Despite the resilience shown by stock markets, particularly in the US, they have now slipped into a period of adjustment. By definition, a correction refers to a decline of between 10 and 20 per cent from a recent peak. It took five weeks for markets to reach that threshold.

The tech-heavy Nasdaq has therefore officially moved into correction territory. Despite efforts by Donald Trump to sustain expectations of an eventual success, markets have recorded five consecutive weeks of declines. The last comparable stretch for the S&P 500 occurred in May 2022.

Even so, negative sentiment remains relatively contained given the geopolitical risks and uncertainty. Markets are still far from entering bear territory, typically defined as a fall of more than 20 per cent.

Tech giants under pressure from lawsuits

US equities have nevertheless suffered an additional setback after a Los Angeles jury ordered Meta and Google to pay a combined 6 million dollars in damages to a young woman who said she became addicted to Instagram and YouTube as a minor.

The court concluded that responsibility does not lie solely with individual users, but also with engineers and behavioural experts who designed algorithms to maximise engagement. It is widely known that such companies draw on insights from modern psychology to increase the time users spend on their platforms.

The case may mark the beginning of a broader shift. Some commentators compare the situation to litigation against tobacco companies, when legal responsibility for addiction gradually moved towards manufacturers – a turning point that contributed to the sector’s long-term decline.

For shareholders, however, the parallel offers some reassurance. Tobacco companies continue to generate substantial profits decades after the first lawsuits, despite declining consumption among younger generations. A similar trajectory for technology firms cannot be ruled out.

[

The six-million-dollar penalty itself is negligible for companies of that scale. The greater risk lies in the volume of similar cases. Given the importance of precedent in US law, both the number of successful claims and the level of damages could increase.

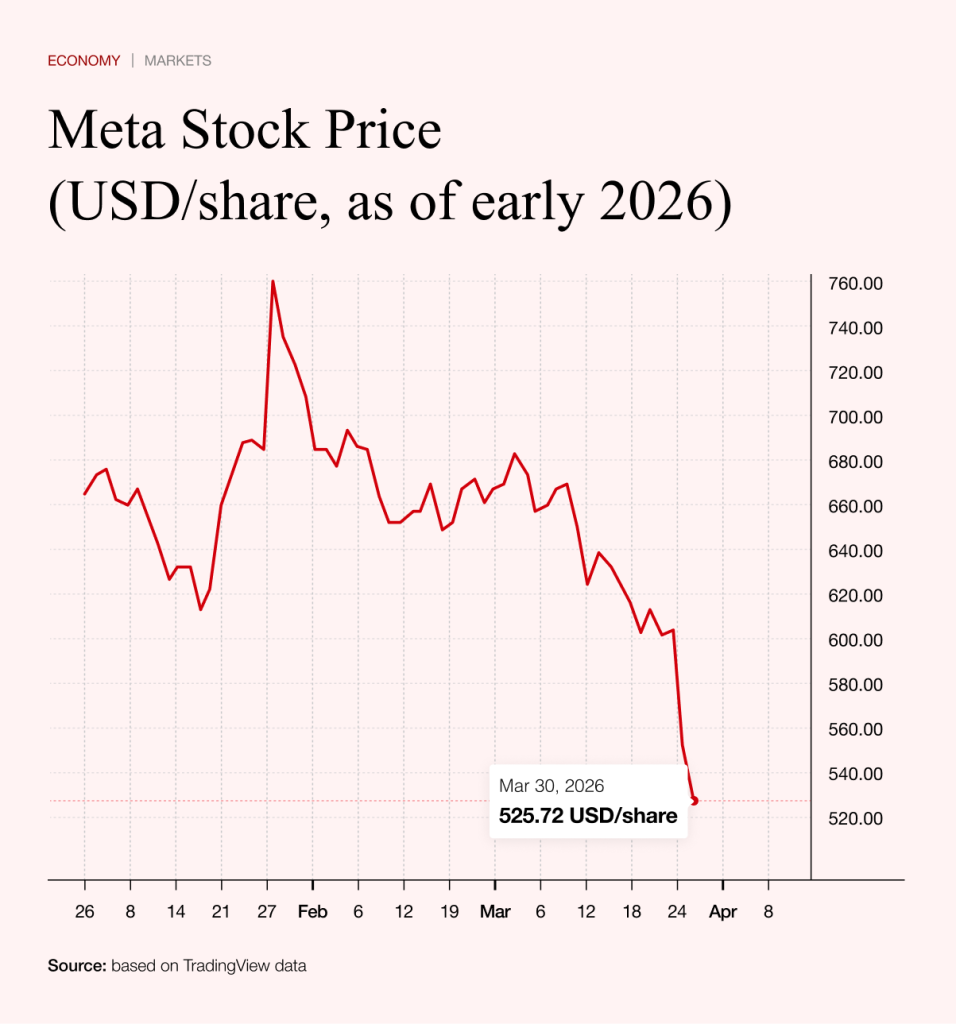

Over time, Meta and Google may be forced to adjust their algorithms and increase transparency. Since the ruling became public, Meta’s share price has fallen by more than 11 per cent. Alphabet has proved more resilient, declining by just over three per cent.

Meta’s vulnerability stems from the nature of its core business, which is centred on advertising. Advertisers pay for precisely targeted exposure, enabled by algorithms designed to hold users’ attention as effectively as possible.

The company has been among the main beneficiaries of advances in artificial intelligence, which have improved content targeting and boosted advertising revenues. That model is now under scrutiny.

Any adjustment is likely to be gradual rather than abrupt. As in the case of tobacco, structural decline may unfold slowly and only become visible in hard data over time. For that reason, some investors view the recent fall in Meta’s share price as a buying opportunity, particularly given that advertising revenues are expected to remain strong this year.

The importance of the Magnificent Seven

For the broader market, however, the timing of the ruling is unfavourable. The Trump administration is seeking to contain the negative impact of high oil prices on investor sentiment.

US indices, however, remain heavily dependent on the performance of the so-called Magnificent Seven. Notably, Apple has so far shown relative resilience, followed closely by Nvidia.

This is somewhat paradoxical. Apple is often criticised for lagging behind in artificial intelligence, having invested less aggressively in the sector than many of its peers.

By contrast, Microsoft, widely seen as a leading beneficiary of the AI boom due to its extensive investments and client base, has struggled this year. From its annual peak, the stock has fallen by more than 30 per cent, underscoring the absence of guaranteed winners in the market.

The oil shock and the risk of a debt crisis

Recent weeks have also highlighted the growing importance of the bond market, which is sending a more cautious signal than equities. Rising yields are steadily increasing pressure on policymakers.

Compared with previous oil shocks, there is at least one mitigating factor: Western economies are less dependent on oil than in past decades. Alternative energy sources, while not a full substitute, may soften the impact.

Paradoxically, the decline of heavy industry also reduces exposure to energy shocks. The greater concern, however, lies elsewhere. The current oil shock is unfolding at a time of elevated public and private debt.

Governments have limited scope for broad support measures without risking a sovereign debt crisis. Households, already burdened by debt, are likely to respond to higher fuel costs by cutting consumption more sharply.

In that sense, the oil shock could act as a trigger for the debt dynamics long anticipated by investors such as Ray Dalio.

These concerns are increasingly reflected in bond markets. Europe appears more vulnerable than the US, as illustrated by developments in France, where ten-year government bond yields have risen to 3.88 per cent.

The central risk, therefore, is not the equity correction itself, but the convergence of war, high oil prices and debt – a toxic mix that may no longer be contained by reassurance from the White House.