With critical midterm elections just months away, a beleaguered President Trump is facing down an old and intractable political foe: inflation.

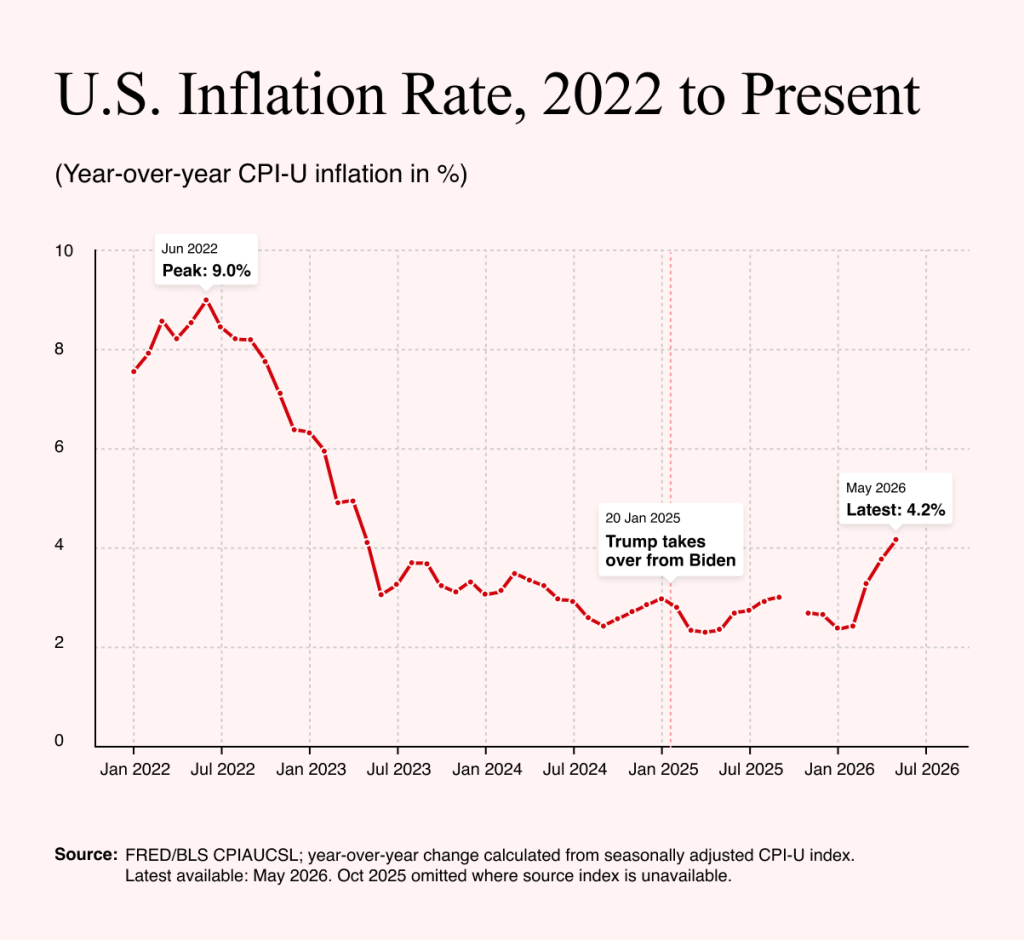

The latest data, released this week, shows prices rising by 4.2% over the year to May – a high for the Trump presidency. But much more alarming is the steep nature of the curve, with prices suddenly shooting upward on a trajectory that could become devastating if the trend is not countered.

Unfortunately, as economists throughout history can attest, countering inflation is one of the most challenging policy issues a leader can face. The most reliable fix for increasing prices is a slump in demand that permits the supply and demand mechanism to reset itself. But a slump in demand has another name: recession.

Despite Trump’s insistence that he is the economic president, the Oval Office’s occupant has never been one to instinctively understand – or to articulate an understanding – of the causes and cures of inflation. Indeed, his second presidency has been marked by a relentless campaign of policy choices that appear almost designed to drive up costs. It is those chickens that might be coming home to roost now in the late spring of an election year.

What are those choices? There are three.

Tariffs Directly Drive Price Increases

First, the president’s tariff policy, designed on its face to reshore American manufacturing and jobs, is deeply and directly inflationary in effect. Consider what it does: it increases prices directly and indirectly. Consumers who buy goods from tariffed nations pay an extra tax, driving up their costs and eating into their household budgets.

Meanwhile, consumers who buy American must account for the fact that even for products produced inside the United States, it is likely that tariffed components or ingredients are part of the price chain. Think of imported steel and aluminum for American cars, for example. Or fertilizer for American agriculture, now being supported by the president in another round of subsidies that are arguably only necessary because of his initial decision to impose tariffs.

Iran War Spikes Oil Costs

The second area where Trump’s policies have been inflationary is, of course, in foreign relations. No single act has driven up prices more than his decision to wage a war on Iran that seems to risk permanently altering the politics of the Strait of Hormuz in a way that will, for years to come, drive up the costs of extracting crude oil through that particular global artery. Iran, for its part, insists that it should now have a permanent right to tax and tariff vessels transiting the strait.

Meanwhile, the mines laid by the conflict will pose an insurance risk for shipping, and the political instability in the region will also result in a prolonged period where prices are higher.

The United States, of course, produces its own oil and gas in quantities that allow it to be strategically self-sufficient – but even though there is no fear of American forecourts running dry, the fact remains that fossil fuels are priced as a global commodity, and the president’s actions have been instrumental in driving those prices higher.

Pressure on the Fed to Pursue Inflationary Policies

There is also a third area where the president has been relentlessly inflationary in his rhetoric and his actions, and that relates to interest rates.

Since he took office for a second time, Trump has been persistently angry with the US Federal Reserve – which is nominally independent of him – for refusing to lower interest rates. The president tried on several occasions to prematurely remove the chairman of the Federal Reserve and has now succeeded in appointing his own man to the job. The president has also made it explicitly clear that he expects interest rates to be lowered.

Yet lowering interest rates would be directly inflationary: doing so would lead to more borrowing and more spending by businesses and consumers. Trump sees this as desirable since more investment in the economy means more jobs – but more investment also means more demand. The Federal Reserve has been very hesitant to obey the president for this very reason. To lower rates now would be pro-inflationary when inflation is spiking.

Taken together, these three policy decisions and areas have taken some time to have an impact, but the graph above shows how suddenly their effects are being felt.

More concerningly, it seems vanishingly unlikely that the president has much of a plan to reverse them, absent his push for a peace deal with Iran which may, or may not, return some semblance of stability to global oil markets.

Even there, however, there is a problem: supply has been constricted for so long that the economy may now be mere weeks from a crisis. “Industry models show the collapse of crude inventories within a matter of weeks could push the cost of oil up by 50 percent or more – sending the price of gas at the pump soaring past $5 per gallon”, the Washington Post wrote this week.

There is another problem, also, as reported by the Wall Street Journal: one reason for oil prices remaining low is that China – the paper says – is “propping up the world economy by importing a lot less oil”. The People’s Republic has consciously tried to keep prices stable by cutting back on its own imports, but this may not be sustainable for long.

If either or both of those threats unfold over the next few months, they could turn the Trump inflation problem into a historic political inflation crisis for the president.

If that happens, then many economists and skeptics who have viewed his policies over the past year as inflationary will be vindicated. Given the likely impact, however, it is unlikely that any of the saner ones would take much pleasure in being proven correct.

Meanwhile, the political effects are not hard to predict. With control of both chambers of Congress at stake this November, and higher prices a key driver of political sentiment, the president’s political security looks precarious. He was elected on his opposition to the record inflation of the Biden presidency and on a promise to address it. Failure to meet that campaign promise could have very grave consequences when Americans go to the polls.