After Sweden abolished inheritance and gift taxes in 2005, private firms with potential family successors grew faster, invested more and paid higher corporate taxes than comparable firms without natural heirs, according to a new study.

The findings challenge a widespread argument in Western societies that tax cuts in this area reduce government revenue and mainly make the rich richer. In Sweden’s case, the opposite appears to have happened. Investment increased, and so did corporate tax payments, as firms no longer had to hold back capital as a reserve for future tax liabilities and could put it to productive use instead.

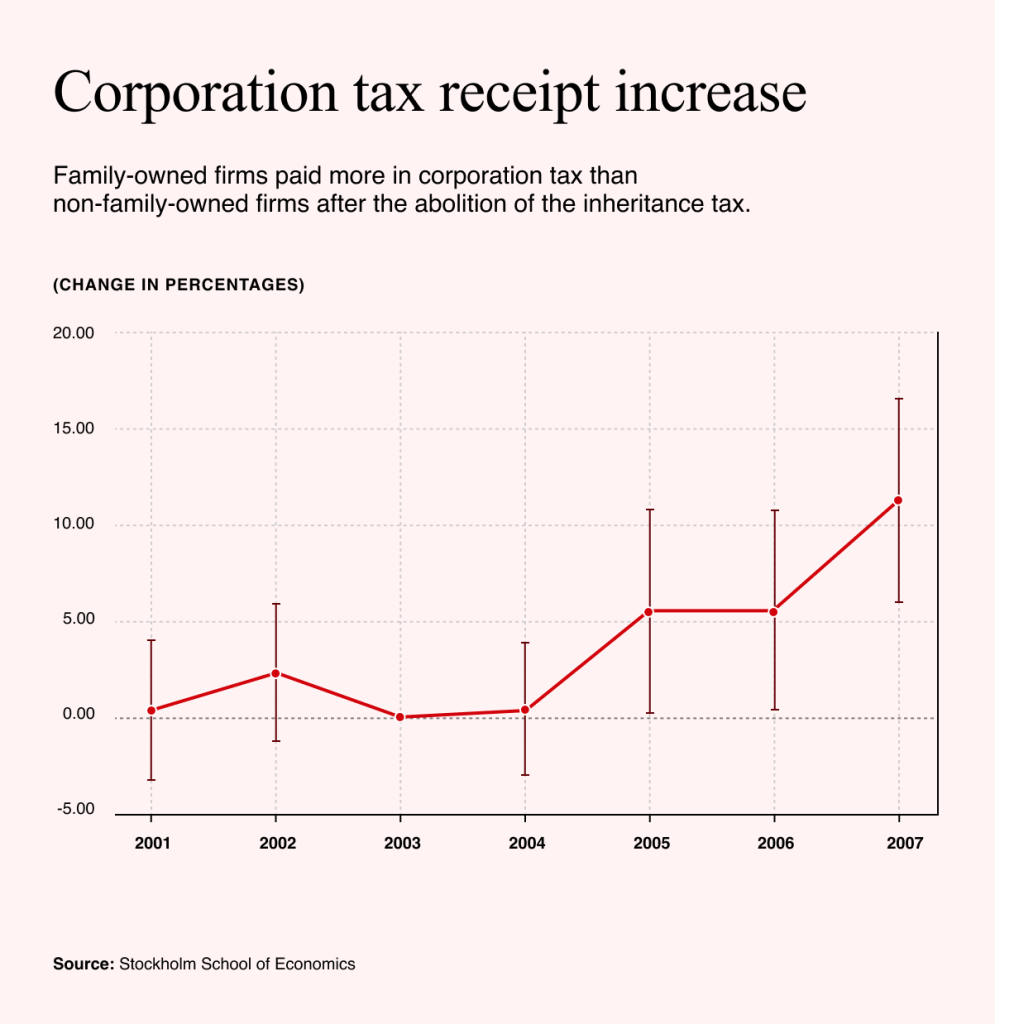

Higher Investment, Higher Tax Revenue

The study, published on 27 April by the Stockholm School of Economics, says the reform appears to have “incentivized and enabled stronger growth and earnings power for private firms that had the prospect of being handed over to the next generation”. The paper was co-authored by Professors Mateja Andric, Mohamed Genedy and Mattias Nordqvist. It examines how the abolition of gift and inheritance taxes affected firm strategy and performance in Sweden.

The firms’ improved profitability led to “long-term benefits to society” through “substantial” increases in salaries and corporate tax payments, the study found.

By 2007, firms with natural heirs had increased salaries at a rate 12% higher than comparable firms without successors, relative to the pre-reform baseline of 2003.

The authors argue that this points to a “meaningful and growing labor market footprint”, which should be taken into account by policy makers. Similarly, corporation tax paid by firms with natural heirs grew at a “substantially higher rate” than that paid by firms without natural successors.

The authors add that, rather than “eliminating [public revenue] entirely”, abolishing inheritance tax meant the state may benefit from recurring public revenue, instead of the previous one-off tax take. Sweden is one of the few European countries to have abolished inheritance tax, along with Austria and Norway.

Tax Reform

As pressure mounts on Europe to maintain its competitiveness, countries such as Britain, Germany and Spain are starting to debate inheritance tax reforms.

For instance, in late 2025, the Labour government proposed reforms in Britain that would see the threshold for 100% relief on agricultural and business property combined increase from $1.36m to $3.41m.

Meanwhile, in Spain, the capital city of Madrid offers a 99% reduction in inheritance tax for close family heirs, as part of a package of tax cuts introduced by Isabel Díaz Ayuso, president of the Community of Madrid. Madrid is one of 17 autonomous local councils in Spain, endowed by the constitution with a variety of powers including education, healthcare and taxation.

By contrast, in Germany, the Social Democratic Party (SPD) is moving to tax heirs of large fortunes more heavily by abolishing the current tax relief for business assets and replacing it with an allowance of $5.89m for such assets.

The contrasting reforms highlight what the authors describe as the “ideological” nature of the debate around inheritance tax. The tax is typically defended as a policy aimed at promoting equality of opportunity by limiting dynastic wealth, curbing the inactive accumulation of wealth across generations and counteracting wealth concentration, the study notes.

Common arguments for abolishing the inheritance tax include the risk of double taxation, where assets are taxed when earned and then again when they are transferred to the next generation; the complexity in the valuation of assets; and the creation of opportunities for tax planning that can lead to tax avoidance and incur high unproductive administrative costs.

Policy Debate

In this context, the study offers empirical evidence in a “critical” policy debate often “dominated by ideology”, according to the authors.

Using data covering about 37,000 companies, the study compared the financial performance of firms led by owners with children, which the authors argue indicates possible succession candidates, with firms led by childless owners.

The research covers the years between 2001 and 2007 inclusive, three years before and after Sweden’s inheritance tax was repealed.

“Before the reform, owners often had to plan for future tax payments tied to inheritance”, said co-author Mattias Nordqvist, professor at the House of Innovation, Stockholm School of Economics. “That may have limited how much capital they reinvested. After the tax was removed, the firms retained more earnings and invested more in growth.”

Prior to the 2005 reforms, inhertance tax rates in Sweden were “progressive”, ranging from about 10%–30% for close relatives and reaching as high as 50%–60% for more distant heirs. For comparison, inheritance tax in Britain ranges from 0%–40%, in Germany from 7%–50% and in France from 5%–45%.

Sales Increase

Following the tax abolition, sales at firms with potential successors were up by 8% in 2007 compared with heirless firms. These firms also increased total assets at a 4% higher rate and grew equity by up to 7% more, relative to the pre-abolition baseline year of 2003, the study found.

They also improved the operating margin by nearly half a percentage point more in the first two years before the difference levelled out in 2007. Corporate tax payments also rose more, with a difference of 10% over three years, and employee salaries grew at a 12% higher rate in 2007 relative to the control group.

The findings suggest that rents from the tax abolition were “not simply appropriated by the owner-managers but instead shared with society through taxes and employee salaries”, according to a spokesperson for the Stockholm School of Economics.

“Our study also points to long-term benefits to society from these increases in earnings power as we found that the reform resulted in higher corporate income taxes paid among firms with potential successors. The abolition of the gift and inheritance tax thus incurred a strengthening of recurring tax revenues from these firms.”