The European economy is not facing one crisis. It is facing several at once: energy, fiscal, industrial and political. Low growth, expensive energy, rising inflation and high debt are not the causes of European weakness, but its consequences. They point to an older disease. Europe is losing the ability to produce the wealth that paid for its welfare state, its influence and its illusion that it could make the rules for the world.

The crisis over Iran only accelerates the problem. After the loss of cheap Russian gas and Nord Stream, Europe no longer has the energy cushion on which its industrial model long rested. It has to pay the market price for energy at a time when competitors in the US and Asia often enjoy more favorable conditions. The impact is visible not only in household bills, but above all in the costs faced by factories, chemical plants, steelworks, carmakers and farmers.

The European Commission’s outlook is therefore not encouraging. In its Spring 2026 Economic Forecast, published on 21 May 2026, the Commission expects weaker economic activity. High energy prices are again pushing inflation higher, as confirmed by Eurostat figures showing that inflation in the eurozone rose to 3% in April 2026 from 2.6% in March. Unsurprisingly, energy recorded the sharpest year-on-year increase, rising by 10.9%, up from 5.1% in March.

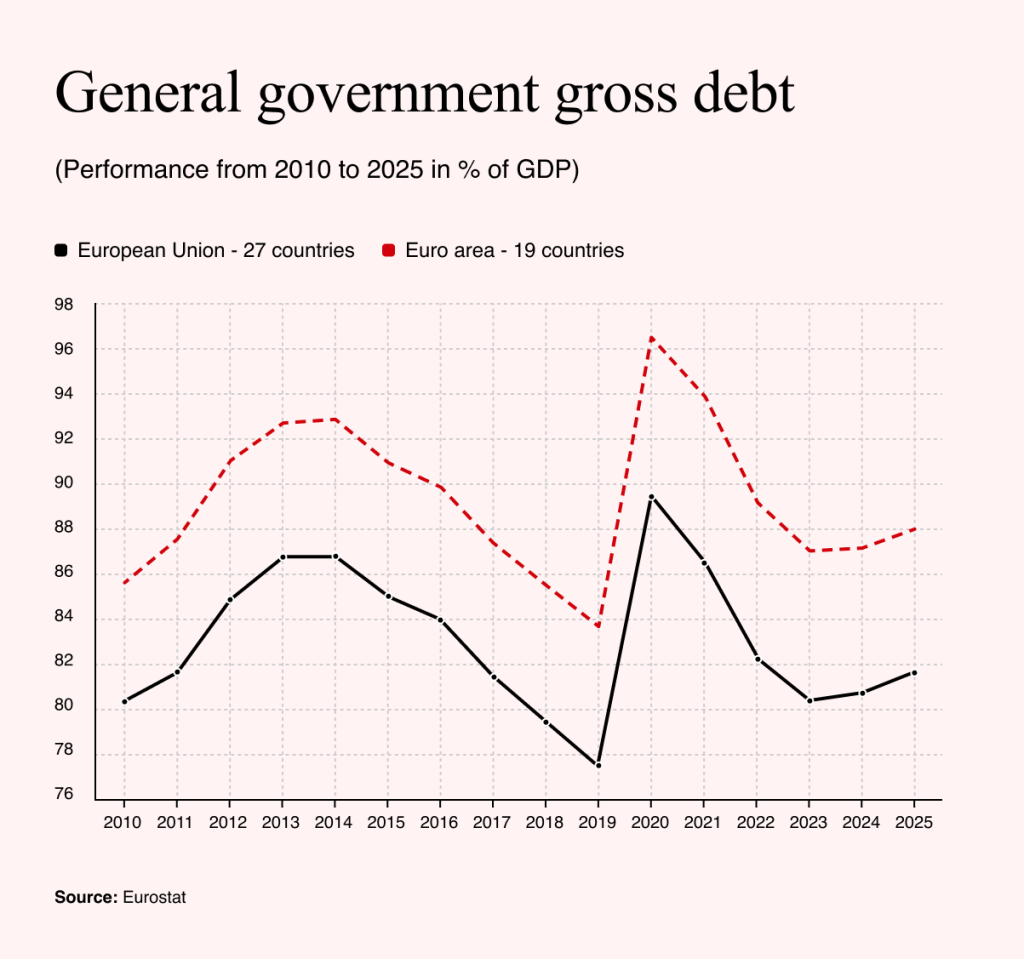

Adding to the unfavorable outlook is Europe’s familiar debt malaise. According to Eurostat’s latest annual data, public debt in the eurozone stood at 87.8% of GDP in 2025 and at 81.7% of GDP in the EU as a whole. Greece, Italy and France still had the highest debt levels, while Germany, by contrast, was in a different fiscal league, with debt of roughly 63.5% of GDP.

At first glance, the figures seem to suggest that Europe is returning to the old story of a responsible north and a debt-ridden south.

A New Economic Geography

But that would be a mistake. The map of Europe no longer overlaps with the old division between northern virtue and southern irresponsibility.

Spain is growing faster than Germany. Poland is operating more dynamically than France. Italy still has an industrial base that many countries would envy, but it carries a debt burden that ties its hands.

Central Europe is industrial, but dependent on the German engine. Germany, long seen as the anchor of the eurozone, has become its biggest question mark.

Europe’s real problem, therefore, is not just found in budget tables. It lies in whether the continent can once again produce enough wealth to support its debts, social model, climate ambitions and geopolitical promises.

Europe can try to cure inflation with tariffs, debt with fiscal rules and weak growth with subsidies. But if it does not solve deindustrialization, it will only treat the symptoms of a disease it has long been unwilling to admit.

The Loss of Sovereignty

The solution to European deindustrialization does not begin with subsidies, new strategies or more Brussels shortcuts. It begins with naming the problem precisely. For too long, Europe has told itself that industrial decline is the natural price of the transition to a more modern, cleaner and more knowledge-based economy. But when a continent loses the ability to produce key goods, it does not gain a higher form of prosperity. It loses part of its freedom.

France has long experience of this phenomenon. Its deindustrialization has weakened regions outside the big cities, widened the trade deficit and increased dependence on imports. That is why the French debate is useful for the rest of the continent.

In an interview with Thinkerview, Olivier Lluansi, an expert on industry and energy, and Arnaud Montebourg, a former French minister for industrial renewal, argue that reindustrialization is not nostalgia for factory chimneys. It is a question of sovereignty, social cohesion and the state’s ability to finance its own model.

Deindustrialization is not just the loss of factories. It is the loss of the ability to make decisions. A country that no longer manufactures can still have a parliament, a government and strategic documents. In a crisis, however, it will discover that its real freedom ends where imports of antibiotics, chips, energy or munitions begin.

Three Industrial Illusions

The return of factories to European soil may sound like yet another new plan for Europe. In reality, however, the issue is not only bringing some production back, but also preserving the production that remains.

In essence, it is a European response to the same logic that Donald Trump has brought back into American politics. Strategic production, in his view, should be at home, not simply wherever it is cheapest. For such a plan to succeed, or to have even a measure of realism, Europe must abandon a number of misconceptions.

The first is that Europe has often confused decarbonization with deindustrialization. When production moves outside the continent, European statistics can look cleaner. The planet, however, does not become cleaner. Emissions merely move with the factories. The continent can therefore buy the illusion of a greener economy at the price of greater industrial dependence.

That is the uncomfortable truth of European climate policy. If the continent shuts down energy-intensive production at home and imports the same goods from countries with a dirtier energy mix, it may not reduce global emissions. It will only reduce its own industrial capacity. Climate policy that cannot sustain production can then easily become a policy of importing Europe’s own carbon footprint.

The second misconception is that the fight against deindustrialization is treated as a succession of political fashions, not as a set of real solutions. It is not a matter of subsidizing start-ups one year, electric batteries the next, then vaccines and finally data centers or military technology.

Factories are not built to the rhythm of press conferences. They need energy, capital, skilled workers, stable rules and time. That is where the weakness of the European response lies. The EU can produce subsidy plans quickly, but it is slow to create the conditions in which production actually pays.

The final misconception is that bringing factories back means bringing all production back to Europe. Reindustrialization does not mean producing everything at home. It means knowing which things the continent cannot afford to be unable to produce.

Europe does not need another abstract competitiveness plan. It needs a list of strategic manufacturing sectors, including medicines, energy technologies, defense capabilities, critical materials, chips, food inputs and industrial machinery. Such production is what would ensure that the EU can withstand crises.

The European crisis, then, is not just a crisis of growth, inflation or debt. It is a crisis of a continent that must find out once again whether it can still produce the wealth that pays for the welfare state. The winner in the new European economy will not be the country that talks best about strategic autonomy, but the one that can turn reindustrialization into real factories, jobs and technological control.

Europe cannot have the Swedish social model, Chinese industrial dependence and American geopolitical ambition at the same time.