When we speak of “balkanization”, we tend to imagine a patchwork of ever smaller political units, shaped by historical grievances, cultural divisions, religious identities and national minorities. From a macroeconomic perspective, however, the region can be read through a much simpler lens: monetary policy. Today’s monetary regimes reveal how much stability Balkan economies have secured and at what cost.

Three Faces of Monetary Policy

The region can broadly be divided into three monetary zones. The first consists of countries firmly anchored in the eurozone: Slovenia, Croatia and now Bulgaria. The second includes economies that use the euro or are closely tied to it without being full members of the monetary union: Kosovo, Montenegro and Bosnia and Herzegovina. The third group comprises countries with their own currencies and central banks: Romania, Serbia, Albania and North Macedonia.

This division is not merely technical. It reflects differing levels of trust, vulnerability and responsibility. Eurozone members benefit from stability, lower exchange-rate risk and easier access to capital. In return, they relinquish the ability to respond to domestic shocks through independent monetary policy. Decisions are made in Frankfurt, not in Ljubljana, Zagreb or Sofia.

What is striking is that each of these countries is writing a distinct economic story. Slovenia remains the most advanced economy in the region, but increasingly resembles parts of Western Europe: stable, yet lacking dynamism. It has strong institutions, industry and credibility, but less of the growth momentum seen in poorer Balkan economies.

For Croatia, the euro has brought stability and closer integration with the European core. At the same time, it has reinforced reliance on tourism, consumption and services. This model performs well in favorable conditions, but is vulnerable to higher energy costs, weaker European demand and geopolitical tensions. The euro strengthens credibility, but does not address structural imbalances.

Bulgaria represents perhaps the most open-ended case. Euro adoption offers two possible paths. One leads to convergence, with cheaper capital, stronger investor confidence and faster economic catch-up. The other risks encouraging easier borrowing without meaningful modernization. The euro is therefore both an opportunity and a test of economic discipline.

Whether cheaper capital translates into infrastructure investment, productivity gains and modernization will determine the outcome. If it is absorbed by corruption or short-term public spending, it will merely mask existing weaknesses.

Imported Stability and Limited Sovereignty

Kosovo and Montenegro have unilaterally adopted the euro, while Bosnia and Herzegovina operates a currency board pegged to it. The benefits are predictability and protection against monetary instability. The trade-off is limited monetary autonomy and the absence of full European Central Bank support.

In the Balkan context, this can be seen as a pragmatic choice. A firm link to the euro reduces the risk of devaluation, inflationary spirals and loss of confidence. These countries have exchanged a degree of sovereignty for stability, not as a path to rapid growth, but as insurance against policy mistakes.

The Cost of Autonomy: Romania’s Stagflation Risk

The third group is perhaps the most revealing. Countries with their own currencies have greater policy flexibility. They can set interest rates, manage liquidity and allow exchange rates to absorb shocks.

Yet this flexibility comes with immediate market discipline. If fiscal policy lacks credibility, the consequences are quickly reflected in bond yields, exchange rates and borrowing costs.

This group includes Albania, North Macedonia, Serbia and Romania. Each faces distinct challenges. Albania benefits from strong tourism, a firmer currency and relatively low inflation. North Macedonia remains highly exposed to the European economic cycle. Serbia has improved investor confidence in recent years and in 2024 received its first BBB investment grade rating from S&P, a notable milestone for the region’s largest economy.

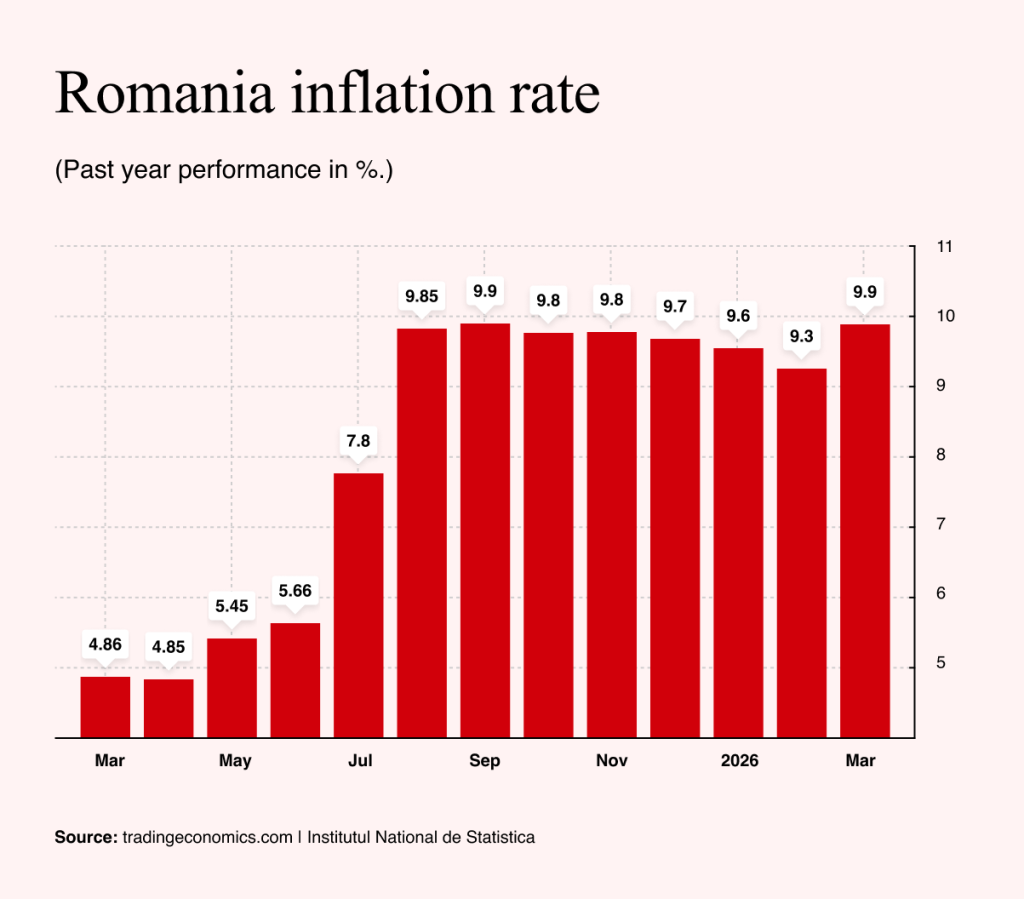

Romania, however, presents a different picture. It illustrates how macroeconomic instability can become a broader political risk. At a time when global discussions increasingly focus on stagflation, Romania offers a near textbook example.

Stagflation describes a situation in which economic growth stagnates or contracts while inflation remains elevated. For central banks, it is a particularly difficult scenario. Lowering interest rates risks fueling inflation, while maintaining high rates suppresses already weak growth.

Romania’s macroeconomic indicators reflect this tension. Inflation stands at 9.9%, driven in part by the removal of electricity price caps, higher VAT and increased consumption taxes.

Fiscal pressures are also mounting. The budget deficit has reached 7.9% of gross domestic product (GDP), making tax increases difficult to avoid. At the same time, higher taxation is weighing on growth. The economy contracted by 1.8% in the final quarter of 2025, while interest rates remain elevated at 6.5%.

Romania’s relatively low debt level compared with Western economies provides some room for maneuver. However, the trajectory is concerning. Public debt is rising rapidly, from 54.8% of GDP in 2024 to 59.3% in 2025. The narrative of economic convergence is increasingly giving way to one of fiscal adjustment.

A Region Defined by Trade-Offs

The Balkans may remain politically complex, but economically the region can be understood through the interplay of currency regimes, debt dynamics and the cost of capital.

Romania’s situation highlights a broader risk: not fragmentation, but the convergence of weak growth, persistent inflation and fiscal pressure into a single, destabilizing dynamic.

As global concerns about stagflation return, Romania is already approaching that threshold. The key question is whether it can avoid the trap or become a warning for others.