US stock markets set another all-time high last week, refusing to fall in almost any circumstances. Two forces continue to drive the rally: hopes of a peace deal between Iran and the United States and enthusiasm about artificial intelligence.

Both rest on increasingly fragile foundations. The upward momentum now pushing indices to new records could quickly reverse if geopolitical relief proves premature, or if investors discover that the AI trade is not pricing in a clear future but a jumble of conflicting expectations – from technological revolution to investment disappointment.

Geopolitical Stalemate and the Oil Market

Developments around Iran are beginning to resemble an endless political soap opera. We appear no closer to a final agreement than we were a month ago, yet markets no longer seem to price in the risk that no such agreement may come.

The main issue is now merely the extension of the ceasefire for another two months. Even that comes with several catches.

The first is that almost every day brings one or two reports of clashes, defensive attacks or new incidents. Any one of them could become the detonator for a wider conflict.

The second problem is that the demands and expectations of both sides have barely moved in a month. Without compromise, the same crisis will return in two months. For now, there is little sign that compromise is possible on the key issues, including enriched uranium and the reopening of the Strait of Hormuz.

The situation is deadlocked, but markets do not seem to mind. What is clear, however, is that the crisis is tightening economic conditions across the world, including in countries not directly involved in the conflict but crucial to the global economy. Japan is one example.

Japan’s oil reserves have fallen from 243 days before the conflict began to 202 days today. Oil imports have dropped by more than 900,000 barrels per day. Japan has not yet been able to make up that shortfall. Even if a rich country such as Japan can do so, it will come at the expense of poorer Asian states. The oil shortage will not disappear. It will merely spill over into weaker economies.

The shortfall in supplies passing through the Strait of Hormuz cannot simply be replaced. Its impact can be reduced, as we are seeing now, mainly through the release of strategic reserves. That is helping to contain the oil price for the moment, but this cannot last forever.

Exxon chief executive Neil Chapman has made the same point, arguing that the current oil price does not reflect reality. If nothing changes, he says, oil could reach $160 a barrel within weeks if the strait is not reopened. Markets have yet to price in that scenario.

They were equally unmoved by the latest US Personal Consumption Expenditures (PCE) inflation data for April. PCE inflation reached 3.8%, its highest level since May 2023. This is the inflation measure most closely watched by the Federal Reserve. The 2% target has clearly been overshot, which should logically push the Fed toward a more hawkish stance.

How did markets respond to this bad news? Virtually not at all. The figure was in line with expectations, and that was enough for investors to conclude that the inflation increase had already been fully priced in.

Will AI Take Jobs from Software Companies?

Artificial intelligence brings its own set of uncertainties. Earlier this year, many traditional software companies sold off sharply on the assumption that language models would soon replace them. Software firms unexpectedly became one of the market’s early AI casualties. The story was simple: language models would write applications themselves, and development teams would no longer be needed.

Snowflake’s latest results suggest the story may be more complicated. Snowflake, which specializes in data warehousing and enterprise data management, had until recently been treated by investors as one of the classic software companies likely to suffer from the rise of AI.

After its latest results, that narrative changed in a single day. Shares rose 38% after both revenue and profit beat analysts’ expectations and the company raised its full-year outlook.

Snowflake reported fiscal first-quarter revenue of $1.39bn, up 33% year on year, compared with market expectations of $1.3bn. Adjusted earnings came in at 39 cents per share, above expectations of 32 cents.

The outlook was even more important. The company raised its full-year product revenue forecast from $5.66bn to $5.84bn.

In other words, at the very moment when some investors assumed AI would begin eating into traditional software, Snowflake showed the opposite. AI may increase demand for its services.

The Snowflake case shows how much the market’s approach to AI is still shaped by perception and emotion rather than sober analysis.

Trump Breaks All the Rules

The war in Iran has also produced a series of questionable oil trades, which repeatedly appear to have tracked shifts in the US president’s statements on social media.

Trump is known for abrupt changes in tone and policy. If anyone consistently profited from those swings, they would likely have had access to unusually timely information. Yet given the nature of the oil market, proving insider trading would be extremely difficult.

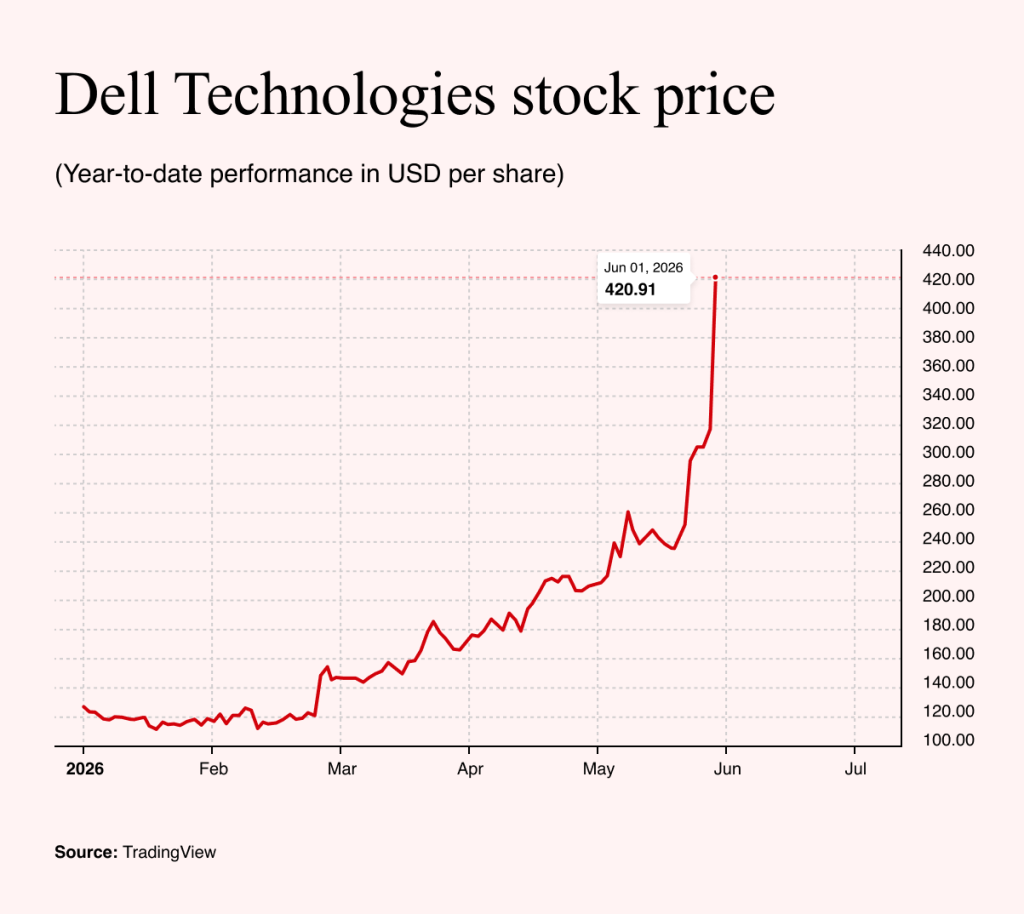

In the case of Dell, however, the president has pushed the boundaries even further.

According to published disclosures, accounts linked to Trump bought between $1m and $5m worth of Dell shares on 10 February.

Nine days later, on 19 February, Trump spoke at the Coosa Steel Corporation plant in Rome, Georgia. Addressing workers on the economy, tariffs and the Trump Accounts program, he ended with an unusual piece of investment advice: buy Dell stock.

That was not the end of it. According to several media reports, Trump mentioned Dell again on 8 May at a Mother’s Day event at the White House. While thanking the Dell family, he once more advised the public to go and buy Dell.

Anyone who took the president’s advice and bought Dell shares as a Mother’s Day gift can now feel rather pleased.

The story reached its climax last week. Dell announced extremely strong results, its shares jumped almost 40% and details emerged of a new five-year Pentagon contract worth $9.7bn.

The company reported revenue of $43.8bn, up 88% year on year. More than a third of sales came from AI-optimized servers, whose revenue rose 757% year on year. Dell also raised its full-year AI revenue estimate from $50bn to $60bn.

Fundamentally, this is a strong story. In the eyes of the market, Dell is transforming itself from a traditional PC maker into a major supplier of AI infrastructure.

On the merits, the company’s management and business strategy deserve credit. But fundamental analysis is one thing. Having a president in the White House who buys your shares, publicly recommends them and then oversees a government that hands you a multibillion-dollar Pentagon contract is something else entirely.