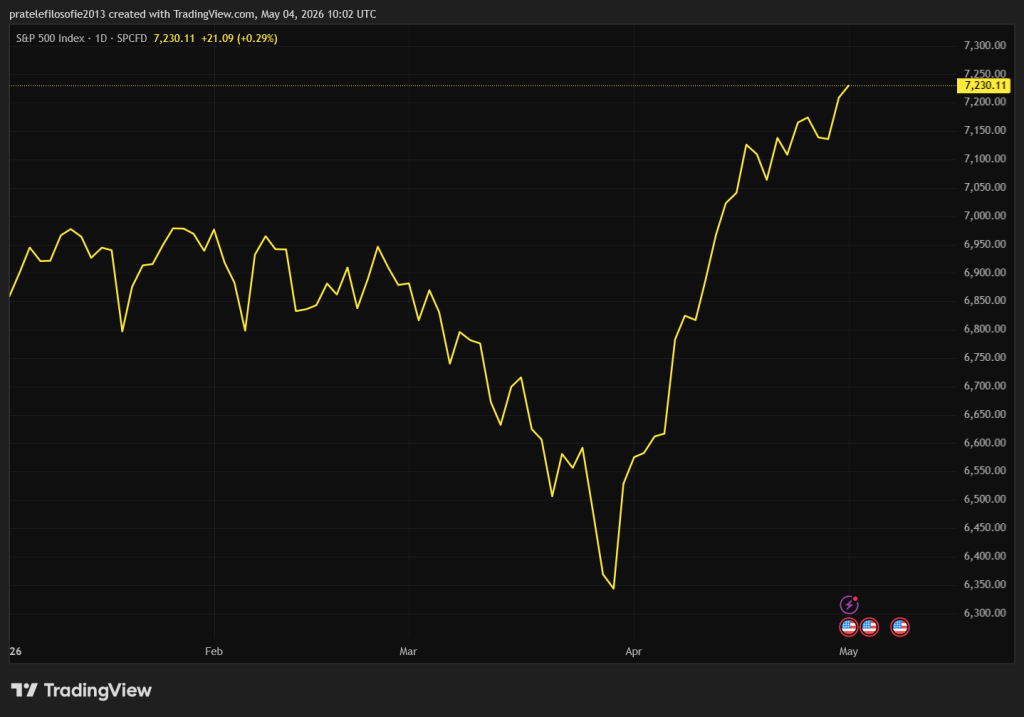

US financial markets have once again exposed the widening gap between economic reality and market behavior. April 2026 was the strongest month in history for the S&P 500 – a remarkable rally that says as much about investor psychology as it does about fundamentals.

The index rose roughly 10.4% over the month, its best performance since November 2020. On the surface, the surge appears easy to explain: the artificial intelligence boom continues to deliver. The latest earnings from major technology firms confirmed that the investment cycle in AI is not slowing – if anything, it is accelerating.

Amazon, Alphabet, Microsoft and Meta are pouring unprecedented sums into data centres, chips and cloud infrastructure. Combined capital expenditure could reach as much as $725bn in 2026, up roughly 77% year-on-year. Amazon alone is heading towards $200bn, while Microsoft and Alphabet are each approaching $190bn. Meta has raised its own outlook to between $125bn and $145bn.

Only Apple stands somewhat apart, investing less in physical infrastructure and more in software, chips and partnerships. But even that distinction does little to change the broader picture: capital is being deployed at a scale rarely seen outside wartime economies.

Unsurprisingly, chipmakers have surged alongside this spending boom. Stocks such as Nvidia and Intel have reached new highs. Under normal circumstances, such valuations might be justified.

Geopolitics and Inflation: The Risks Markets Ignore

The Strait of Hormuz – one of the world’s most critical energy chokepoints – has effectively ceased functioning. Traffic has collapsed since late April, and by early May, shipments had all but stopped.

At the same time, tensions between the United States and Iran continue to escalate. While diplomatic signals have emerged – with Tehran putting forward proposals that allow negotiations to resume – this is more about optics than finding a resolution. It offers political cover, not stability.

Each additional day of disruption carries a clear economic consequence: rising inflation.

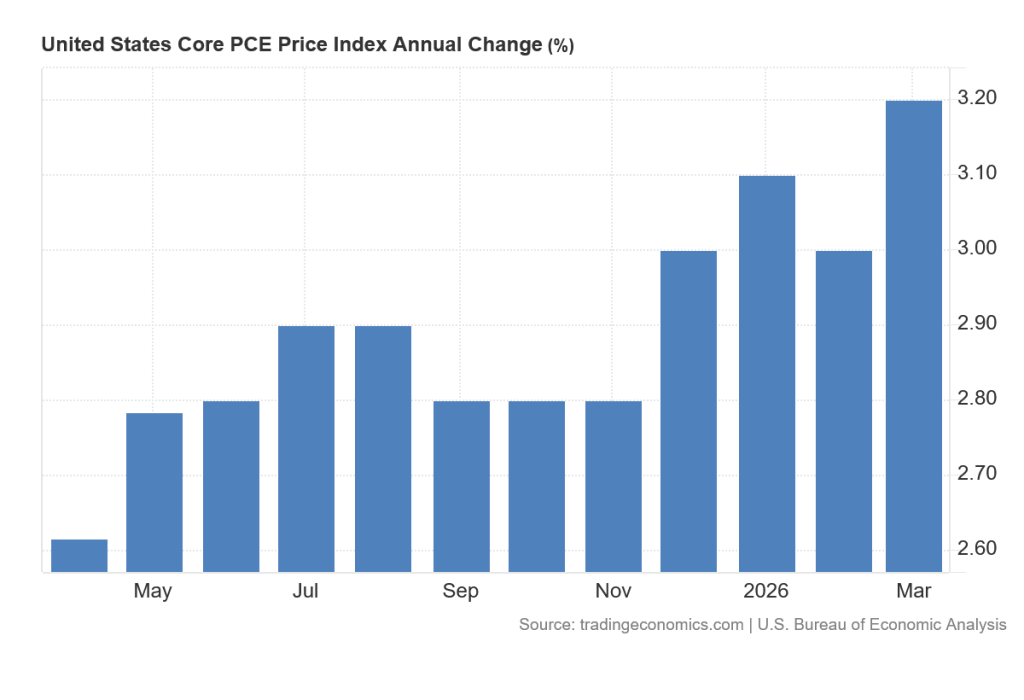

The latest data confirms it. US core Personal Consumption Expenditures (PCE) inflation – the Federal Reserve’s preferred measure – stood at 3.2% in March, well above the 2% target. Crucially, this measure excludes energy and food, the very components now surging.

In other words, inflation is no longer confined to volatile sectors. It is spreading across the economy.

Given persistently high energy prices throughout April, there is little reason to expect improvement in the next reading. Inflation is not easing, it is embedding itself.

For Donald Trump, this presents a political problem as well as an economic one. A core part of his electoral base expected relief from rising living costs. Instead, the geopolitical escalation with Iran is pushing prices higher.

Central Banks Caught in a Trap

Central banks are now boxed in. The Federal Reserve, the European Central Bank and the Bank of Japan have all opted to hold rates steady. But this pause reflects uncertainty, not confidence.

ECB President Christine Lagarde made it clear that rate hikes remain on the table. Within weeks, policymakers will have to decide whether inflation risks outweigh the already fragile state of economic growth.

For Europe, the stakes are particularly high. The economy is stagnating. A tightening of monetary policy would not only suppress growth further, but could also reignite tensions in sovereign debt markets, particularly in countries like France.

The dilemma is stark: fight inflation and risk recession, or tolerate inflation and risk losing control altogether.

Meanwhile, US equity markets continue to climb.

Apple and the Market Paradox

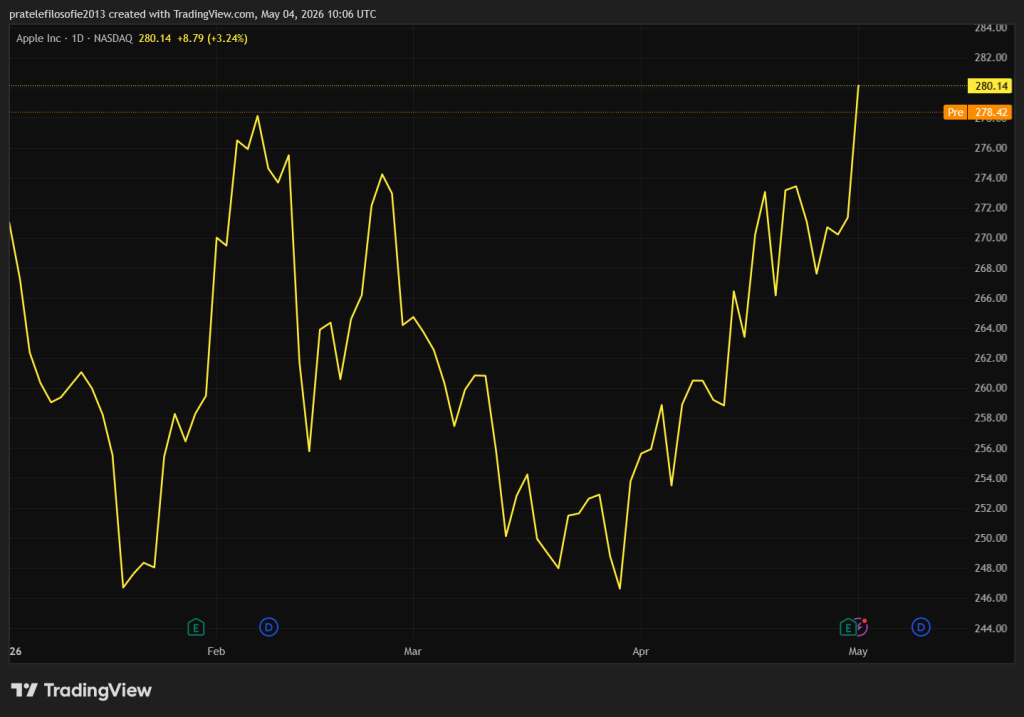

The disconnect between markets and reality is perhaps best illustrated by Apple.

Despite mounting macroeconomic pressures, the company’s shares rose nearly 5% following its latest earnings. The reason was not strong fundamentals, but financial engineering: a $100bn share buyback program and a dividend increase.

This is what the market wanted – and what it rewarded.

Yet beneath the surface, the picture is less reassuring. Apple’s capital expenditure on infrastructure remains modest compared to its peers, but its research and development spending has surged to a record $11.4bn as it builds out its AI strategy.

More importantly, cost pressures are mounting. Demand from hyperscalers for memory chips is driving prices sharply higher. Even Apple is not immune.

Its product gross margin declined by 200 basis points quarter-on-quarter, despite slightly beating expectations overall. Tim Cook himself acknowledged that rising input costs – particularly in memory – will weigh on the company in the months ahead.

The message is clear: even the strongest companies are feeling the strain.

Markets Detached from Reality

And yet, markets continue to behave as if none of this matters.

Record equity valuations, persistent inflation, geopolitical escalation and tightening financial conditions are all moving in the same direction. But investors remain focused on a single narrative: growth driven by AI.

For now, that narrative is enough, but it rests on an increasingly fragile foundation. What we are witnessing is not a reflection of economic strength, but a suspension of disbelief – a market willing to ignore risk as long as the story holds. The illusion of prosperity remains intact, but the question is how long it can last.