The end of last week in financial markets had the feel of a classic Hollywood drama rescued by a last-minute reversal. Inflation and, above all, the prospect of a shift in monetary policy had cast a shadow over investor sentiment.

Midweek inflation figures in the US pointed to a renewed acceleration in price growth. Earnings reports from Oracle and SuperMicro also served as a reminder that the AI boom will require enormous investment.

Tech companies have consequently begun borrowing on a scale rarely seen in the sector. Higher financing costs could therefore hit an industry that has so far been largely shielded from elevated interest rates by strong margins and low debt levels.

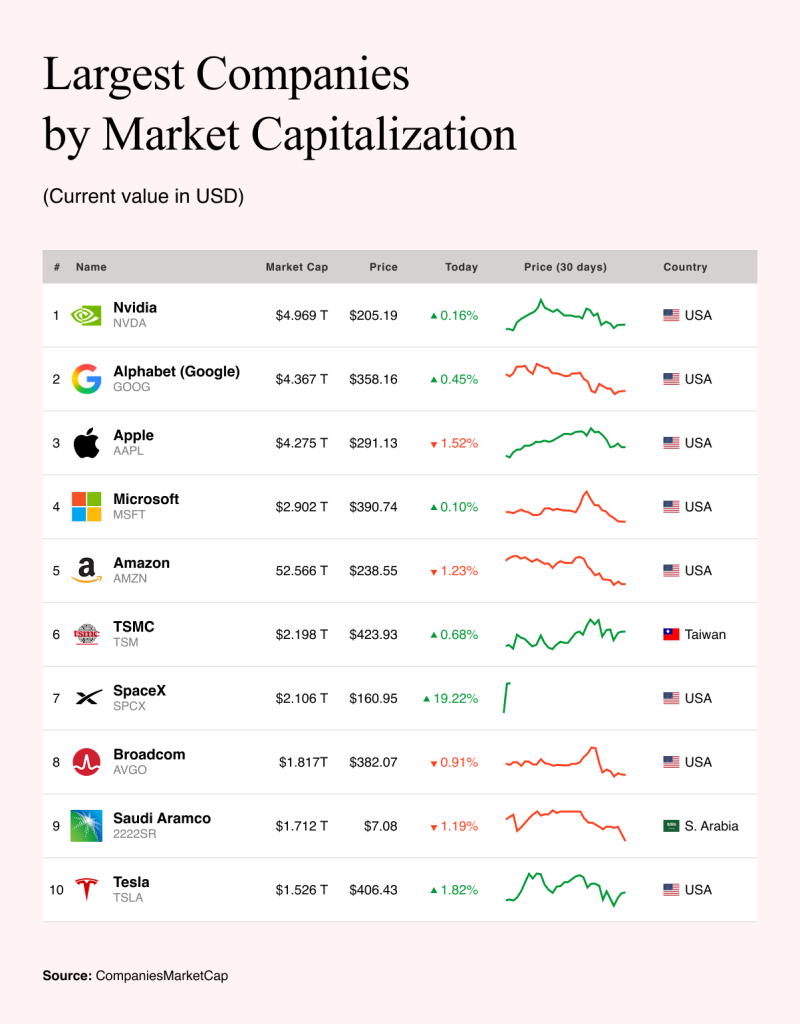

To cap off the week, the largest initial public offering in stock market history was due to take place: the listing of SpaceX. Had sentiment turned sour on Friday and had the IPO failed, a loss of faith in technological progress could have dragged down the entire AI sector. A sell-off in those stocks would then have weighed on the broader market. The stakes were exceptionally high.

Will the Deal Finally Be Signed?

At that critical moment, however, Donald Trump stepped onto the scene, announcing that the much-heralded and repeatedly delayed agreement between Iran and the US could finally be signed over the weekend. Further reports later supported his claim.

Iran was taking its time, but it was becoming increasingly clear that the talks had made substantial progress. That was enough to lift sentiment on Wall Street. Airline stocks gained the most, as expected, because an end to the conflict would be crucial for the sector.

Many are now trading at highly attractive valuations. Investors searching for cheap stocks, an exceptionally difficult task in today’s market, therefore have a wide range of options among airline companies.

Oil and natural gas prices, unsurprisingly, moved lower. The main question now is where they will eventually settle, particularly liquefied natural gas traded in Amsterdam.

The prevailing view among analysts is that a major collapse remains unlikely because Middle Eastern countries will have to spend heavily on rebuilding infrastructure.

Oil prices are also being distorted by the decision of several major economies to release strategic reserves to offset the shortfall in supplies passing through the Strait of Hormuz. Although prices have stabilized, those reserves will have to be replenished over time if the strait is reopened. A number of countries, particularly in Southeast Asia, have also recognized the need to build stockpiles of their own.

The alternative is that the damage proves less severe than feared, production and supplies recover quickly and oil falls below $60. The Trump administration would naturally welcome such an outcome, as it could improve its prospects in the November elections while easing pressure on the Federal Reserve to raise interest rates.

The US central bank would then have a stronger case for continuing to monitor developments without resorting to restrictive measures. The timing of the prospective peace agreement therefore not only helped Musk’s SpaceX go public but also worked in the Fed’s favor.

Europe Has Lost Influence and Risks Recession

At the same time, the episode highlighted how much influence, and therefore access to information, Europe has lost. The European Central Bank raised interest rates at its meeting, a controversial decision because tighter monetary policy will weaken the economy’s growth prospects.

Eurozone gross domestic product already fell by 0.2% in the first quarter of 2026, and higher rates may prolong the run of negative growth. The currency bloc could therefore slip into recession, commonly defined as two consecutive quarterly contractions.

The rate increase may prove particularly misguided if oil prices fall sharply and ease inflationary pressure across the EU. So far, that is exactly what appears to be happening. In trying to avoid repeating the mistake of the previous monetary cycle, when it waited too long to raise rates, the ECB may have shot itself in the foot. If prices continue to fall and inflation declines next month, Christine Lagarde and her colleagues will face sharp criticism.

SpaceX’s Astronomical Valuation and the Bet on AI

Donald Trump’s remarks helped create a more favorable backdrop for SpaceX’s initial public offering. The shares surged by more than 19% on their first day of trading.

Its market capitalization reached $2.1tn, immediately placing SpaceX seventh among the world’s most valuable companies. The listing also surpassed the previous largest IPOs, including those of Saudi Aramco and Musk’s other company, Tesla. Tesla shares rose by 1.82% as well, undermining fears that Elon Musk would gradually turn his attention exclusively to SpaceX.

The valuation, however, reflects not the company’s fundamentals but investors’ expectations that SpaceX will emerge as the next major technology leader. The underlying figures are far less impressive.

Last year, SpaceX lost $4.9bn on revenue of $18.7bn, and its losses deepened further in the first quarter. One of its largest clients is the US government, which awarded the company contracts worth $4bn through 2025. That is hardly a textbook example of free-market capitalism.

The astronomical valuation is therefore based not on current performance but on the one buzzword driving markets today: artificial intelligence. Elon Musk did not merely sell investors a rocket manufacturer or a satellite internet provider, even though Starlink is currently the company’s only profitable division. He sold them a grand vision of giant orbital data centers designed to power AI in the future.

Fundamentals have been cast aside, and the market is betting almost entirely on future growth. Some analysts have noted that the revenue expansion SpaceX would need to justify its valuation borders on the absurd.

For now, however, investors appear unconcerned. The successful IPO generated enormous returns for long-term backers and made Elon Musk, who owns about 40% of the company, the world’s first trillionaire, at least on paper.

The coming weeks will nevertheless test investors’ faith in SpaceX. Initial euphoria is often followed by a reality check, with the share price falling once the subscription phase is over. The pattern has affected companies that later became highly successful, including Facebook. Its strong IPO was followed by a sharp decline, and investors had to wait more than a year for the shares to return to their listing price.

The question is whether Musk will once again produce something genuinely new or ultimately follow the familiar Facebook model. In any case, buying into the stock immediately after the IPO would be an imprudent move for a long-term investor. Waiting until the initial market euphoria has subsided would make far more sense.