Financial markets have recently acquired a new variable beyond Donald Trump’s social media account: the bond market. Unlike equities, bonds do not offer dramatic stories or spectacular rallies. Yet they serve as a rational brake whenever markets begin ignoring economic reality.

For experienced investors, US Treasury yields have become an almost infallible signal for Trump’s geopolitical pivots and the so-called “TACO trade” – Trump Always Chickens Out.

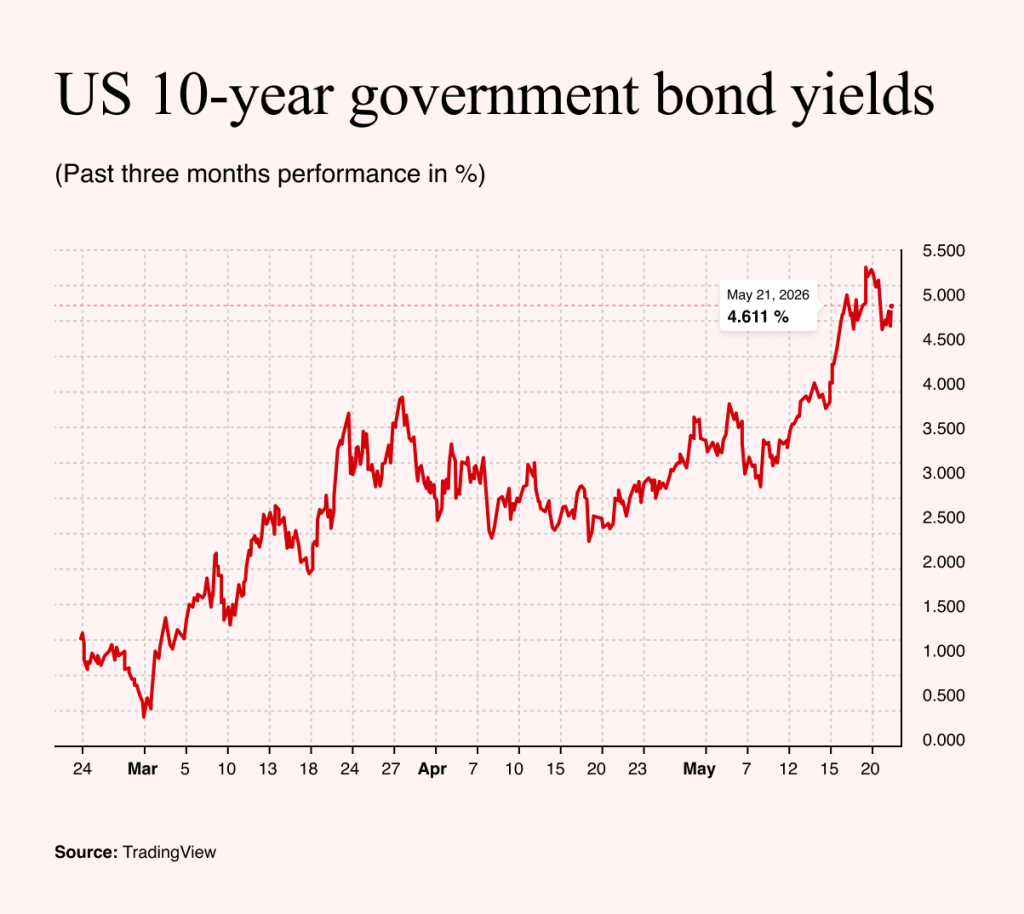

Whenever 10-year US Treasury yields approached 4.4% during the crisis, a softer US posture toward Iran typically followed, easing pressure on both oil prices and borrowing costs.

Since 14 May, however, yields have moved decisively above that threshold. Investors therefore assume the US administration will once again try to bring them lower. This expectation explains why markets still believe Trump ultimately needs a rapid resolution to the crisis.

Every additional day of elevated yields means one thing: higher financing costs for America’s enormous debt burden. And the larger the debt becomes, the less willing markets are to finance it cheaply.

Geopolitically, demand for US bonds is weakening as well. Middle Eastern states, traditionally major buyers of Treasuries, may now need to spend heavily rebuilding after the war. That means selling assets rather than accumulating US debt. Investors have also noticed that American weapons systems failed to fully shield regional allies from Iranian drone attacks.

In other words, purchasing US bonds in exchange for security guarantees suddenly appears less attractive. At the same time, many developing economies are reducing their dollar reserves to defend their own currencies and soften the impact of expensive imported energy.

Together, these pressures are creating a dangerous environment for the bond market. Any single factor might be manageable, but their convergence is far harder to contain.

Pressure on the Real Economy

This situation poses a serious problem for the US Treasury. Higher yields not only increase debt-servicing costs but also feed directly into the housing market.

Thirty-year Treasury yields serve as the benchmark for US mortgages, with lenders typically adding another one to one-and-a-half percentage points. Mortgage rates therefore begin around 6% – an extremely high level for the American economy.

That raises the prospect of renewed stress in the housing market alongside broader economic weakness.

At this point, the only realistic way to ease pressure on bond markets would be reopening the Strait of Hormuz. Until then, yields are likely to keep climbing, along with the systemic risks beneath the global financial system.

Margin Debt and the Illusion of Endless Optimism

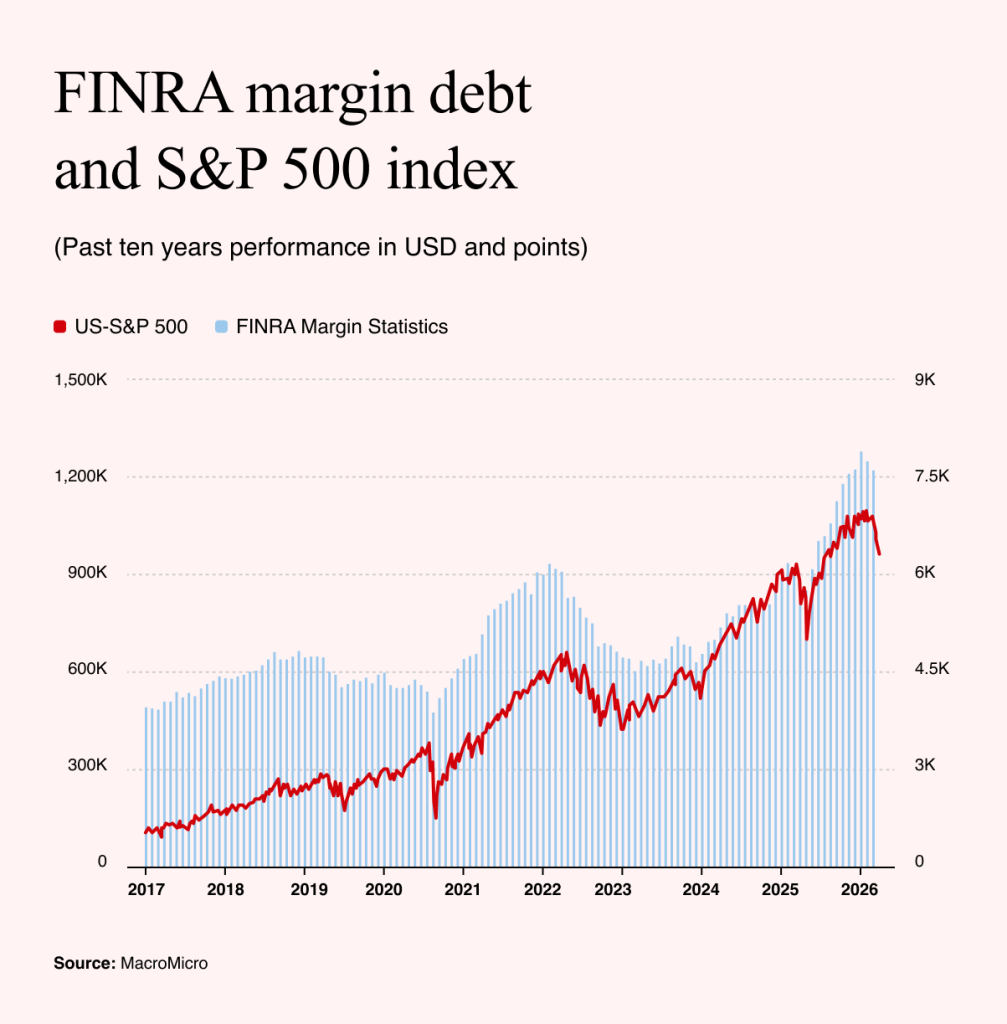

Another warning signal receives far less attention but may be equally dangerous: the record amount of borrowed money flowing into US equities. Margin debt reached $1.3tn in April, the highest level on record. In practice, this means the stock market is increasingly driven not merely by optimism but by leverage.

Historically, this is a late-cycle signal. Retail investors borrowing aggressively to buy stocks usually reflects the belief that risk has effectively disappeared. What makes the situation extraordinary is the backdrop against which this optimism persists: hundreds of tankers stranded near Hormuz, rising inflation, slowing global growth and a leadership transition at the Federal Reserve.

Leverage works brilliantly while markets rise, magnifying gains and reinforcing confidence. But once markets reverse, leverage operates in the opposite direction.

A sufficiently sharp decline forces investors either to inject additional cash or liquidate positions. That is how ordinary corrections become avalanches.

And this is where two seemingly separate worlds suddenly collide.

On one side, bond markets are driving up the price of money and confronting Washington with the costs of massive indebtedness. On the other, equities are sitting atop record levels of leverage.

If geopolitical tensions, expensive energy and rising yields begin weighing seriously on stocks, forced selling could spread rapidly through the system.

US bonds are not the only time bomb. Another is ticking inside the stock market itself.

Nvidia and the Limits of Investor Miracles

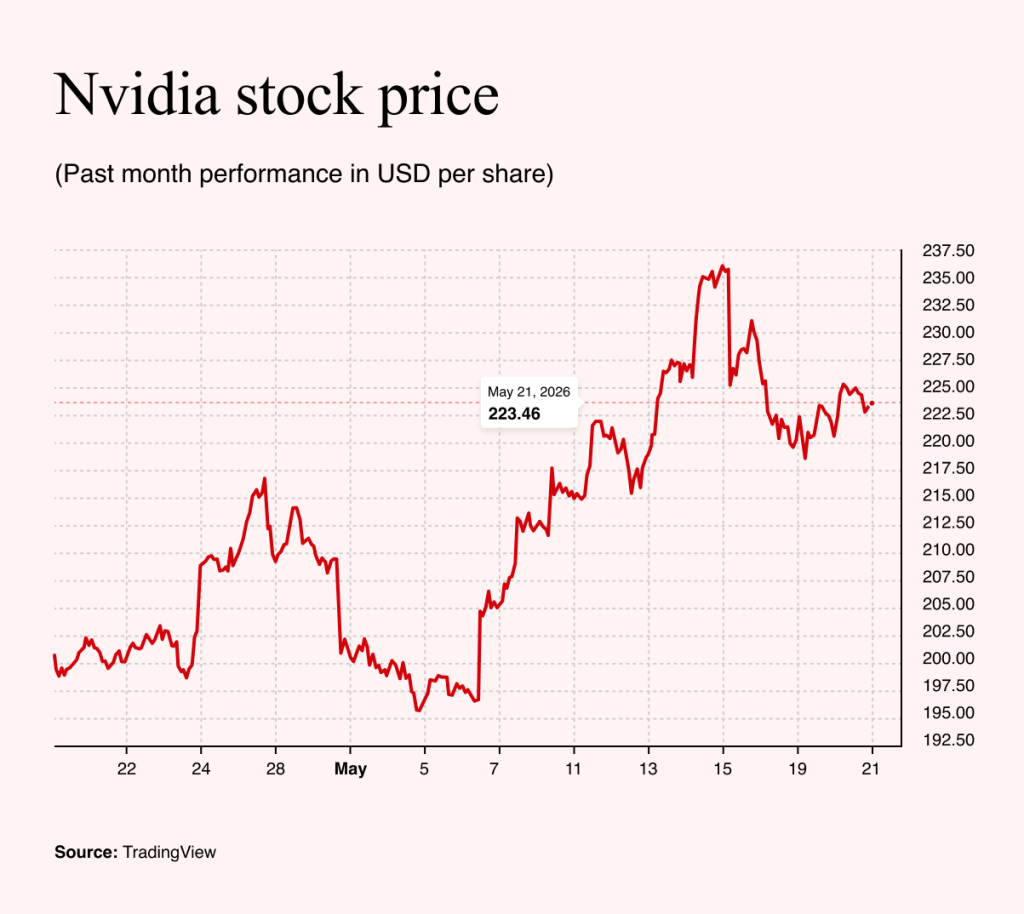

At the moment, only artificial intelligence appears capable of sustaining market optimism. That is why Nvidia’s earnings report after Wednesday’s close became so important.

The context matters.

Nvidia shares have risen 18% since the start of the year – an excellent result for almost any company. Yet for a firm that has become the symbol of the AI revolution, investors increasingly treat such growth as insufficient.

The era of exponential stock appreciation appears to be over. Speculative enthusiasm has partly shifted toward competitors such as Intel and AMD, as well as adjacent sectors like memory chips.

Paradoxically, Nvidia now resembles a relatively mature growth company. Its price-to-earnings ratio of 46 still makes it expensive, but compared with other AI-related stocks, it is no longer unusually stretched.

That cooling of enthusiasm has unnerved investors for months. Nvidia’s results therefore needed to be exceptional to sustain the AI narrative. And they were. First-quarter revenue reached a record $81.6bn, comfortably exceeding analyst expectations. Adjusted earnings per share of $1.87 also beat forecasts.

More important was the company’s guidance. Nvidia expects second-quarter revenue between $89.2bn and $92.8bn, once again above market estimates. The company also announced a new $80bn share buyback program and raised its dividend from a symbolic one cent to 25 cents per share.

The message was unmistakable: Nvidia is generating so much cash that it can continue growing aggressively while simultaneously returning capital to shareholders.

The underlying numbers remain extraordinary. Over the past three years, total revenue has risen by 1,035%. Ironically, however, this success has become part of the problem. The results were exceptional and exceeded expectations across the board. Yet that is no longer enough.

The stock barely moved and later weakened modestly. Investors have grown accustomed to miracles – and miracles become mathematically impossible once a company approaches a $5tn valuation.

Nvidia now faces a new kind of challenge: the company continues to grow at revolutionary speed, while the market increasingly prices it as though the revolution itself has already happened.