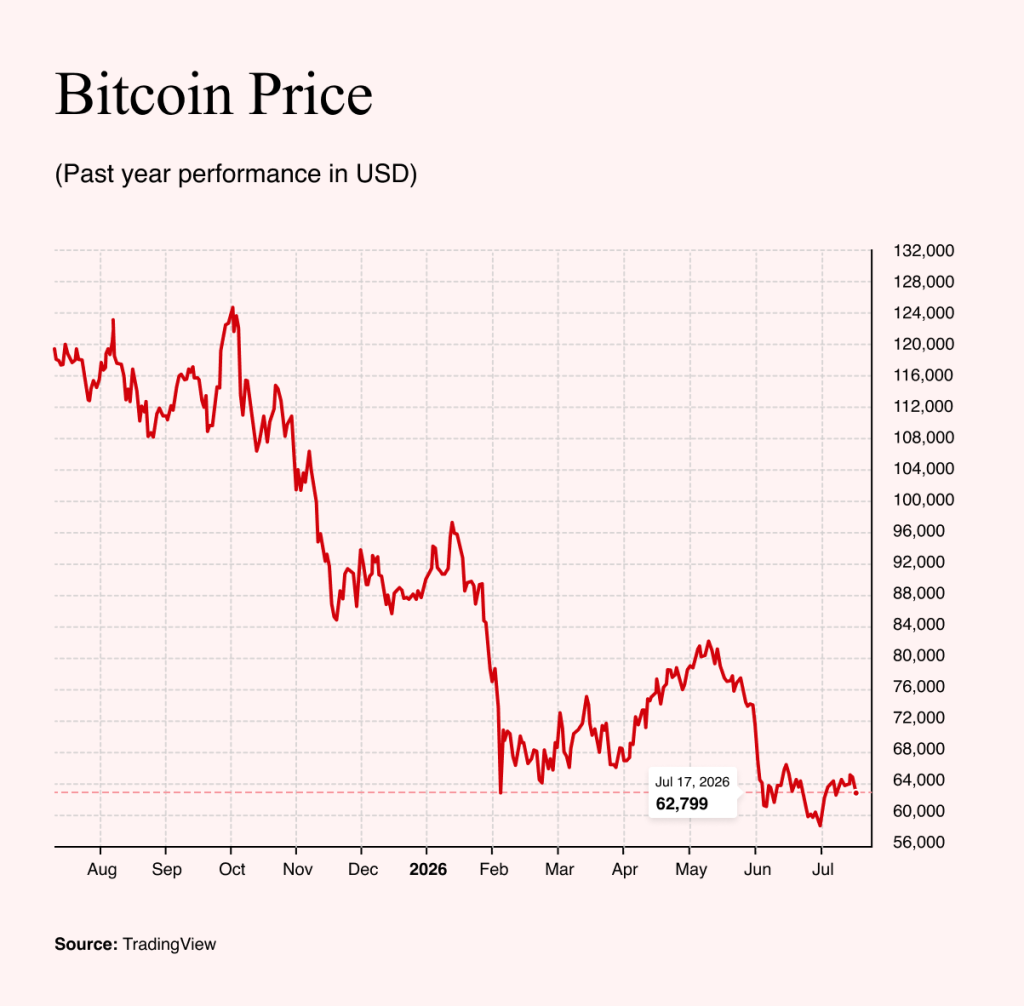

Even though Bitcoin has existed for more than 17 years, a hard-core group of detractors still believes its value will eventually collapse to zero. Such predictions surface regularly, typically whenever the cryptocurrency enters a bear market and its price begins to tumble.

So far, however, none of them has come true. After every previous crash, Bitcoin has recovered and gone on to surpass its previous all-time high. That makes it unlikely we are witnessing its demise this time either. The only certainty is that the prolonged downturn is once again exposing the vulnerabilities of the broader cryptocurrency market.

Bitcoin itself may not be the first casualty. Speculators who have built increasingly complex financial structures around its rise are typically the first to come under pressure. The clearest example is Michael Saylor and his company Strategy, formerly known as MicroStrategy.

The current market offers Bitcoin's critics plenty of ammunition. Strategy's share price has fallen by about 80% over the past year. Investors are no longer concerned solely about Bitcoin's decline; they are increasingly questioning Saylor's entire financial strategy.

Those doubts deepened when Strategy sold Bitcoin for the first time. Saylor had long argued that selling was the biggest mistake a Bitcoin holder could make.

The first transaction involved just 32 Bitcoin, but it was quickly followed by a much larger sale worth $216m. Although these amounts are insignificant compared with the company's holdings of more than 847,000 Bitcoin, the sales shattered the perception that Strategy's reserves were untouchable.

The principle that Bitcoin would never be sold has effectively been abandoned. When one of the cryptocurrency's most committed advocates changes course, it signals that the situation has become serious.

At the same time, Saylor could hardly have believed Bitcoin's price would rise indefinitely. He is well acquainted with the theory of halving cycles and the recurring pattern of sharp rallies followed by steep corrections. His view of Bitcoin itself has not changed. Rather, he has reconsidered whether Strategy should treat its holdings as entirely untouchable. How, then, should investors interpret this shift in strategy?

How Strategy’s Bitcoin Model Worked

To understand the current situation, it is first necessary to explain the mechanics of Strategy's Bitcoin model. The company began as a conventional software business, but in 2020, it started converting its excess cash into Bitcoin.

At a time when borrowing costs were exceptionally low, this appeared more attractive than leaving billions of dollars sitting idle on the balance sheet. Bitcoin's price was rising rapidly, while financial assets across the board were appreciating. Strategy was far from alone in pursuing the idea.

Tesla and the payments company Block also added Bitcoin to their balance sheets. Later, companies including Japan's Metaplanet and the US healthcare firm Semler Scientific adopted variations of Saylor's approach.

The difference was one of scale. For most companies, Bitcoin remained only one component of their assets. At Strategy, however, accumulating and holding Bitcoin gradually became the company's primary business. Once its own cash reserves were exhausted, it turned to issuing new shares and bonds through a relatively straightforward financial mechanism.

Strategy's shares frequently traded at a substantial premium to the value of the Bitcoin held on its balance sheet. That allowed the company to issue new shares at elevated prices, use the proceeds to buy additional Bitcoin, expand its reserves and repeat the process.

Investors were therefore buying more than a stake in a software company. They were buying into the expectation that Saylor could continue increasing the amount of Bitcoin backing each share by tapping the capital markets. As long as Bitcoin continued rising and investors remained willing to pay a premium for Strategy's shares, the model worked remarkably well.

The company later added another layer by issuing convertible bonds and high-dividend preferred shares. Its flagship product became the STRC preferred share, marketed under the name Stretch.

Unlike Strategy's common stock, STRC is a separate security aimed primarily at income-focused investors. It initially offered an annual dividend yield of 11.5% and has since increased it to 12%. That, however, is where the problems begin.

The Engine for New Capital Has Stalled

As soon as prices began to fall, the entire mechanism started to break down. STRC preferred shares dropped below their $100 par value, making further issuance uneconomical because investors could buy the same security more cheaply on the open market.

Moreover, at such depressed prices, even a 12% dividend is unlikely to compensate investors for the risk of further capital losses. Strategy's common shares have run into the same problem. Once investors were no longer willing to pay a substantial premium over the value of the company's Bitcoin holdings, issuing additional shares ceased to make financial sense because it would merely dilute existing shareholders.

With both funding sources effectively shut off, Strategy has shifted its focus from steadily accumulating more Bitcoin toward protecting its balance sheet.

Will the Halving Cycle Save Strategy?

The company’s defensive strategy now rests on a single assumption: that the current downturn in Bitcoin will not last too long. According to the theory of halving cycles, the bear market should come to an end in early autumn. So far, Bitcoin has followed that pattern with remarkable consistency. Previous halvings have been followed by a sharp rally, a new all-time high and then a steep correction.

This time, however, one factor could make the cycle different: artificial intelligence.

In previous cycles, Bitcoin was one of the primary destinations for speculative capital seeking outsized returns. Today, it no longer occupies that position alone.

Investors can instead direct the same capital toward manufacturers of memory chips, semiconductors, servers and other infrastructure essential to artificial intelligence. Companies such as Micron and SK Hynix now offer many of the same attractions that once drew speculative investors to Bitcoin: rapid growth, a compelling narrative and exposure to a potentially long-lasting technological transformation. Bitcoin has therefore gained a formidable competitor in the battle for speculative capital.

That does not necessarily mean the halving cycle has stopped working. Artificial intelligence could, however, significantly alter its dynamics. If it continues attracting capital that might otherwise have flowed into cryptocurrencies, Bitcoin's return to the spotlight could be delayed or less pronounced than in previous cycles.

That is ultimately what Strategy's future depends on. If the halving cycle regains momentum, Saylor's recent decisions may prove to have bought the company valuable time. If speculative capital remains concentrated in artificial intelligence, however, the current Bitcoin winter could last far longer than Strategy's financial model anticipates.