The escalating standoff in the Strait of Hormuz is pushing oil prices higher, while the artificial intelligence boom is diverting investment away from traditional IT spending. Markets have once again become highly volatile, with IBM emerging as one of the first casualties of the shifting investment landscape.

Tensions in the Strait of Hormuz have intensified sharply. After US President Donald Trump suggested that Washington should charge a 20% fee for protecting commercial shipping, oil prices were almost certain to rise.

Iranian Foreign Minister Abbas Arakchi responded with a touch of irony. He agreed that the Strait of Hormuz needed a guardian, but argued that the role belonged not to the United States, but to Iran, which regards itself as the true protector of the strategically important waterway.

Arakchi also joked that a 20% fee was excessive, adding that Iran would supposedly offer a fairer price.

Shipping Grinds to a Halt

The crisis has continued to escalate. The United States has launched several attacks on targets linked to the Strait of Hormuz, while Iran has retaliated with missile strikes against US bases in the region.

More importantly for global markets, however, shipping through the strait has once again slowed to a crawl. The reason is straightforward: under current conditions, ships and oil tankers cannot obtain insurance. Without insurance, few operators are willing to risk the journey.

The figures illustrate the scale of the slowdown. According to shipping analytics firm Kpler, only 19 commercial vessels passed through the Strait of Hormuz last weekend – less than half the number recorded the previous weekend.

The data for 15 July was even more striking. Public Automatic Identification System (AIS) trackers recorded just five transits: three vessels entering the Persian Gulf and two leaving it. These were not necessarily all large oil tankers, however, as AIS tracks every vessel transmitting a signal. Some ships may also switch off their transponders or limit their use.

The broader trend is nevertheless unmistakable. Traffic through the Strait of Hormuz has once again fallen to exceptionally low levels. Until insurers return to the market and shipping companies regain at least a basic sense of security, traffic is unlikely to recover. All of this is unfolding as global strategic oil reserves continue to decline.

The Return of Extreme Volatility

Technology stocks have also been hit by renewed volatility. One example is South Korean memory chip maker SK Hynix, whose American depositary receipts (ADRs) began trading on Nasdaq last Friday. During a single trading session, the stock can gain 10%, only to lose a similar amount the following day.

Such swings bear little relation to companies' underlying value or to macroeconomic or corporate developments. Instead, they increasingly reflect speculative trading.

The moves are reminiscent of the 2021 meme-stock frenzy that sent shares of companies such as GameStop and AMC soaring. This time, however, the companies involved are established technology firms with solid profits and resilient business models. Even so, they have not escaped the turbulence. During Wednesday's trading session, Dell fell by more than 10%, while Western Digital lost 9%.

The sharp swings in technology stocks were accompanied by a decline in gold prices. As has often been the case in recent months, worsening security tensions in the Middle East have paradoxically pushed the precious metal lower.

The reason is straightforward. Investors increasingly fear that central banks – particularly those in countries with weaker currencies – may be forced to sell part of their gold reserves to stabilize their exchange rates. At the same time, yields on US Treasury bonds rose, pushing bond prices lower. In effect, apart from cash, traditional safe-haven assets offered little refuge.

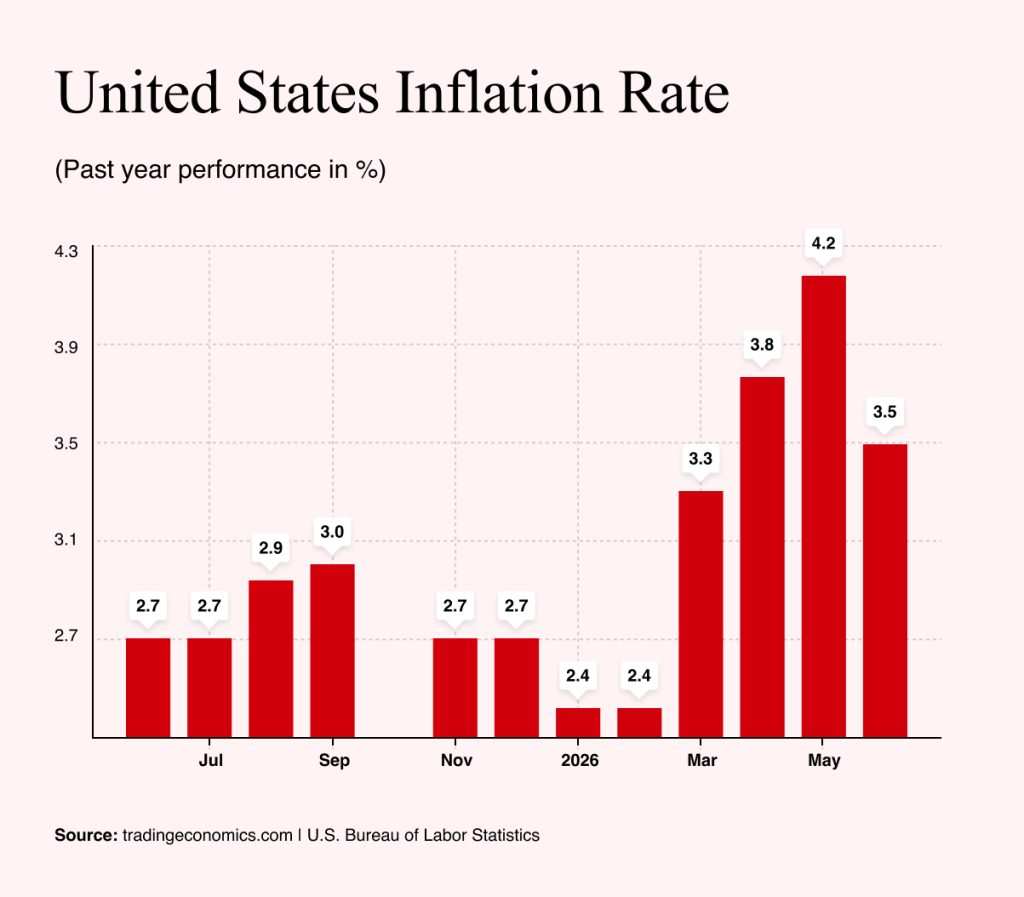

The only respite came with the release of US inflation data. Annual inflation slowed from 4.2% in May to 3.5% in June, giving markets some breathing space. Although the likelihood of an interest rate increase in September has declined, it remains above 50%.

The figures also highlighted how vulnerable inflation remains to higher energy prices. Should oil rise above $100 a barrel again, June's improvement could prove only temporary.

The AI Boom Begins to Reshape Technology Spending

Memory chip manufacturers were not the only companies attracting investors' attention this week. IBM also found itself in the spotlight after releasing preliminary quarterly results.

Companies rarely publish preliminary figures ahead of schedule unless they are preparing investors for disappointing news, and IBM proved no exception.

The company expects second-quarter revenue of $17.2bn, below analysts' expectations of $17.9bn. Adjusted earnings are forecast at $2.93 a share, compared with consensus estimates of $3.01.

The shortfall itself was relatively modest and, on its own, did not justify the stock's 25% decline in a single trading session. What unsettled investors was management's explanation.

Chief executive Arvind Krishna said customers had abruptly shifted spending priorities toward the end of the quarter. Rather than investing in IBM's traditional infrastructure and services, many accelerated purchases of servers, data storage and memory chips in anticipation of higher component prices.

In other words, the AI investment boom is beginning to divert spending away from other areas of corporate technology budgets. Companies are prioritizing chips and computing capacity, leaving less money available for software, consulting and traditional IT infrastructure.

IBM also acknowledged that it had underestimated the speed of this shift. The company was unable to adapt quickly enough, causing several major contracts to slip into future quarters.

That sent a far more troubling signal than the earnings miss itself. Investors began asking a much more fundamental question: Is AI really a growth engine for IBM, or could it instead begin eroding the company's traditional business?

IBM has long argued that artificial intelligence will drive demand for its software, hybrid cloud platform and consulting services. For now, however, the first phase of the AI investment cycle appears to be benefiting manufacturers of chips, memory chips and servers. The rest of the technology sector will have to wait until companies begin deploying the infrastructure they are now building.

That helps explain the severity of the sell-off. Investors were not simply reacting to a weak quarter – they were questioning IBM's entire AI strategy. In the space of a single day, a company widely seen as a stable beneficiary of the AI boom suddenly came to be viewed as one of its first casualties.

That outcome is far from inevitable. Much will depend on whether IBM can successfully shift its consulting business away from traditional enterprise IT and toward AI implementation.

The company's history offers grounds for cautious optimism. IBM has successfully navigated several technological revolutions before, reinventing itself from punch-card machines to electronic computers, then to personal computers and, later, to software and IT services.

The recent sell-off has also pushed IBM's dividend yield above 3% – an attractive level for a US technology stock. More importantly, management has given no indication that the dividend is under review.

The company currently spends about $6bn a year on dividend payments while generating roughly $13bn in free cash flow over the past 12 months. For now, the payout appears well supported.

That could make the stock more attractive to conservative investors seeking exposure to the technology sector without paying the lofty valuations commanded by many AI leaders.

Following the recent decline, IBM is trading at roughly 18 times expected earnings. While that is not yet a bargain, the shares are considerably cheaper than they have been in recent years.

IBM has survived several waves of technological disruption. It must now prove that artificial intelligence will not be the first one it fails to master.