For decades, oil markets have feared one scenario above all: war in the Persian Gulf. Since Saturday, when Israel and the United States attacked Iran, that threat has become reality.

The consequences for the oil and gas markets will be complex. The issue is not only the potential loss of Iranian production, which contributes more than three million barrels of oil per day to global supply. More important is that the Iranian leadership has chosen an asymmetrical style of warfare. One of its objectives is to create as much disruption as possible with limited resources, and energy infrastructure is among its principal targets.

During Iran’s response – which was directed at several countries in the region – key energy facilities were struck or forced to restrict operations. The Ras Tanura refinery on the eastern coast of Saudi Arabia, owned by the state giant Saudi Aramco, was temporarily shut down after being hit by an Iranian drone.

Another Iranian drone attack targeted the world’s largest liquefied natural gas export terminal in Qatar. Qatar’s state energy company, QatarEnergy, subsequently suspended production.

Production at the Khor Mor gas field in Iraq has also been halted. In addition, tanker traffic through the Strait of Hormuz – through which roughly one fifth of the world’s oil consumption normally passes each day – has almost come to a standstill.

At first glance, such reports may suggest that the world is facing a historic oil shock. The reality is more nuanced. Oil prices are rising, which is hardly surprising under the circumstances. For Europe, however, the price of natural gas poses a potentially greater risk.

The negative news can therefore be placed in perspective. The situation is serious, but not necessarily as catastrophic as it might initially appear.

The bottleneck of global energy

As for the Strait of Hormuz, Tehran does not have to impose a formal blockade or mine the waterway to disrupt shipping. Traffic has already slowed dramatically because tankers must be insured before entering the area. Insurance costs are directly linked to the value of the vessel, which typically reaches about $100 million.

Insurance companies, led by the British market Lloyd’s, only need to raise their premiums, and the transport of oil quickly becomes uneconomical. The logic is simple.

President Donald Trump has sought to circumvent this obstacle by instructing his administration to explore ways of providing state-backed insurance guarantees for tankers. That would help stabilise the market, but it would not eliminate the underlying safety risks, which remain extremely high.

The United States also wants its navy to escort commercial tankers. Although naval escorts have proved effective against piracy or isolated drone attacks, the situation here is more complicated. US warships would need to be confident that they can approach the Iranian coast without unacceptable risk. In practical terms, that would only become possible after the fall of the current regime.

There is, however, a strategic alternative. Saudi Arabia operates an east–west oil pipeline known as Petroline, which connects the oil fields of the Persian Gulf with the port of Yanbu on the Red Sea.

The pipeline allows shipments to bypass the Strait of Hormuz altogether. Transport by land is more expensive because of transit fees and additional logistics. Even so, the route represents an important safeguard against supply disruptions and helps limit the geopolitical premium in oil prices. Between five and seven million barrels of oil per day could be transported this way, significantly reducing the overall impact on global markets.

Most of the oil passing through the strait is destined for Asia. Around 38 per cent goes to China, 15 per cent to India, 12 per cent to South Korea and 11 per cent to Japan.

That creates a serious challenge for those countries, although the full effects will probably only become visible after several weeks. The key question is where they will obtain alternative supplies and whether suitable new suppliers can be found.

Only if those efforts fail would Asian buyers have to begin purchasing large volumes directly on the open market, which could trigger sharp price increases. There has also been speculation that Iran is allowing Chinese vessels to pass through the strait. Such claims cannot be verified. In any case, any arrangement of that kind would almost certainly remain unofficial, as an open military and economic alliance between China and Iran does not currently exist.

Real prices and speculative capital

When analysing oil markets, it is important to distinguish between physical consumption and financial trading. While roughly 102 million barrels of oil are consumed worldwide each day, the daily volume of financial transactions amounts to between two and three billion barrels.

This discrepancy largely reflects hedging activity between major producers and consumers seeking to protect themselves against price risks.

A second factor is purely speculative investment. Together, those two forces are currently pushing oil prices higher.

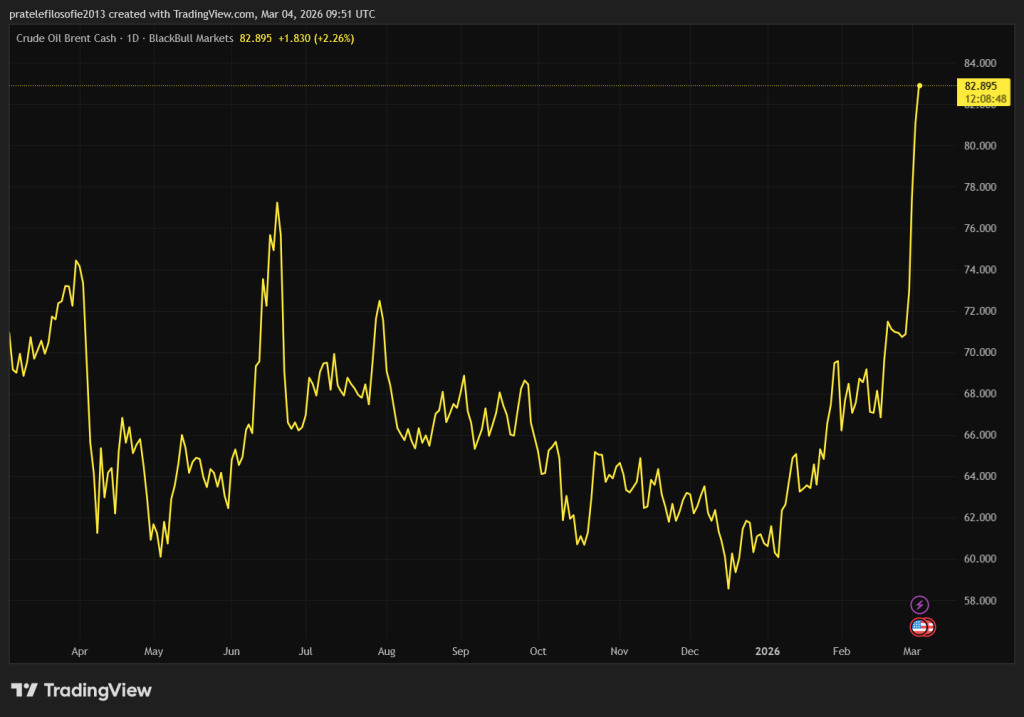

Looking at the development of North Sea Brent crude, the price has risen from about $70 per barrel before the attack on Iran to roughly $82 afterwards – an increase of around 19 per cent.

Such a reaction is hardly surprising. Brent prices had already been climbing since the beginning of the year as investors anticipated a deterioration in the global security environment. The rise accelerated once speculation about a direct attack on Iran began to circulate. In that sense, financial markets were already partly prepared for the conflict.

How high could prices rise? In the immediate aftermath of the attack, some commentators quickly predicted oil prices of $100 or even $150 per barrel. Such dramatic scenarios tend to attract attention, but reality is usually less extreme.

Current prices already reflect market expectations about the likely duration of the military operation, which many analysts estimate at around four weeks. If the conflict were to last significantly longer, another sharp price increase could follow, with potentially serious consequences for the global economy.

The initial price surge was therefore predictable. After the first jump, further increases are likely to occur more gradually even if the conflict escalates. The key issue is when prices might cross a threshold that becomes genuinely damaging for the real economy.

Two parameters are particularly important: the duration of the conflict – currently estimated at roughly one month – and the price level to which oil might gradually climb. Brent last reached its recent peak in the summer of 2022, after Russia’s invasion of Ukraine, when it traded at about $122 per barrel. Current prices remain well below that level.

Even then, however, prices did not remain elevated for long. The explanation lies in basic market mechanics. At sufficiently high prices it becomes profitable to produce oil almost everywhere, including in Venezuela, prompting producers to expand output.

Another factor is the weakening of the US dollar against the euro. Even if oil prices rise in dollar terms, the real impact on European economies may therefore be somewhat less severe.

The new structural reality of the markets

The price level at which oil would become the dominant macroeconomic problem of the conflict is probably somewhere around $150 per barrel. The good news is that current prices remain well below that threshold. The less reassuring news is that there is still considerable room for further increases.

Another important structural change should also be considered. Financial markets today react less strongly to fluctuations in energy prices than they did in the past. 20 or 30 years ago, a similar jump in oil prices would probably have caused far greater nervousness and sharp sell-offs on global stock exchanges.

The explanation is structural. In the main US equity benchmark, the S&P 500, the energy sector now accounts for only about 3.5 to 4 per cent of the index, while technology companies represent more than one third. The price of oil therefore has only a limited direct impact on the dominant technology sector.

The situation would change, however, if oil prices were to rise far above the critical threshold and begin to push global inflation sharply higher. In that scenario, central banks would most likely respond by tightening monetary policy again.

The structure of the US stock market therefore illustrates how profoundly the global economy has changed over recent decades. Oil remains a crucial commodity, but it is no longer the most important one.

Paradoxically, financial markets today would probably react more violently to a large-scale attack on copper mines or sources of rare metals – raw materials that are central to the digital and energy transition in much the same way that oil once was to the industrial age.