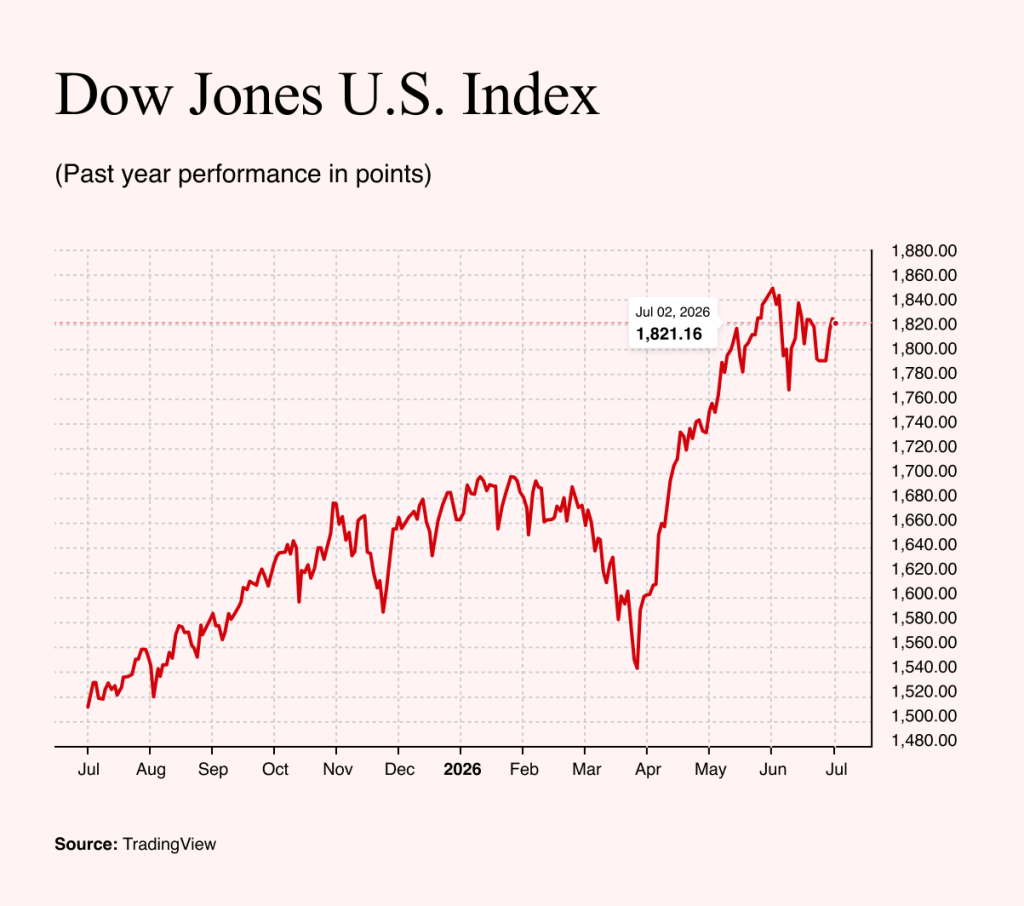

Since the US and Israeli attacks on Iran began, financial markets have entered what appears to be an almost surreal phase. Yet, US indices are breaking one historic record after another.

Most recently, this week, the Dow Jones Industrial Average climbed above the 52,000-point mark for the first time in history. That rally has come despite the increasingly entrenched standoff between the US and Iran.

The recently signed memorandum of understanding resembles more a memorandum of misunderstanding. Each side has endorsed language that reinforces its own interpretation while downplaying the points that would require significant concessions.

Slow-Moving Tankers and an Impatient President

Financial markets have yet to price in any significant geopolitical risk, and Brent continues to trade at around $70 a barrel. Donald Trump, however, has reportedly expressed frustration that US gas station prices have not fallen in line with the drop in global oil prices. Brent crude has already fallen by more than 36% from its recent peak.

Bloomberg reported that, despite continued rhetorical exchanges between the two sides, tankers carrying more than 10 million barrels of oil are once again passing through the Strait of Hormuz every day. While that represents a positive development, traffic remains at only about half the levels recorded before the conflict began.

Many experts also point out that, although the strait is navigable, ships still require several weeks to reach their destinations. Supply disruptions could therefore continue to weigh on GDP growth in a number of countries, further weakening the global macroeconomic outlook. Nevertheless, despite heightened geopolitical and energy-related uncertainty, US equity markets remain close to record highs.

The Japanese Yen: A Ticking Time Bomb

Renewed conflict in the Middle East and disruptions to energy supplies are not the only risks facing investors. Virtually unnoticed, the Japanese yen has plummeted to historic lows against the US dollar.

This is a very disturbing development. The next major financial crisis is likely to be of a monetary nature, with currencies coming under pressure as public debt continues to mount and the consequences of decades of central bank policy become increasingly apparent.

The Japanese yen is a perfect example of this. Its long-term depreciation is largely the result of four decades of exceptionally loose monetary policy. Rebuilding confidence in the Japanese currency will therefore be a lengthy and complicated process that cannot be easily achieved by one or two policy decisions.

The second reason is that the Bank of Japan faces no easy solution. Either the yen will continue to weaken – a highly likely scenario, particularly while other central banks, including the Federal Reserve, the European Central Bank, and even the Czech National Bank, are adopting hawkish rhetoric.

In that scenario, Japanese inflation would continue to rise, mainly because Japan remains heavily dependent on imported commodities, including oil. A weak yen pushes up import prices even when the dollar price of oil declines. Eventually, the Bank of Japan would have little choice but to raise interest rates.

The alternative is to act now by increasing rates to support the yen and curb inflation. However, such a move would also drive up Japanese government bond yields. That, in turn, would reduce the attractiveness of yen-funded carry trades because borrowing costs would rise.

A carry trade involves borrowing Japanese yen at very low interest rates and investing the proceeds in higher-yielding assets denominated in other currencies. Two years ago, during the summer, Japanese financial markets experienced the full impact of what this strategy can do. Another turbulent August cannot be ruled out. In any case, Japan may only be the first warning sign, as a number of other economies also appear vulnerable to a currency crisis.

Artificial Intelligence: Salvation or Bubble?

Why, then, are US stock indices continuing to reach new highs despite these mounting risks? The primary driver remains investors' enthusiasm for companies linked to artificial intelligence and the semiconductor industry.

More recently, however, investors have begun rotating within this sector. Investors are losing faith in the largest members of the Magnificent Seven – the seven dominant US technology companies – whose spending on AI infrastructure has reached unprecedented levels. Doubts are growing that these companies will be able to recoup their expenses with AI profits in the foreseeable future.

As a result, investors have shifted towards companies supplying components for data centers, including Micron and Western Digital. Even so, it might be premature to dismiss the prospects of the Magnificent Seven altogether.

Meta has introduced a strategy aimed at selling off its excess computing capacity and offering outside customers access to its AI models. With this move, Meta hopes to create a new line of business capable of challenging cloud computing giants such as Amazon, Alphabet and Microsoft.

Rather than allowing its astronomical AI spending – which is expected to reach an incredible $145bn this year – to become a source of investor concern, Meta is turning it into a potentially significant new revenue stream.

However, this move brings a very interesting twist to the aforementioned sector rotation. Market leadership appears more fluid than previously thought. Investors welcomed the decision, sending Meta shares up by more than 8%. Even after that rally, however, the stock remains below its level at the beginning of the year.

Where Are Those Job Cuts?

One final set of data from the US labor market highlights just how complex the AI story remains. If AI were already transforming the economy on the scale many expect, its adoption might also be expected to result in substantial job losses. So far, however, labor market data provides little evidence of such a trend.

Earlier this week, the latest Job Openings and Labor Turnover Survey (JOLTS) showed that US job openings rose by 9,000 to 7.6 million, the highest level since May 2024.

The ratio of job openings to unemployed workers in the US has also improved. Judging by these figures alone, it would appear that artificial intelligence in the United States is creating new jobs rather than destroying them.