The summit left markets uneasy on several fronts. Investors were looking for signs that Washington and Beijing could ease pressure on trade, technology and energy security. Instead, they were left with few concrete results, continued uncertainty over the Strait of Hormuz and bond markets increasingly convinced that inflationary stress will last longer than hoped.

Many still argue this is a temporary effect that will fade once tensions with Iran ease. Inflation, in this view, remains transitory.

Investors, however, remember that term all too well. During the last inflation surge, Federal Reserve Chair Jerome Powell repeatedly described price growth as transitory before ultimately reversing course and raising interest rates aggressively.

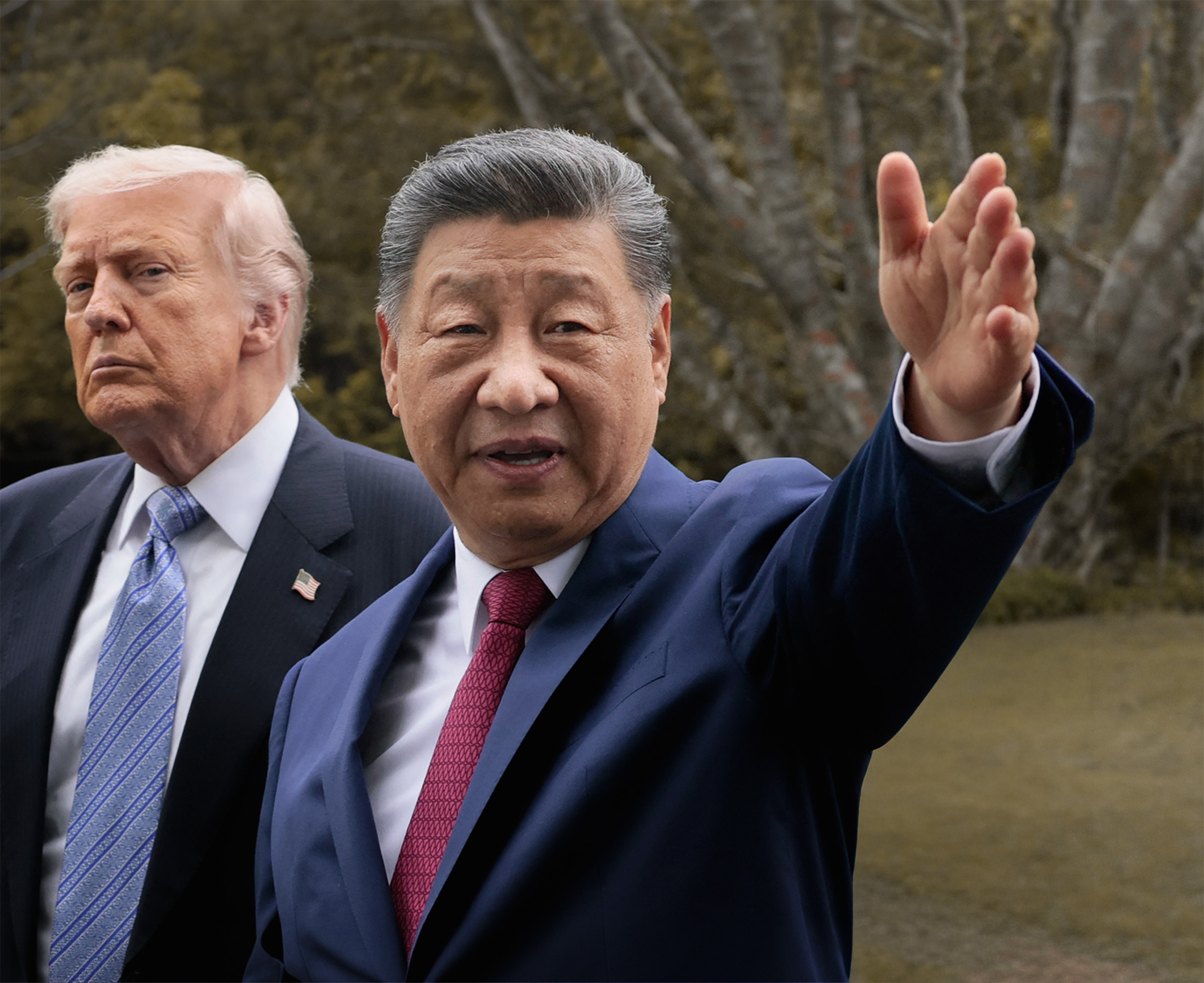

Hopes of easing inflation were briefly supported by meetings between President Donald Trump and his Chinese counterpart. Markets initially welcomed the composition of the US delegation, which suggested trade agreements would dominate the agenda.

Expectations were high. The delegation included key figures, and investors anticipated tangible progress.

But the outcome fell short. Despite Trump’s optimistic tone, markets reacted with disappointment. The only clear positive was the agreement to continue talks, with a follow-up meeting planned at the White House in September.

The willingness to engage still matters. Only a year ago, Trump portrayed China as exploiting the US economy, a message that resonated politically, and it is still the case that a concrete and strong trade agreement would be a great boost for the markets.

Unmet Expectations and Geopolitical Constraints

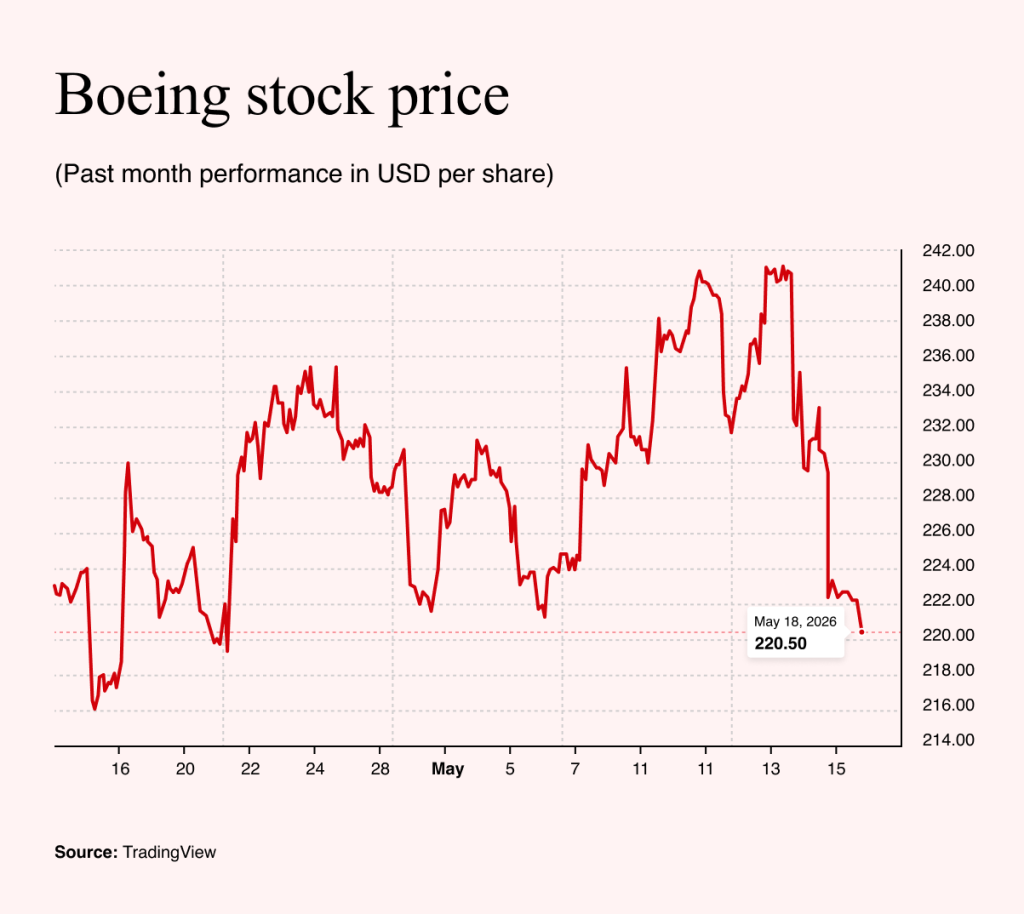

Investor disappointment was driven by the lack of concrete outcomes. Expectations had been elevated further by reports that Trump had personally invested in shares of Boeing and Nvidia.

The presence of both companies’ executives raised hopes of major deals in China. Instead, Boeing secured an order for just 200 aircraft, well below expectations of up to 500.

Nvidia faced a deeper challenge. Its H20 chips were designed as a compromise between US export restrictions and Chinese demand for artificial intelligence computing power. That compromise is now eroding.

Washington has tightened and then partially relaxed restrictions, while Beijing is actively promoting domestic alternatives. For investors, this underscores a key shift: China is no longer a conventional export market for Nvidia, but a geopolitical arena.

The biggest disappointment, however, came from the absence of progress on the Strait of Hormuz. Many analysts viewed this issue as central, even if it was not formally expected to dominate the agenda.

Investors were left with only vague statements about the importance of reopening the route. There were no concrete steps towards a solution, while Trump’s renewed hardline rhetoric toward Iran over the weekend reinforced the view that tensions will persist.

China, for its part, appears reluctant to take a more active role. As in previous crises, Beijing is observing developments rather than intervening directly. This stance has contributed to continued upward pressure on oil prices.

Bond Markets Sound the Alarm

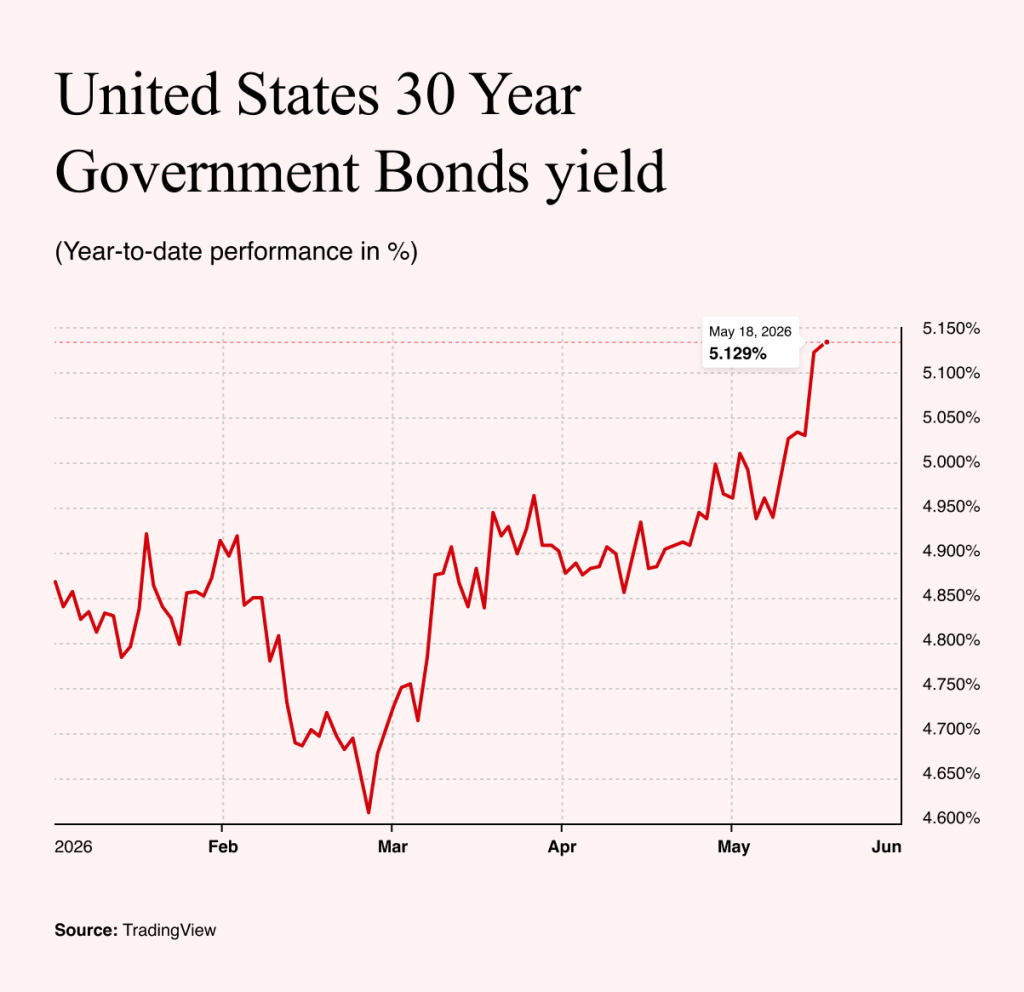

The late-week sell-off was ultimately driven by the bond market. Investors began to price in a prolonged disruption to oil flows, with no near-term reopening of the Strait of Hormuz.

This points to a drawn-out geopolitical standoff. Time, however, is a constraint for the United States, as inflationary pressures continue to build. Bond yields are already reflecting this. The 30-year US Treasury yield reached 5.12% by the end of the week, its highest level since 2007.

Such levels are difficult to sustain. Unlike in 2008, the US now faces significantly weaker public finances, limiting its ability to respond to future shocks.

Markets are also signaling that inflation expectations remain elevated. Bond yields are effectively tightening financial conditions without waiting for action from the Federal Reserve or its expected new leadership under Kevin Warsh.

The question is no longer how many rate cuts will occur this year, but whether rates might need to rise again. This runs counter to Trump’s expectations of looser monetary policy ahead of elections.

Pressure is not limited to the US. Japan’s bond market is also under strain. The yield on 30-year Japanese government bonds has climbed to 4.2%, approaching US levels.

This is significant given Japan’s still very low short-term interest rates. The steepening of the yield curve is therefore a sensitive signal for global markets.

The memory of 2024 remains fresh. A sharp appreciation of the yen triggered a carry trade unwind, as investors who had borrowed cheaply in yen were forced to close positions.

The result was a sell-off in Japanese equities and broader market volatility. Japan’s challenge is not convergence with US rates, but the potential end of an era. For decades, global risk-taking has been supported by cheap Japanese financing.

If that model is breaking down, the consequences will extend far beyond Japan. It would represent a broader reckoning for years of abundant liquidity.