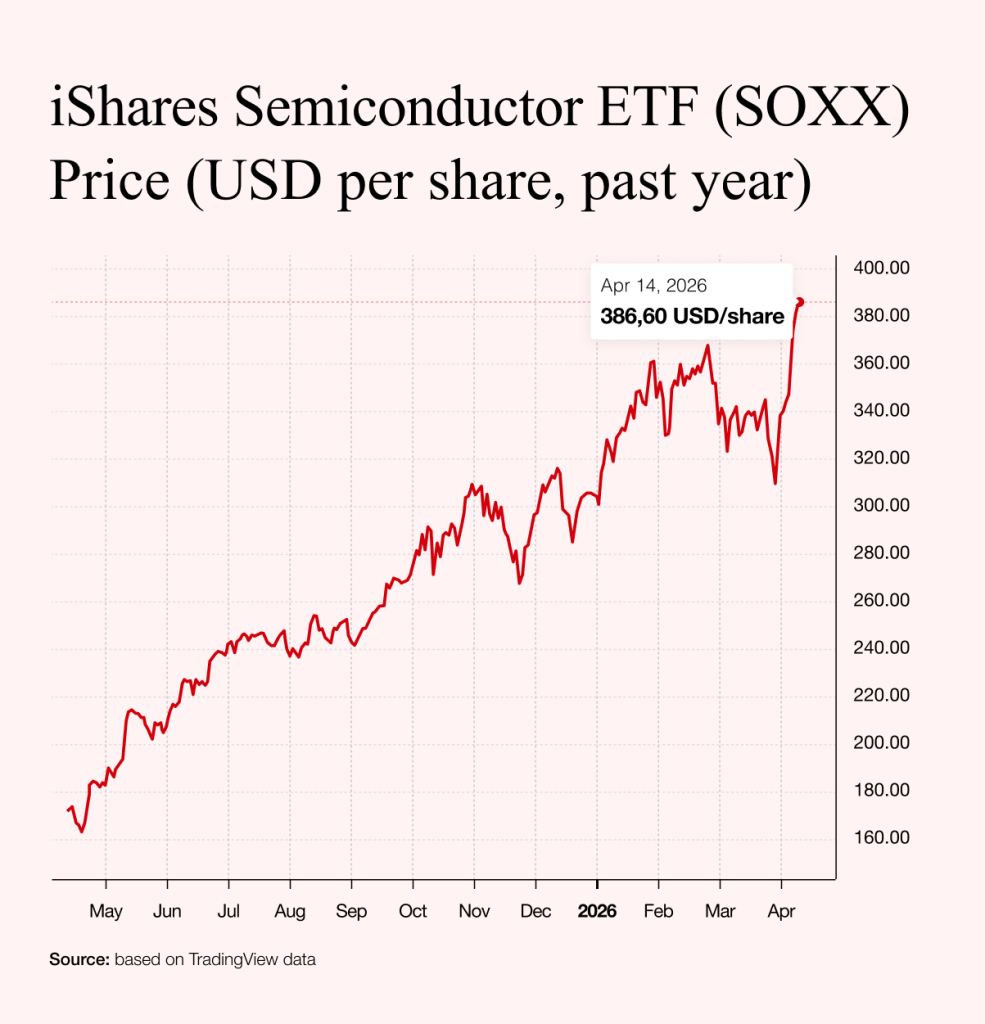

This is illustrated by the performance of the SOXX index, which aggregates companies in the semiconductor sector. Despite a possible helium shortage, the index is at all-time highs. The war in Iran has not weakened faith in the digital future but, on the contrary, strengthened it.

Despite all the potential consequences of the Iranian conflict, an important part of the market is ignoring it. Many investors have moved funds into the perceived safe haven of the semiconductor sector.

This may reflect not only resilience, but also speculation that, if there is a ceasefire between the US and Iran, technology stocks would rise first. At the same time, however, there is a medium-term risk that markets are currently ignoring: stagflation.

The Return of the Inflation Scarecrow

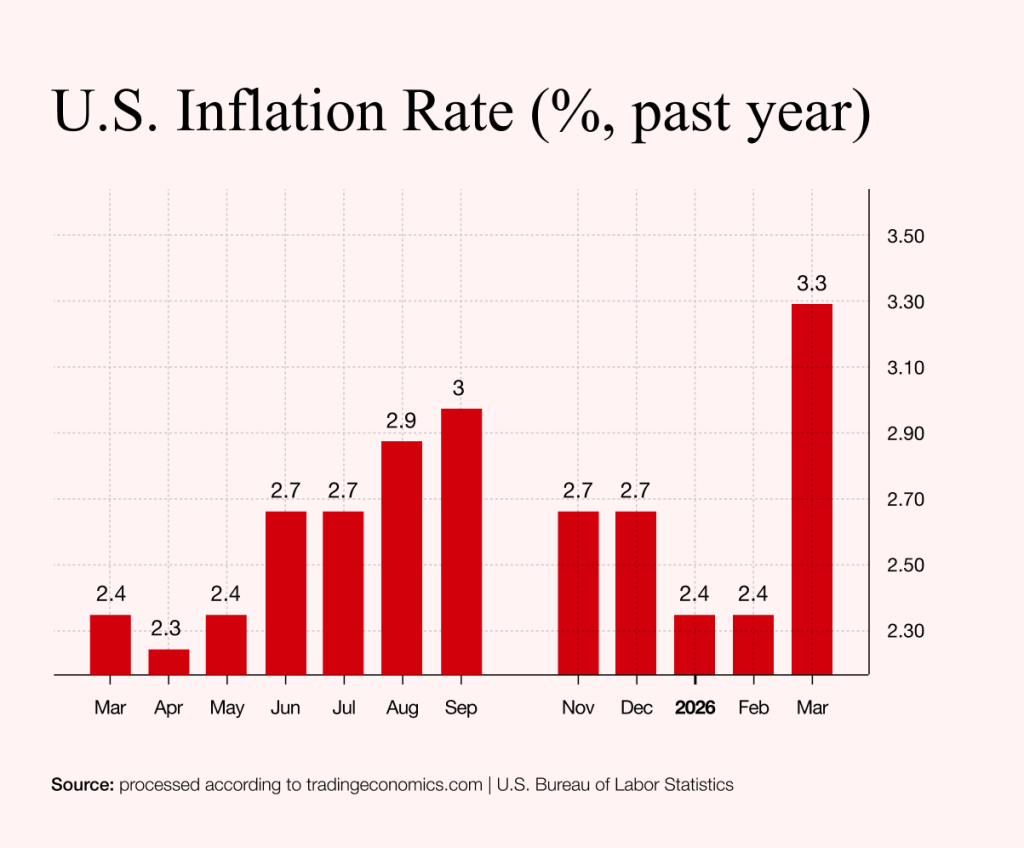

At the end of the week, inflation data from the US were released. For completeness, inflation also rose in Europe in March, particularly in Germany, where it reached 2.9% for the first time in a long period. The only positive news from the US was that the figures were broadly in line with analysts’ forecasts.

Inflation is rising, but not yet uncontrollably. Nevertheless, US inflation in March 2026 again delivered an unpleasant surprise. It accelerated to 3.3% year on year, the highest level since May 2024, after 2.4% in the previous two months.

The main driver was energy: prices rose by 12.5%, mainly due to gasoline increasing by 18.9% and heating oil by 44.2%. The jump was largely due to the military conflict with Iran, which once again showed how quickly geopolitical turmoil is transmitted to households’ wallets. Inflation is therefore above the 2% target.

The rise in energy prices is a primary phenomenon that was to be expected, and no central bank – not even the US Federal Reserve – is likely to counter it directly. Oil prices are now determined by geopolitics. The problem is that once energy prices remain elevated over a longer period, as they have for two months, behavior begins to shift in an inflationary direction.

Price increases will gradually be passed from the energy sector to others. Given that households have vivid memories of the last inflationary wave, which began in 2022, they will expect central banks to intervene.

This is where markets will make decisions. Once it becomes clear that central banks will adjust monetary policy, a wave of sell-offs could hit equities. The situation is not entirely straightforward, however, because tighter monetary policy would also affect the geopolitical balance, particularly with regard to Iran.

The fight for time is now being played out in the Strait of Hormuz, even as inflation rises and Donald Trump makes no secret of his preference for rate cuts.

Political pressure on the central bank is currently enormous. A decision may be postponed for a month or two, but there is then a risk of repeating the previous inflation cycle, when central banks delayed tightening for too long.

Markets are therefore witnessing a dangerous race against time, in which the eventual winner will be whoever exits the stock market merry-go-round early enough.

The President as Market Influencer

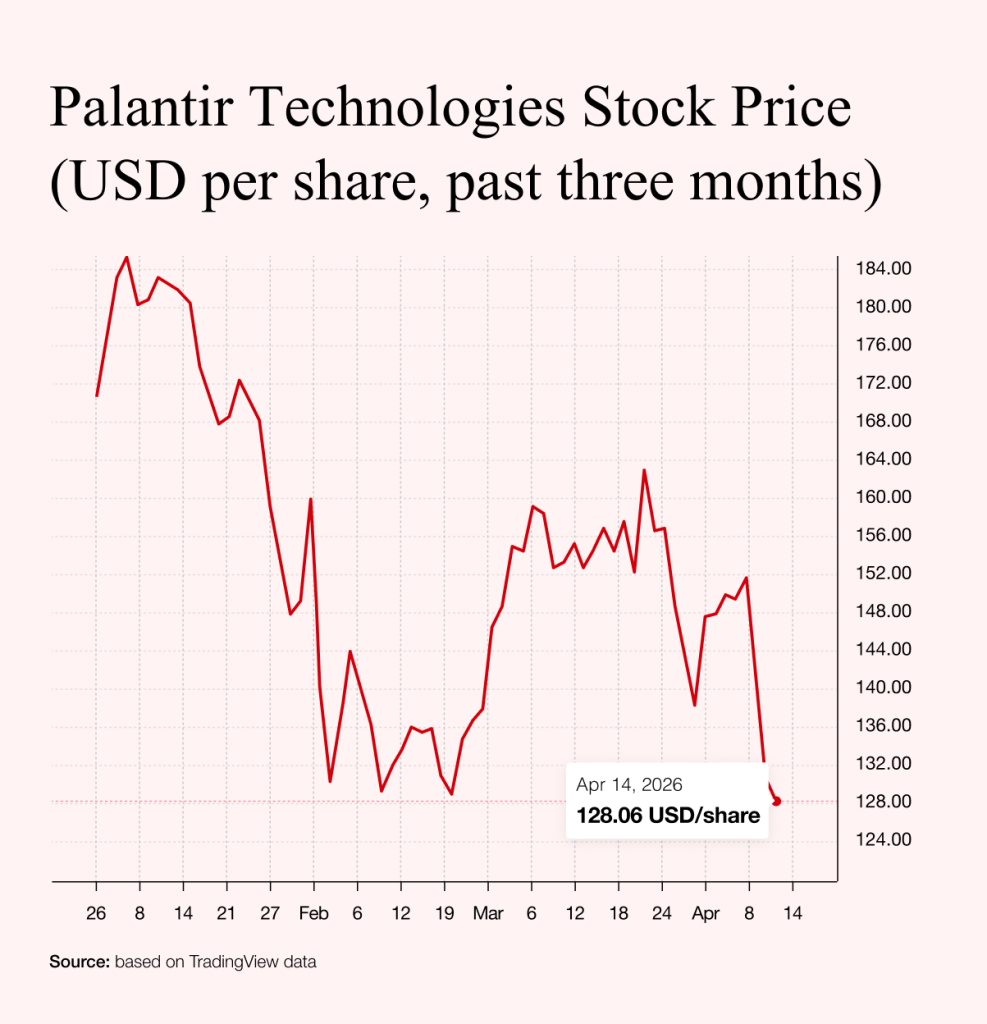

Donald Trump briefly turned investment analyst and offered followers a stock tip late last week. On his Truth Social platform, he praised Palantir, saying the company had shown strong warfare capabilities, and even added the ticker symbol PLTR.

In doing so, he behaved more like a financial influencer than a president. The timing was striking: Palantir’s stock had just recorded its worst week in more than a year, plunging 14%.

Trump has therefore once again stepped onto thin ice. There is widespread suspicion that well-informed traders may have profited from his shift. Yet he behaved as he often does. Rather than dispelling suspicion, he added a specific investment tip.

Palantir plays a major role in the ongoing war. Its business depends heavily on government contracts, and it is also among Trump’s donors. The conflict of interest is clear.

Even the president’s statement, however, was not enough to change the trend. The issue is not only White House goodwill but also the valuation: the stock’s P/E ratio stands at 202. It is therefore an extremely expensive stock, making even Nvidia appear conservative by comparison.

For a symbolic punchline, short seller Michael Burry continues to bet against the stock, arguing that its fundamental value lies well below $50. This suggests there is no shortage of sceptics around Palantir.