The world gained one million additional millionaires in 2025, while the total wealth on the planet expanded by some 10.8%. Those are findings of UBS Bank in its Global Wealth Report for 2026.

The figures, which the bank says are an accurate count for about 92% of the global economy, show, however, that the vast majority of the wealth increase can be attributed to an increase in property values, with land and property owners seeing considerable increases in their theoretical – not liquid – wealth. The report also highlights a pervasive gap between the so-called “haves” and “have-nots”, with people worth more than $1m comprising about 1.5% of the global population, but controlling over 48% of the world’s total assets.

Meanwhile, those with less than $10,000 in assets comprise 42% of the global population, but control just 0.6% of the world’s wealth. A figure that might inspire even this writer to start humming the Internationale.

The other concerning figure? That while global wealth increased on average, the median amount of wealth actually fell in most jurisdictions. So, in plain English, it is a great time to be rich. It is not a great time to be somewhere in the middle, or below that level.

Is Growing Wealth an Illusion?

Since markets are governed by the price mechanism of supply and demand, and since the UBS report ties the increase in global wealth primarily to property and asset prices, a reasonable inference is that landowners and asset holders are being made wealthier internationally by market conditions that reflect housing shortages and property market crises across much of the world.

This is a self-reinforcing loop: as asset prices spiral upwards, so in turn do they become a more attractive investment strategy, and so in turn do investors seek to put their money into them, driving demand.

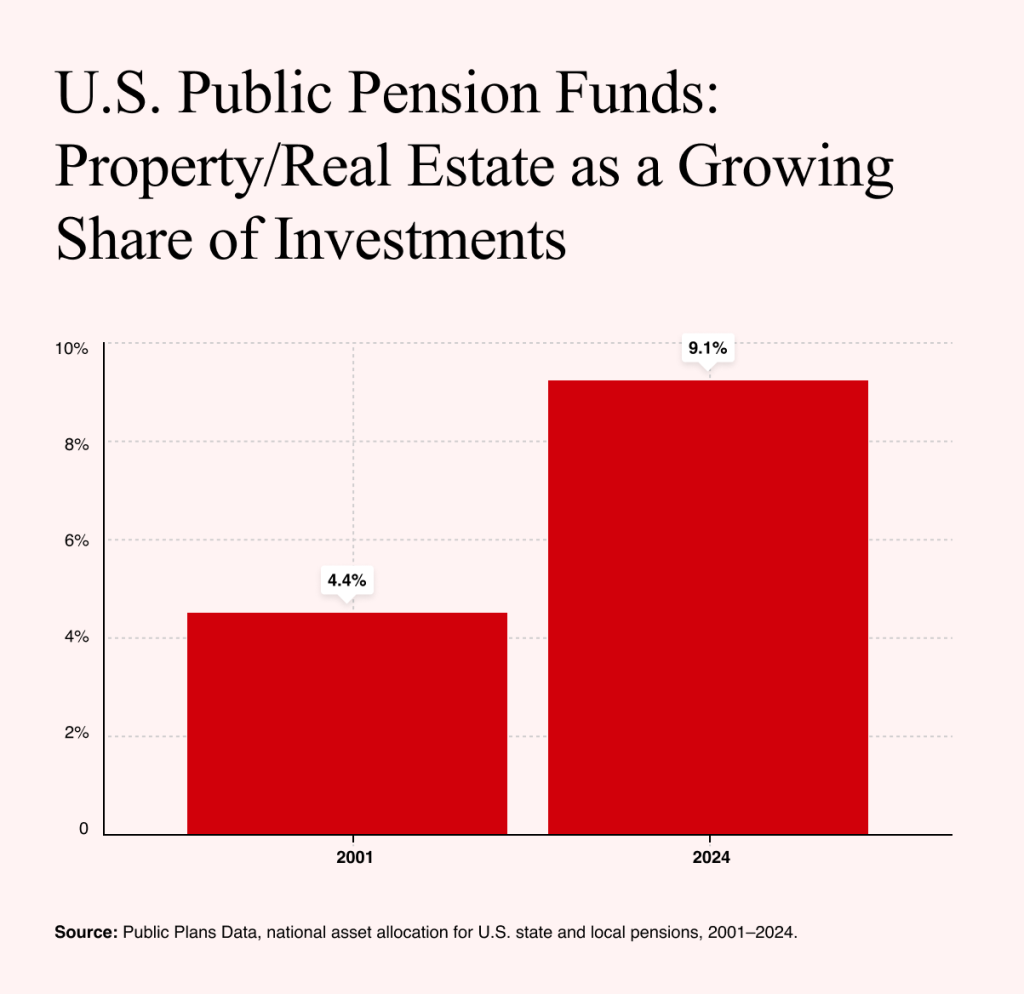

Data supports this: for example, over the past 20 years, US investment funds have more than doubled the share of their asset portfolios held in property and real estate, often making large asset acquisitions that, in turn, drive up the price and demand for those assets.

The underlying reason for this should be of concern. Why are so many investment funds shifting – slowly but consistently – away from shares and equities and towards property and hard assets?

One explanation is simply that investors have less faith than they once did in the monetary system itself. The past two decades have seen a consistent pattern of so-called quantitative easing by central banks and an explosion in government-held debt. The US national debt, for example, approaches $40tn. Given the possibility that this may only ever be dealt with by devaluing the dollar to make the debt more bearable, many wealthy people have chosen instead to invest in concrete assets – like land and property – that cannot be devalued by administrative fiat.

This is arguably having profound consequences for the rest of us: shifting the price and accessibility of property ever higher and further out of reach, which in turn requires yet more government spending to support an underclass of citizens for whom housing itself is ever less affordable.

The Instability Risk

The ingredients for very severe economic turmoil are already in place, if examined closely enough. This is because so little of the total global wealth increase is obviously productive: much of the increase in the value of the world’s assets is being driven disproportionately by price increases in existing assets, driven by scarcity and a degree of asset hoarding.

Meanwhile, the underlying state of the Western financial system is precarious. The enormous gulf between the asset-holding and asset-poor classes creates a political stability risk, and the immense borrowing of many Western states – which largely exists to bridge the gap between rich and poor – creates sovereign-debt risks.

This is not to say that the UBS report predicts a depression. It does not. Indeed, UBS is doing what banks do: counting assets, assessing markets and calmly informing its clients that the rich have, once again, become richer.

But the report does illustrate, in stark numbers, the increasingly strange nature of the economy that decades of Western economic policymaking has built. If it proves one thing, it might be that a society can get richer on paper while becoming poorer in reality. A house can double in value while the family living in it becomes more anxious, not less. A pension fund can become more secure while the young worker funding it can no longer afford the first step onto the property ladder, and so on. Workers can be told they are living in a richer country, when many of them feel poorer – because in relative terms, they are.

That last point matters politically.

The Broken Promise of Post-War Capitalism?

For most of the post-war period, the promise of Western capitalism was not simply that wealth would exist but that, with hard work and good decision-making, that wealth would be broadly attainable. Work hard, save money, buy a home, raise a family, retire with dignity: that was the offer. It was not utopia, or ever presented as such. It was, however, the basic bargain that made capitalism politically legitimate to millions of people who were never going to be rich but who could reasonably expect to be secure. And it is a bargain that is now under pressure.

If the chief source of wealth creation is the rising price of assets already owned by the affluent, then that reflects market failure rather than wealth creation. There is no trickle-down effect, in Reagan’s terms, from wealth derived by a 20% increase in the value of a field.

This is why the politics of housing has become so combustible across the Western world. It is not merely that rents are high, or that mortgages are expensive, or that planning systems are dysfunctional, though all of those things are true. It is that housing has quietly ceased to be treated primarily as shelter and has instead become one of the main repositories of global wealth.

This is the kind of situation in which revolutionary socialism and leftism thrive and is probably connected to the increase in such sentiments in many Western democracies. The public looks at these figures – even if they do not understand them – and sees them reflected in the reality around them every day. It explains the increased political toxicity of landlords, the popularity of rent controls, and the election of figures like Zohran Mamdani in New York. Resentment of asset-holding classes has triggered almost every left-wing revolution in history, and it now threatens another.

The UBS report shows a world swimming, theoretically, in cash. But France, under Louis XVI, was also one of the wealthiest countries in the world, on paper.

As the saying goes: those who do not understand history are doomed to repeat it. Unfortunately, it may also be said that those who do understand history are doomed as well – to watch everybody else repeat it.