Among classical liberal investors, there is a longstanding wariness of industries that carry an ideological label or depend on government subsidies. The reasoning is straightforward: such sectors tend to be poor vehicles for returns.

The government has an unfortunate habit of distorting the market environment. It changes the rules mid-game, and it determines winners not according to the quality of a business model, but according to who manages to have their name inserted into the right clause of a bill while it is still being drafted.

An investor, then, needs more than a grasp of the product, the margins and the company's balance sheet. They also need to read the political winds correctly, anticipating which technology will be designated as strategic next year and which will end up on the list of offenders. Green energy has long carried precisely this label.

This perception was further reinforced during the environmental, social and governance (ESG) era, when investment analysis began, in some cases, to resemble a moral judgment more than a financial one. Alongside emissions and energy efficiency, scrutiny extended to whether a company was sufficiently socially conscious, inclusive and aligned with the right values.

In effect, a vocabulary better suited to activism than to capital allocation had entered the world of hard-nosed business, a world in which capital costs, return on investment and the ability to generate cash are what typically matter.

From Moral Project to Market Necessity

The logic once seemed straightforward. Once the era of cheap money and generous subsidies ended, green energy would be exposed to market discipline for the first time. What had looked like a transformative industry would turn out to be, in large part, a utopian project, well suited to political speeches but poorly suited to shareholder returns.

Part of this thesis has held up. ESG investing is today, to put it bluntly, something of a has-been. After the euphoria of the cheap-money years, green stocks came crashing back to earth. Many solar and hydrogen names lost dozens of percentage points in value, and investors drew the obvious conclusion: climate urgency, on its own, does not make a company profitable.

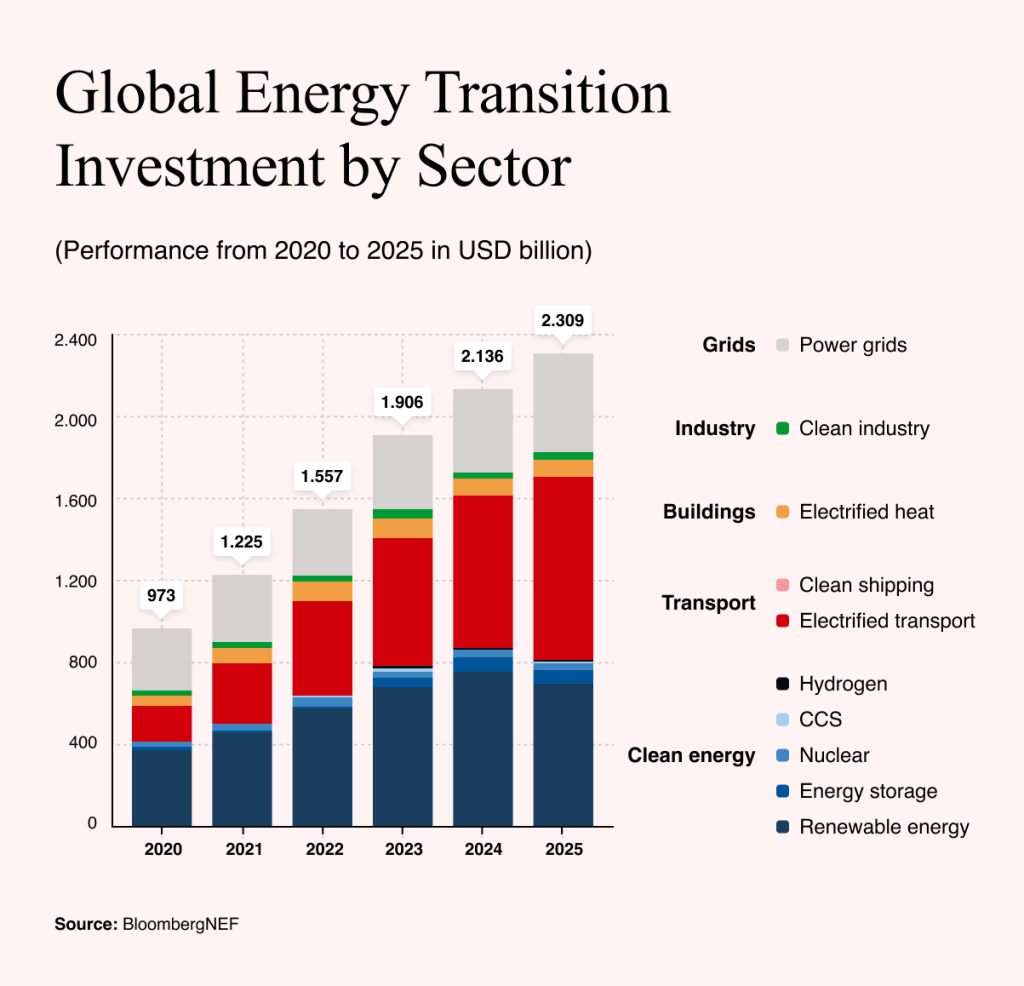

Yet this was not the end of the story, and the reason is instructive. Green energy did not disappear. Instead, it kept attracting capital at scale. According to BloombergNEF, $973bn flowed into the energy transition in 2020. By 2023, that figure had risen to $1.9tn, and by 2025, it reached a record $2.3tn.

The trend is expected to continue into 2026, and this persistence points to something more significant than a rebound in sentiment. It is not that investors have rediscovered enthusiasm for a sustainable, degrowth-oriented vision of society. Rather, the underlying investment case for green energy has changed.

The sector is evolving from a moral project into an infrastructural necessity. Clean electricity is no longer required merely to satisfy climate targets. It is required to run electric vehicles, power industry, support battery storage and grids and, increasingly, supply artificial intelligence data centers.

In other words, green energy is ceasing to be a matter of ideological virtue and becoming a matter of raw capacity. The relevant question is no longer who will save the planet. It is who can supply enough electricity to a world whose demand for it keeps rising.

Anatomy of an Investment Debacle

This turning point is clearly visible in the performance of the specialized iShares Global Clean Energy ETF, for which 2024 and 2025 serve as a useful case study in contrasts.

In 2024, the fund posted a disastrous performance, losing more than 25%, while the S&P 500 gained roughly 25% over the same period. The gap is the more telling figure. An investor who chose clean energy over the leading US index in 2024 did not merely lose money in absolute terms. Relative to an investor in the S&P 500, they underperformed by roughly 50 percentage points, a gap wide enough to move this beyond the category of ordinary sectoral weakness and into that of an investment debacle.

Several factors were behind this. The most fundamental was interest rates. Although rates were no longer rising sharply in 2024, they remained painfully high, and markets were gradually forced to abandon the assumption that central banks would soon restore an era of cheap money. For solar and wind developers, this was structurally damaging news.

The reason lies in the underlying business model, which depends on massive upfront investment, long payback periods and inexpensive financing. Once the cost of capital rises, that model starts to unravel from the inside. A project that looked, in a presentation, like the green power plant of the future can turn out, once run through a cost spreadsheet, to offer a dismal return on investment.

The second factor was a broader sobering up after the subsidy boom. Rising capital costs put pressure not only on companies but also on the governments backing them. Facing emptier coffers, many governments began cutting subsidies, reassessing them or signaling that existing support schemes would not last indefinitely.

This uncertainty exposed an underlying weakness in the investment case: a significant share of green projects had been attractive not because of an exceptionally strong business model, but because they were underwritten by public support. Once that support came into question, the appeal of the sector faded quickly.

Sector-specific problems compounded the effect. In solar, Chinese overproduction was the dominant factor. Cheap Chinese panels accelerated decarbonization and lowered technology costs globally, but they also placed severe pressure on margins for Western manufacturers, many of which could not match the scale, pricing or industrial capacity of Chinese production. Wind faced a different but related set of pressures: more expensive financing, higher material costs, project delays and, in the case of offshore wind, contracts structured during the cheap-money era that no longer reflected current economics.

A further, less structural factor amplified the decline: a shift in investor attention. Capital that tends to follow momentum moved out of green energy and into artificial intelligence. The logic was simple. Why commit to a solar farm with a decade-long payback period when Nvidia, Microsoft, Meta, Amazon or Broadcom offered more immediate upside?

As a result, 2024 was not simply a weak year for green stocks. It was the year in which artificial intelligence absorbed the market's attention, its capital and, perhaps most consequentially, investors' patience for slow-moving infrastructure narratives.

AI Runs on Electricity, Not Ideology

It was ultimately artificial intelligence that reshuffled the deck. In 2025, the iShares Global Clean Energy ETF rose by more than 46%, outperforming even the S&P 500, which had a positive year of its own but posted a more modest gain of around 17%. The reversal from the previous year is the point worth dwelling on, since it reflects a change in the underlying investment logic rather than a simple rebound.

The mechanism is straightforward. As AI infrastructure has scaled up, it has become clear that data centers require enormous, continuous amounts of electricity. Because they run 24 hours a day, intermittent generation from solar and wind alone cannot meet the load.

Meeting that demand requires battery storage, stronger power grids and a stable, zero-emission source able to supply power when neither the wind nor the sun cooperates. This is the specific gap that has returned nuclear power to serious consideration, and it explains why stocks tied to nuclear energy, batteries and broader electrification infrastructure have driven the rebound in green investment.

In my view, this is also where the more durable investment opportunity lies over the coming years. It is not in every company that presents itself as green, but specifically in those building the physical backbone of the new energy system: transmission grids, transformers, cables, battery storage, demand response and stable baseload power.

The underlying logic is that AI, despite appearing to be an intangible revolution, runs into a distinctly physical constraint: it requires electricity, transmission capacity and grid connections. This is why companies such as ABB, Schneider Electric, Siemens Energy, Eaton and Prysmian, all active in electrification, grid automation, high-voltage infrastructure and consumption management, are attracting renewed investor interest.

A similar logic applies to battery storage providers such as Fluence Energy and to companies tied to nuclear fuel or stable, zero-emission generation, such as Cameco. Taken together, these shifts suggest that the green narrative is moving from ideology to business, under a simpler mandate: less moralizing, more megawatts, cables and substations.