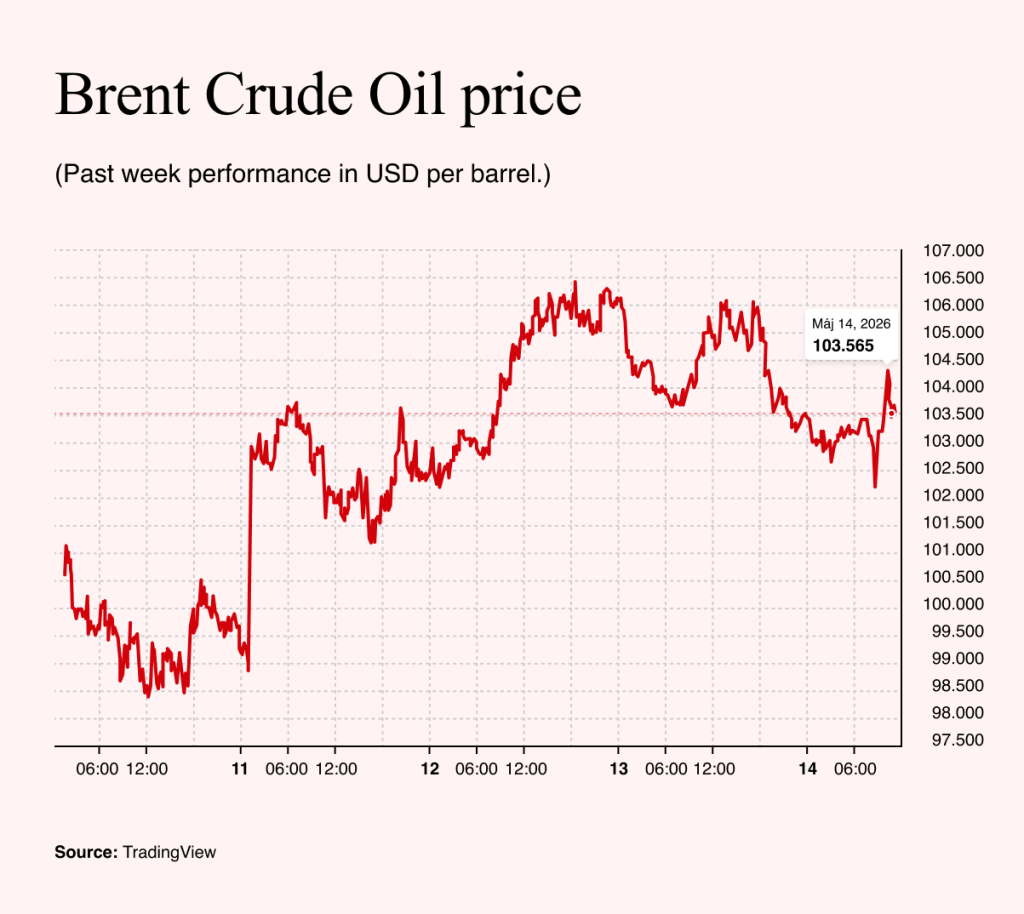

Financial markets continue to operate in a widening disconnect from geopolitical reality. The new week began on a cautious note, driven largely by developments around Iran. Donald Trump dismissed Tehran’s response to the US peace proposal as “totally unacceptable”, accusing it of “playing games”. Oil prices reacted immediately, climbing back above $100 per barrel.

Trump has also found a way to frame the current price level as a success. He argues that oil remains “low” because the most extreme forecasts – which saw prices rising to $250 per barrel if the Strait of Hormuz were closed – have not materialized.

The US president has a clear talent for recasting unfavorable outcomes. In doing so, however, he shifts the benchmark: success is no longer cheap oil, but simply the avoidance of the worst-case scenario.

This interpretation overlooks a central point. It was Trump who authorized US involvement in the strikes on Iran, contributing to the current crisis. He is now credited with containing a situation he helped to create.

The fact that oil prices have not surged further reflects not calm markets, but temporary buffers. Increased US exports and reduced Chinese imports have helped offset supply disruptions, masking underlying fragility.

Morgan Stanley describes the situation as a “race against time”. According to the bank, US exports rose by 3.8 million barrels per day, while Chinese imports fell by 5.5 million, together covering a shortfall of 9.3 million barrels. If the Strait of Hormuz remains closed for longer, these buffers will erode. In that case, $100 oil may prove to have been only a temporary reprieve before a renewed price shock. Signs of this pressure are already appearing in macroeconomic data.

Inflation Returns to the Fore

Throughout the Iranian crisis, markets have continued to price in an optimistic outcome in which the Strait of Hormuz reopens and conditions normalize. Yet the disruption has lasted long enough to begin feeding into economic data.

Last week, investors took comfort from stable US employment figures, despite the rapid integration of artificial intelligence into business processes. From that perspective, there was little immediate cause for concern.

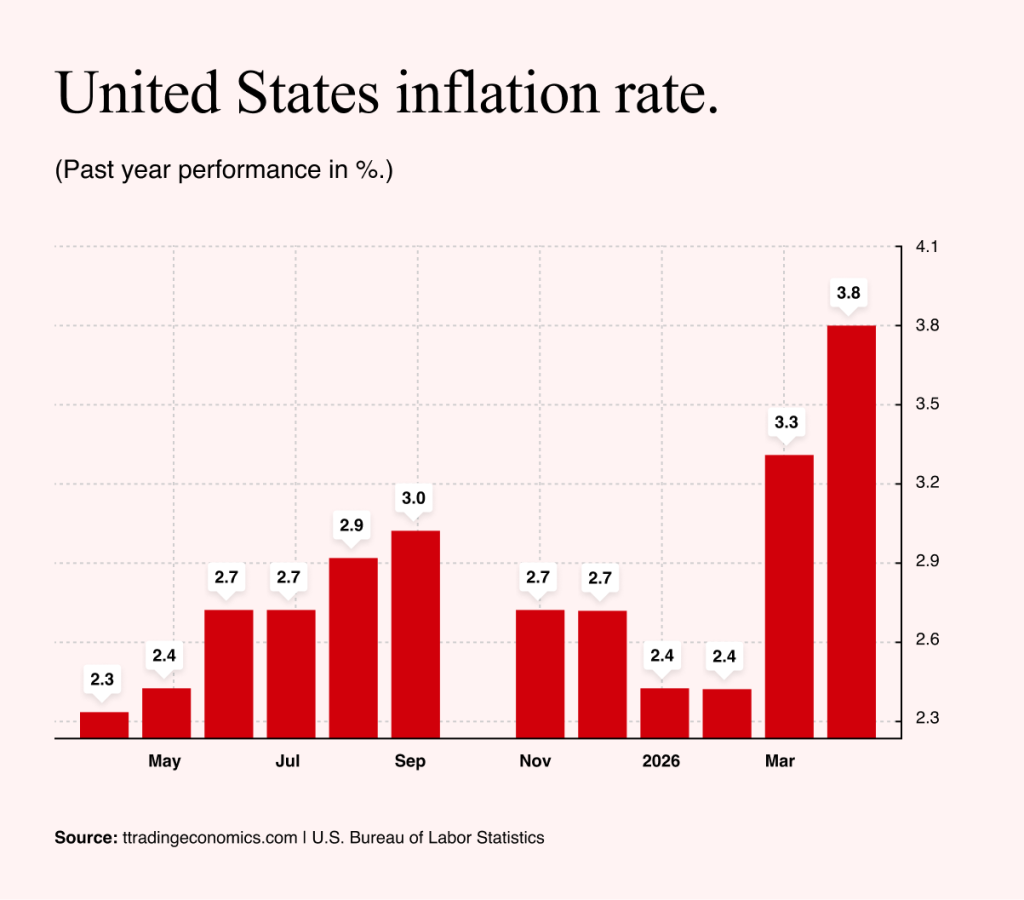

This week, however, inflation returned to the spotlight. The data was far less reassuring. Headline inflation rose to 3.8% in April, the highest level since May 2023 and above expectations of 3.7%. On a monthly basis, price growth slowed to 0.6% from 0.9% in March, but the overall pace remains elevated.

The driver is clear: the disruption of global energy flows through the Strait of Hormuz. Brent crude has climbed from around $70 per barrel to above $100 since the conflict began, with direct consequences for households. Petrol prices are up 28.4% year on year, airline tickets 20.7% and food 3.2%. Beef prices have risen even more sharply, by 14.8%.

This is not merely a commodity market story. Through transport, logistics and energy costs, oil prices feed directly into household budgets. If the crisis persists, further increases are likely.

Unlike the post-pandemic inflation surge, households are not entering this period with significant savings or pent-up demand. Instead, rising prices are hitting at a time of limited financial buffers.

The result is a classic squeeze. Consumers face higher costs for essentials such as fuel, transport and food, while other household expenses also rise. Inflation could therefore begin to weigh on consumption and economic growth, potentially pushing the economy toward recession. Wage growth has already lagged behind price increases, leading to a decline in real purchasing power.

At the same time, the US Federal Reserve faces limited room for maneuver. Despite political pressure and market expectations, it cannot easily justify cutting interest rates under current conditions.

Markets initially responded with a sell-off, particularly in technology stocks such as Intel and Qualcomm, as investors moved to lock in gains. The Nasdaq fell by more than 2% at one point.

Yet, as often in recent months, the decline was short-lived. Algorithmic trading strategies quickly shifted toward buying the dip, limiting losses by the close.

Markets continue to treat any significant decline as a buying opportunity. This approach has proved profitable over the past year, reinforcing investor confidence. Once again, bullish sentiment prevailed.

The Risks of Persistent Optimism

By midweek, concerns over inflation had largely faded, with attention shifting to the upcoming meeting between Donald Trump and Chinese President Xi Jinping.

Paradoxically, both sides have strong incentives to project stability. Domestic pressures in both economies increase the need to signal progress, making a breakdown in talks unlikely. Markets are well aware of this dynamic and may continue to rally in the near term.

However, this optimism carries risks.

A sustained rise in equity markets gives the White House greater latitude to escalate pressure on Iran without immediate financial repercussions. As long as markets remain resilient, geopolitical risks can appear manageable.

The longer this disconnect persists, the greater the potential correction. If markets continue to underestimate the economic consequences of the crisis, the eventual adjustment could be severe.