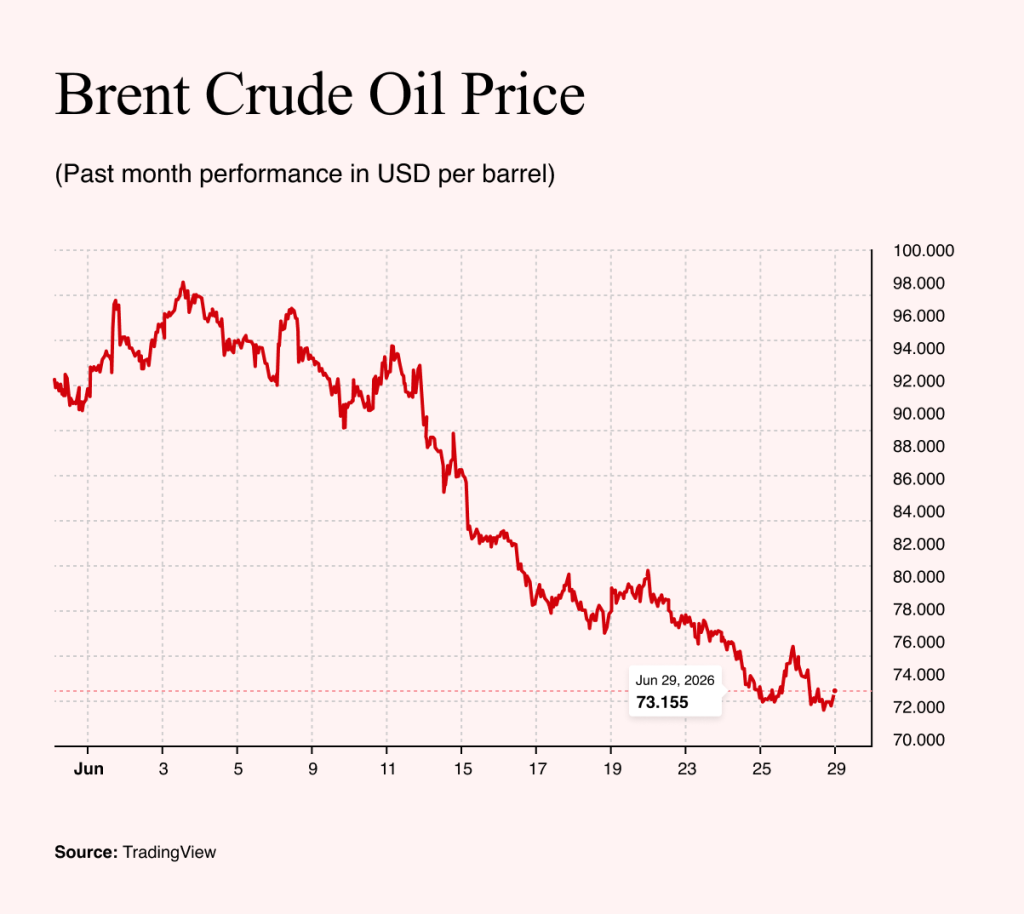

The latest turn in the Iran conflict had an uncomfortably familiar feel. Ahead of the US attack on 28 February 2026, pressure on Tehran had also been building in stages, often over the weekend, while global markets were closed.

Something similar happened this weekend. Both sides accused each other of violating the ceasefire, and explosions were again heard near the Strait of Hormuz. Shipping traffic, however, did not stop entirely and was estimated at about 40 ships a day.

The situation therefore looked tense. But as Sunday evening approached, with Asian markets about to open, tensions eased. In the end, oil prices rose only very slightly, by tenths of a percent.

This suggests that, for now, neither side wants rhetorical or military escalation to spill over into financial markets. Such a development could again force the Americans to launch a more aggressive military operation.

None of this means that the conflict cannot flare up again during the week or lead to another open confrontation. But the weekend’s events make clear that, for now, neither side wants to increase economic tensions unnecessarily. Both have an interest in stabilizing the situation. For the Iranian regime, it is crucial that Iranian oil be allowed to return to the market and that sanctions be lifted.

When Hardware Sets the Price

Micron’s strong financial results had an unexpected impact on other tech companies. The memory manufacturer’s numbers were so impressive that they reversed the gloomy mood around artificial intelligence.

That does not mean the astronomical growth in revenue and margins among memory module manufacturers is good news for everyone. Micron reported a steep increase in gross margins, from 37.7% to 84.6%.

For a moment, the commodity memory manufacturer became a cash-printing machine. Margins rose because demand for memory modules is so enormous that Micron can charge astronomical prices. And this is not just true of Micron. Other manufacturers, including SanDisk and Western Digital, report that their production capacity is virtually sold out until the end of the year.

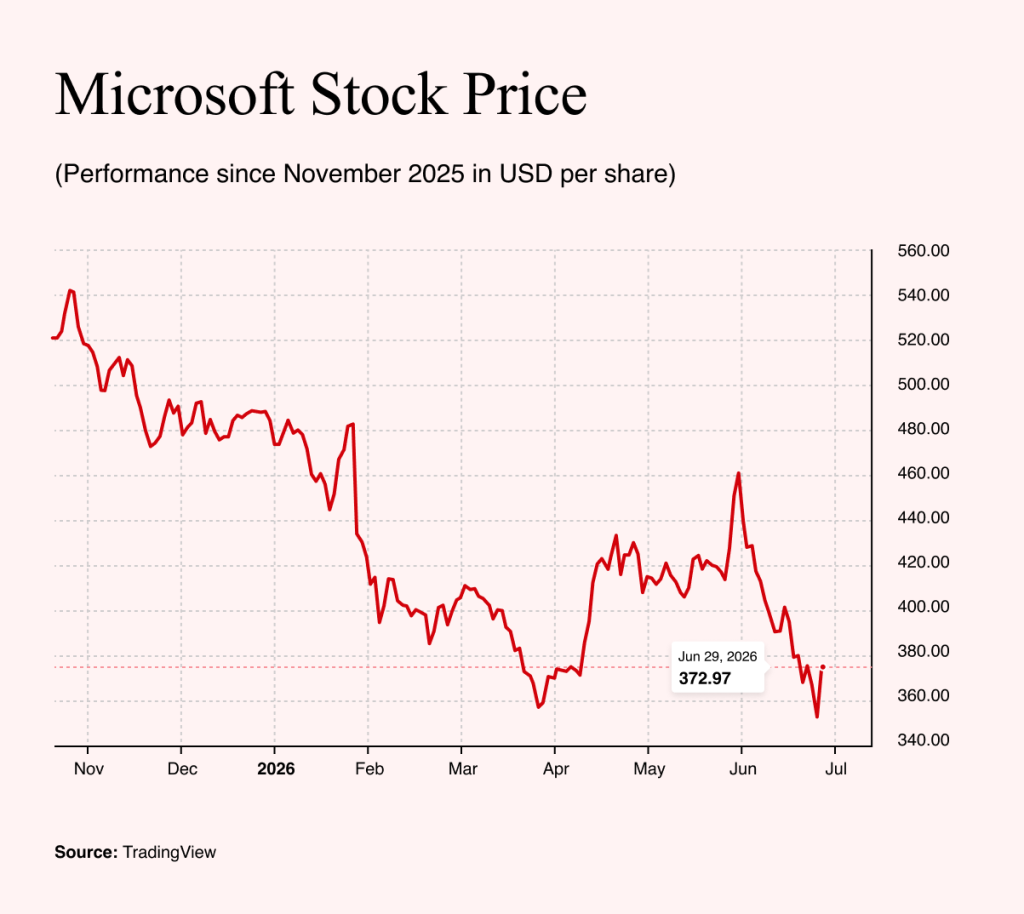

Prices for memory and other components are rising, and that will feed through into the cost of computers and other devices. Apple has raised prices on selected products by roughly 15%–25%. Microsoft has announced higher prices for Xbox consoles from 1 August 2026, with models set to cost $100–$150 more.

Investors did not welcome the move. Apple shares fell by more than 4.73% during the week. Microsoft shares dropped by 6% after the announcement, but by the end of the week, the decline had drawn investors back in. The performance of Microsoft and Apple shares has diverged since the beginning of the year. Apple’s share price is still up by about 4% since the start of the year, while Microsoft shares have lost more than 20% and are therefore relatively cheap from a fundamental perspective.

It is precisely in Microsoft shares that we can see the “Magnificent Seven” story, which drove financial market growth in 2024 and 2025, coming to an end. This year, the AI trade has definitively shifted to component manufacturers such as Micron.

However, demand for memory modules is clearly cyclical. It could drop significantly next year, once a large share of data centers is already operational. The AI sector has therefore entered its next phase.

A Warning from the Central Banks’ Headquarters

The annual report of the Bank for International Settlements (BIS) offers a more detailed analysis of artificial intelligence, especially from a macroeconomic perspective.

The institution occupies a unique place in the global financial system. Its view of artificial intelligence is particularly interesting because it moves beyond the usual debate over whether tech stocks are overvalued or undervalued. The BIS sees AI as a new macroeconomic phenomenon.

According to the BIS, the investment boom around AI was one reason the global economy weathered the combination of tariffs, geopolitical uncertainty and weaker consumer sentiment better than expected in 2025. Investment in semiconductors, data centers and energy infrastructure became one of the drivers of US growth and, through supply chains, also helped parts of Asia.

In its report, the BIS examines AI from several angles. One of the most interesting is its warning that if AI begins to replace jobs on a large scale, it will increase the economy’s productive capacity and make production more efficient, but at the same time significantly weaken the consumer base.

There is therefore a risk that income will shift too quickly from labor to capital. Companies will produce more efficiently, but the economy will lack sufficiently strong demand to absorb this new capacity. In other words, AI is technologically brilliant, but economically less useful if it cuts off the very consumers on whom it depends.

The Supercycle Sucking Up Liquidity

Another risk identified by the BIS is capital risk. Artificial intelligence is often presented as a purely digital revolution. In reality, it is increasingly an industrial and infrastructure boom.

It requires chips, memory, servers, data centers, cooling, electricity, transmission networks and construction capacity. All of this costs enormous amounts of money. The five largest hyperscalers are expected to spend more than $1tn on AI-related capital expenditures in 2025 and 2026. This is no longer garage-based innovation or a software product with minimal marginal costs. It is a new investment supercycle.

Every investment supercycle has one unpleasant characteristic: it consumes capital before it begins to generate returns. AI is therefore beginning to drain liquidity from financial markets. Money that could be flowing into other sectors, such as dividends, share buybacks, smaller companies or traditional investments, is being diverted to data centers and infrastructure.

At first, this appears to be evidence that artificial intelligence will reshape the future. Later, however, it may turn out that some of this capital was spent too soon, at too high a cost and on the basis of overly optimistic assumptions.

It is precisely here that the BIS warning takes on concrete market significance. The problem is no longer just whether artificial intelligence will eventually boost productivity, but how long companies will have to keep increasing investment before that promise begins to show up in their results.

Apple and Microsoft are no longer raising prices because they are selling customers new technological features, but because someone has to pay for the rising costs of memory and other components.

Investors understood this immediately. Hyperscalers are being forced to increase capital expenditures once again, while the market is no longer willing to forgive this insatiable appetite for investment. The BIS warning therefore did not remain an academic footnote in the annual report.

It is visible on the stock market itself: after a few weeks, Wall Street is running out of steam. As the first half of the year draws to a close, Europe suddenly does not look like the laggard, but rather like a market that, at least for the moment, can afford to keep pace.