Markets continue to drift higher despite a deteriorating geopolitical and macroeconomic environment. Two forces explain this.

First, investors are still betting on the Hollywood version of events, in which disaster is averted five seconds before it strikes. The situation between Iran and the US has deteriorated further this week and, if Iranian sources are to be believed, negotiations have broken down. Oil supplies are also dwindling by the day.

According to the heads of US oil companies, a collision between commodity markets and reality is inevitable. They differ only on the timing. Some are pointing to mid or late June.

In any case, time is running out. Unless a last-minute rescue arrives, prices at the pump will begin rising at the worst possible moment: during the summer holidays. Trump risks a serious loss of popularity, which gives markets another reason to believe that everything will still end happily.

AI Keeps the Rally Alive

Belief in a happy ending would not be enough on its own. Markets are still being carried by the artificial intelligence story. It is likely to receive fresh fuel in the coming days from two expected market events: SpaceX’s planned stock-market debut and Anthropic’s confidential filing for a US listing. If they succeed, the euphoria may last for several more weeks.

The lingering enthusiasm surrounding artificial intelligence, and the belief that the technology will fundamentally change the world economy, has once again reshaped the market narrative. The latest symbol of this wave is Japan’s SoftBank, whose shares have surged to record highs. SoftBank is not itself a classic artificial intelligence developer, but it is one of the major investors in the wider AI ecosystem.

Its value is based primarily on stakes in companies directly linked to the trend. The most visible is its stake in OpenAI, but even more important is its majority holding in Arm, the UK firm that designs chip architectures. Investors increasingly see Arm as a key player in the future of data centers and the computing infrastructure needed for AI.

Hopefully, however, SoftBank has learned to price risk more carefully. This is not the first time it has found itself at the center of a technology boom. At the turn of the millennium, it was one of the symbols of the internet frenzy. After the dotcom bubble burst, its shares all but collapsed.

Both the company and its founder, Masayoshi Son, learned then how thin the line can be between a vision of the future and a belief that begins to ignore reality. Son also suffered personal losses on an almost unimaginable scale.

His paper fortune, estimated at $76bn–$78bn at the height of the dotcom fever, plunged after the bubble burst. In a short period, one of the world’s richest men became a symbol of how quickly technological certainty can turn into painful sobriety. Masayoshi Son is now on a roll again, and his fortune is soaring along with SoftBank’s shares. That only sharpens the question of whether he can keep his technological vision closer to reality this time than he did during the dotcom rush.

Europe Looks Exposed

The reality remains that behind the record highs in US indices lies a harder truth: only two of the 11 sectors, technology and energy, are growing. The rest of the economy is left to cope with an inflationary shock and shortages of key raw materials that previously flowed unhindered through the Strait of Hormuz.

Europe, including its stock markets, will have to deal with the consequences of the crisis. Unfortunately, European indices are not made up of 40% AI-related technology firms, as is the case in the US. Nor does Europe have a key financial institution such as Japan’s SoftBank financing the development of AI.

The pride of European stock markets, the luxury goods sector, is going through harder times. Chinese demand for luxury goods remains weak. Demand from the wealthy in the Middle East is also falling, with many of them currently having other things to do than buy the latest Louis Vuitton handbag.

The ECB’s No-Win Choice

Europe’s entire economic environment may soon be tested by rate increases.

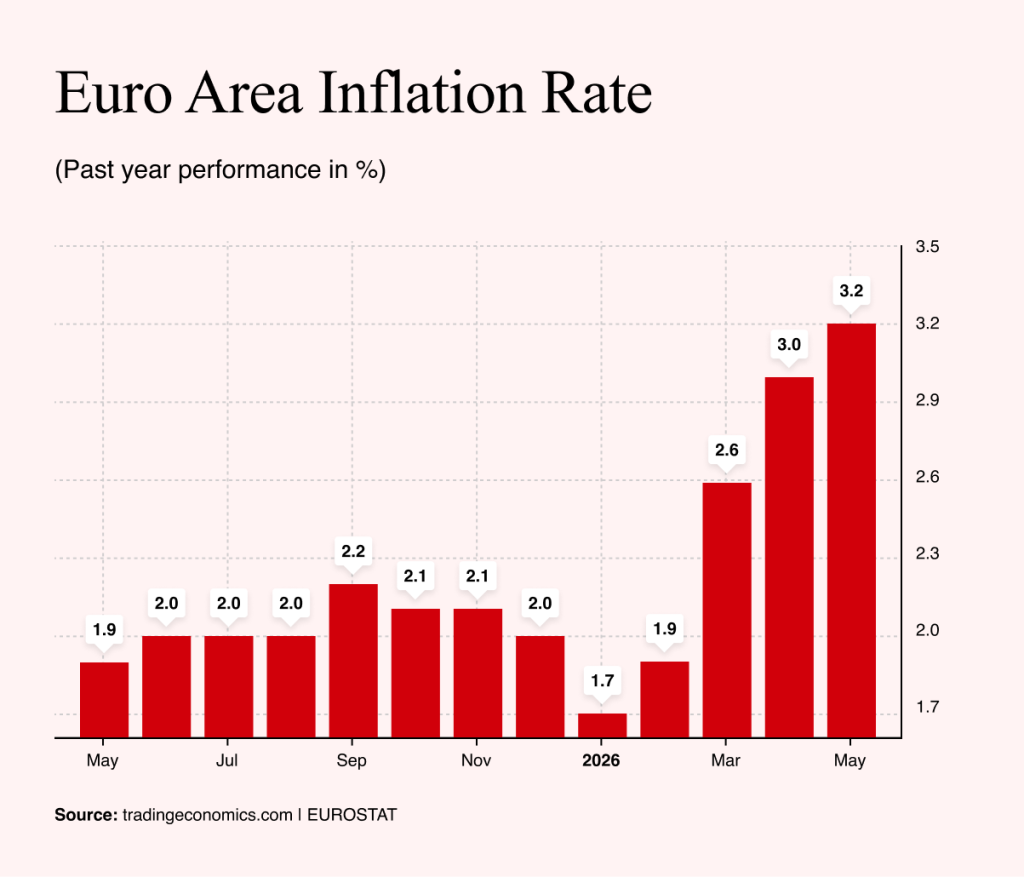

Eurozone inflation figures were released this week. Unsurprisingly, inflation accelerated from 3% in April to 3.2% in May. That has strengthened calls in the eurozone for intervention by the European Central Bank.

Since Germany is one of the countries where inflation is a particularly sensitive topic, it will surprise no one that ECB Executive Board member Isabel Schnabel is prepared to support higher eurozone rates at the next central bank meeting.

But such a hawkish move by the ECB is not universally welcome. After all, no central bank can fundamentally influence oil prices or unblock the Strait of Hormuz. If the oil price continues to rise, inflation will keep rising too. A 25-basis-point rate increase will not stop it.

In human terms, it is understandable that the ECB does not want to repeat the mistake it made in 2022, when its leadership reacted too late to rising inflation. But the bank made a different mistake in 2011, when it began raising rates in the middle of an economic slowdown for the same reason: rising energy prices.

If the central bank takes too hard a line, it could repeat the mistake of 2011 and slam on the brakes at a moment when the engine of European growth is already losing power. If, on the other hand, it does nothing, it will expose itself to suspicion that it is once again underestimating inflation risks.

The ECB therefore faces no easy choice between fighting inflation and supporting growth. It faces a much worse question: how can it convince markets and the public that it has the situation under control when the main sources of the problem lie beyond its reach?

The Iranian crisis may therefore widen the economic gap between Europe, the US and Asia.